Canadian Dollar surged broadly overnight, following the strong rally in oil prices, partly due to strike in Norway which affect as much as one million barrels a day of crud oil production. The Loonie is also the strongest one for the week so far, awaiting employment data for the next move. Yen remains the weakest one together with New Zealand Dollar. Dollar is not too far away though. Some fresh selling is actually seen in the greenback in Asian session as Dollar might take on near term support against other majors before weekly close.

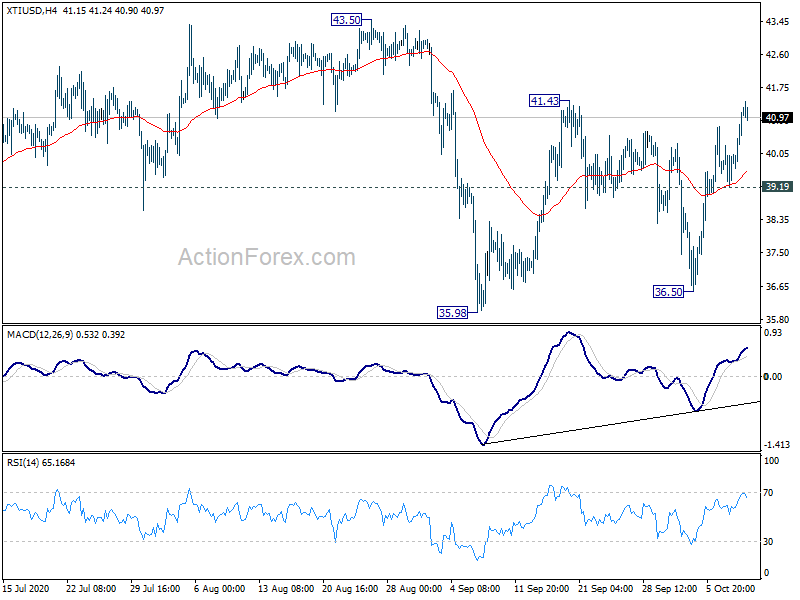

Technically, while the rebound of WTI from 36.50 is impressive, it’s not the less just part of the sideway consolidation pattern from 43.50. Strong resistance should be seen between 41.43/43.50 zone to limit upside of the next move. Break of 39.19 support should start another down leg back towards 35.98/36.50. Based on this view, the upside prospect of Canadian Dollar would depend more on today’s job data, as well as overall Dollar sentiments. 1.1807 minor resistance in EUR/USD would be a key to the next near term direction in Dollar and break will target a test on 1.2011 high, probably in tandem with Dollar selloff elsewhere.

– advertisement –

In Asia, currently, Nikkei is down -0.31%. Hong Kong HSI is up 0.16%. China Shanghai SSE is up 1.89%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down -0.0066 at 0.033. Overnight, DOW rose 0.43%. S&P 500 rose 0.80%. NASDAQ rose 0.50%. 10-year yield dropped -0.020 to 0.765.

Fed Rosengren: Fiscal policy is the right tool for this time

Boston Fed President Eric Rosengren said yesterday that “fiscal policy is the right tool for this time”. It’s “tragic that it has not been deployed already”. He also noted that his economic outlook was much weaker than other Fed policymakers because additional fiscal stimulus was not counted in.

“Most of my colleagues had an assumption that there was going to be additional fiscal stimulus. I had a somewhat different assumption,” he said. “I assumed no fiscal stimulus until the beginning of next year. As a result my forecast was much weaker than many of my colleagues.”

Rosengren also said the recovery from the pandemic was made more difficult due to the ” slow build-up of risk in the low-interest-rate environment that preceded the current recession”. He noted that commercial real estate firms have “gradually increased risk by taking on more leverage, which magnifies returns with good outcomes – but also magnifies losses when bad outcomes occur.

Fed Kaplan skeptical about benefits of more QE

Dallas Fed President Robert Kaplan said expected the economy to shrink about -2.5% this year, which is among the most bullish forecasts by Fed’s policymakers. Though, he noted the recession has hit some sectors and some groups of people worse than others. “It will take more than just a vaccine to revive depressed industries”.

The “number one economic policy, more than fiscal or monetary policy, is mask-wearing,” he said. “If there is no fiscal stimulus, mask-wearing, following health protocols will be even more important.”

Also, he’s “skeptical about the benefits of doing more” QE. “The bond-buying needs to curtail, the Fed balance sheet growth needs to curtail” when the pandemic crisis passes. Also, it’s not “healthy” for the markets to be “addicted, or too reliant” on Fed.

China Caixin PMI composite dropped to 54.5, economy remained in recovery phase

China Caixin PMI Services rose to 54.8 in September, up fro August’s 54.0, above expectation of 54.5. PMI Composite dropped to 54.5, down from 55.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the economy remained in a post-epidemic recovery phase and improved at a faster pace. Supply and demand both expanded in the manufacturing and services sectors…. In the near term, there will still be uncertainties from Covid-19 overseas and the U.S. election, and the development of “dual circulation” in the domestic and international markets will continue to face challenges.”

Elsewhere

Japan labor cash earnings dropped -1.3% yoy in August, better than expectation of -1.5% yoy. Household spending dropped -6.9% yoy, below expectation of -6.6% yoy.

Looking ahead, UK will release GDP, productions and trade balance. France and Italy will also release industrial output. Later in the day, Canada employment will take center stage.

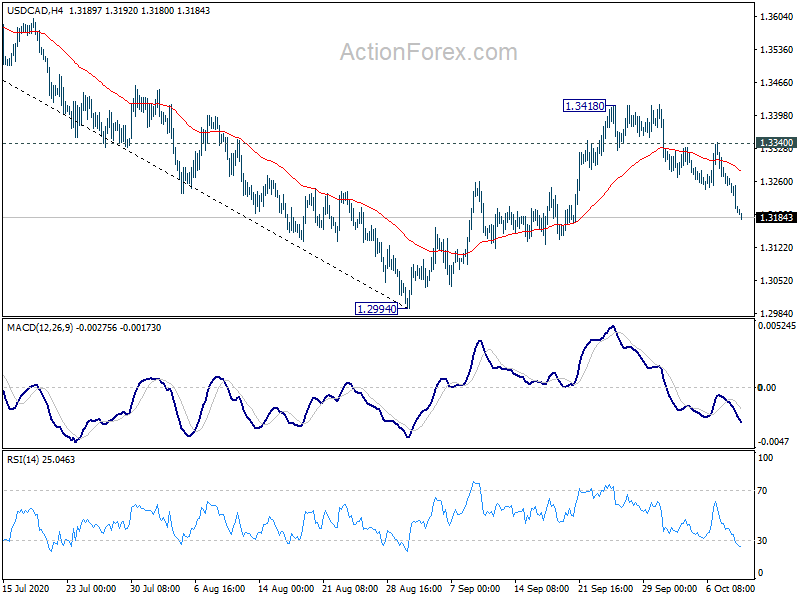

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3172; (P) 1.3219; (R1) 1.3244; More….

USD/CAD’s fall accelerates to as low as 1.3180 so far and intraday bias remains on the downside. Corrective rebound from 1.2994 should have completed and deeper decline would be seen to retest this low. Firm break there will resume larger down trend from 1.4667. On the upside, though, break of 1.3340 minor resistance will flip bias back to the upside to extend the corrective rebound from 1.2994 with another up leg.

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). Sustained break of 61.8% retracement of 1.2061 to 1.4667 at 1.3056 will target a test on 1.2061 (2017 low). But we’d expect loss of downside momentum as it approaches this key support. On the upside, firm break of 1.3715 resistance will argue that this falling leg has completed and turn focus back to 1.4667/89 resistance zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | -1.30% | -1.50% | -1.50% | |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | -6.90% | -6.60% | -7.60% | |

| 06:00 | GBP | GDP M/M Aug | 5.70% | 6.60% | ||

| 06:00 | GBP | Index of Services 3M/3M Aug | -4.00% | -8.10% | ||

| 06:00 | GBP | Manufacturing Production M/M Aug | 3.20% | 6.30% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Aug | -10.50% | -9.40% | ||

| 06:00 | GBP | Industrial Production M/M Aug | 2.60% | 5.20% | ||

| 06:00 | GBP | Industrial Production Y/Y Aug | -7.80% | |||

| 06:00 | GBP | Goods Trade Balance (GBP) Aug | -9.1B | -8.6B | ||

| 06:45 | EUR | France Industrial Output M/M Aug | 2.30% | 3.80% | ||

| 08:00 | EUR | Italy Industrial Output M/M Aug | 1.30% | 7.40% | ||

| 12:30 | CAD | Net Change in Employment Sep | 230.2K | 245.8K | ||

| 12:30 | CAD | Unemployment Rate Sep | 10.10% | 10.20% | ||

| 14:00 | USD | Wholesale Inventories Aug F | 0.50% | 0.50% |