Global stock markets are under heavy selling pressure as risk-off sentiment dominates the final trading day of February. The selloff intensified across major indices, with Japan’s Nikkei plunging -3% and Hong Kong’s Hang Seng Index down -2.8%, following the steep declines in US equities overnight. Investors are increasingly wary of escalating trade tensions, which could further weigh on the fragile global recovery.

Market sentiment took a sharp hit after confirmation that the 25% US tariffs on Mexico and Canada will take effect on March 4. The more consequential reciprocal tariffs, set for April 2, have also drawn attention, particularly with US President Donald Trump threatening to extend a 25% tariff on European Union imports.

NASDAQ was the hardest hit among US indices, tumbling -2.78%, with semiconductor giant Nvidia leading the declines with an -8.5% drop. Despite reporting strong quarterly earnings, the company is facing increased concerns that it won’t be immune to the broader trade war, particularly if Taiwan’s chip industry comes under new US tariff measures. Given Nvidia’s dominant role in the AI sector, any disruption in its supply chain could ripple through the entire tech sector.

In the currency markets, Dollar is now firmly leading the weekly performance rankings after its sharp rally overnight. Swiss Franc follows as the second-strongest, while Sterling also benefits from the broader selloff in Euro. Meanwhile, commodity-linked currencies are bearing the brunt of risk aversion, with New Zealand Dollar plunging the most, followed by Australian and Canadian Dollars. While Euro and Yen are positioned in the middle of the performance spectrum, the single currency is looking rather vulnerable.

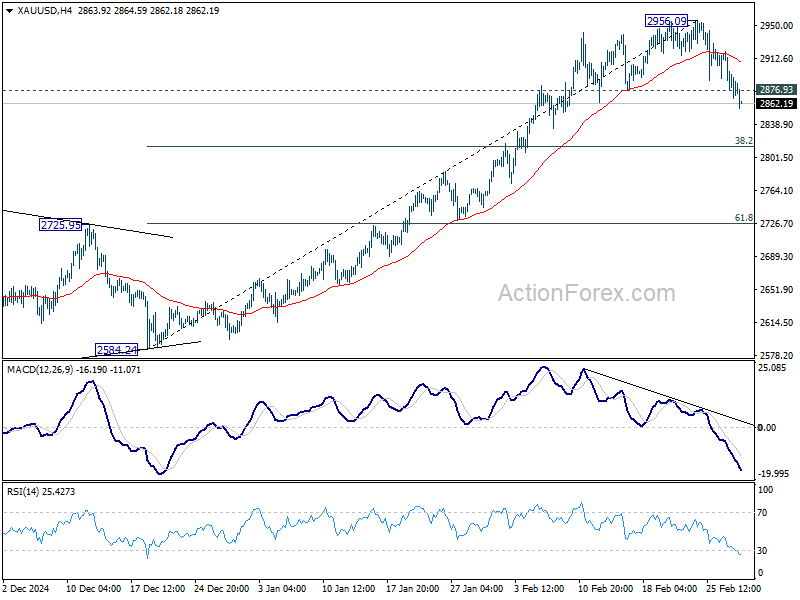

Technically, Gold’s extended decline is another confirmation of the Dollar’s underlying strength. The break of 2876.93 support confirms short-term topping at 2956.09, just below the key psychological 3000 level, with bearish divergence in 4H MACD.

Deeper correction should be seen to 38.2% retracement of 2584.24 to 2956.09 at 2814.04. Rebound from there indicate that it’s just a near term correction, and keep the larger up trend intact. However, sustained break of 2814.04 will suggest that a larger scale correction is already unfolding.

In Asia, at the time of writing, Nikkei is down -2.97%. Hong Kong HSI is down -2.58%. China Shanghai SSE is down -1.11%. Singapore Strait Times is down -0.72%. Japan 10-year JGB yield is down -0.023 at 1.373. Overnight, DOW fell -0.45%. S&P 500 fell -1.59%. NASDAQ fell -2.78%. 10-year yield rose 0.036 to 4.285.

BoJ’s Uchida: Yield rise reflects market’s views on economic and global developments

Speaking in parliament today, BoJ Deputy Governor Shinichi Uchida said recent rise in JGB yields “reflects the market’s view on the economic and price outlook, as well as overseas developments.”

“There’s no change to our stance on short-term policy rates and government bond operations,” he emphasized, adding that the bond holdings “continue to exert a strong monetary easing effect” on the economy.

When asked whether the prospect of further rate hikes and tapering would continue to drive yields higher, Uchida responded that it is ultimately “up to markets to decide.”

Japan’s Tokyo CPI slows to 2.2% yoy in Feb, industrial production down -1.1% mom in Jan

Tokyo’s core CPI (ex-food) slowed to 2.2% yoy in February, down from 2.5% yoy and below market expectations of 2.3% yoy. This marks the first decline in four months, largely due to the reintroduction of energy subsidies. Meanwhile, core-core CPI (ex-food and energy) held steady at 1.9% yoy. Headline CPI slowed from 3.4% yoy to 2.9% yoy.

In the industrial sector, production contracted by -1.1% mom in January, a sharper decline than the expected -0.9%. Manufacturers surveyed by Japan’s Ministry of Economy, Trade, and Industry anticipate a strong 5.0% mom rebound in February, followed by a -2.0% mom drop in March.

On the consumer front, retail sales grew 3.9% yoy in January, slightly missing the 4.0% yoy forecast, but still pointing to resilient domestic demand.

Fed’s Hammack signals cautious approach, stresses policy patience

Cleveland Fed President Beth Hammack said Fed has the “luxury of being patient” given the strength of the labor market and the uneven progress in reducing inflation.

In a speech overnight, she noted that while inflation has moderated, it remains above the 2% target, and policymakers are not yet confident that price pressures will fully subside. As a result, she expects the federal funds rate to stay steady “for some time”.

Hammack acknowledged that the current policy stance has helped ease inflation, but she warned that risks remain. While Fed anticipates a gradual return to 2% inflation over the medium term, she stressed that this is “far from a certainty.”

She suggested Fed will need to take a “patient approach” in monitoring how inflation and the labor market adjust before making any policy changes.

Fed’s Harker says one inflation report shouldn’t sway policy in either direction

Philadelphia Fed President Patrick Harker noted in a speech overnight that recent inflation data continues to show an uneven path toward the 2% target. He acknowledged that January’s consumer price data came in hotter than expected, marking the fastest increase in 18 months.

However, he stressed that policymakers should “not be moved to act, in either direction” based on a single month’s data.

Harker reaffirmed his stance that the Fed’s current policy rate remains sufficiently restrictive to keep inflation in check without undermining overall economic stability.

Despite inflation’s persistence, Harker remains optimistic about the economic outlook. He stated, “I am of a position that we let monetary policy continue to work.”

Looking ahead

Germany will release CPI flash, import prices, retail sales and unemployment in European session. Swiss will release KOF economic barometer.

Later in the day, Canada will publish GDP. Focus is also on US PCE inflation, goods trade balance and Chicago PMI.

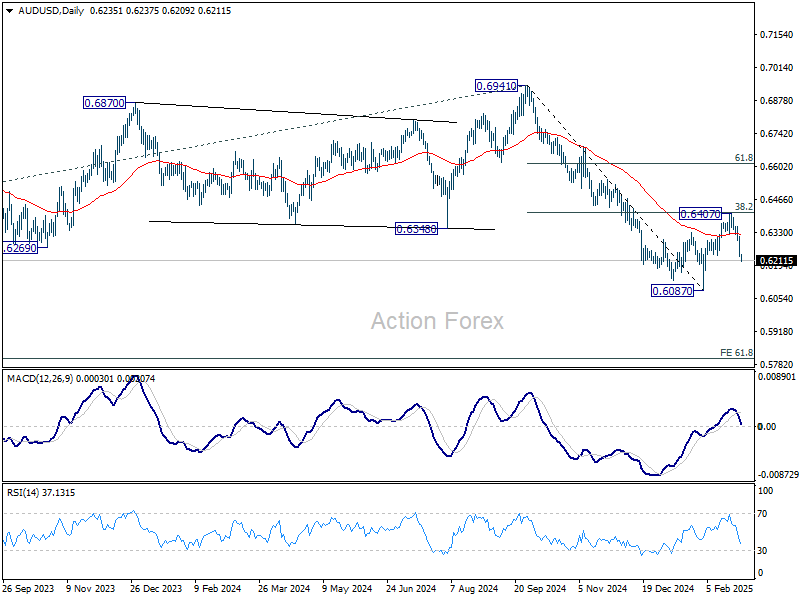

AUD/USD Daily Report

Daily Pivots: (S1) 0.6207; (P) 0.6261; (R1) 0.6291; More...

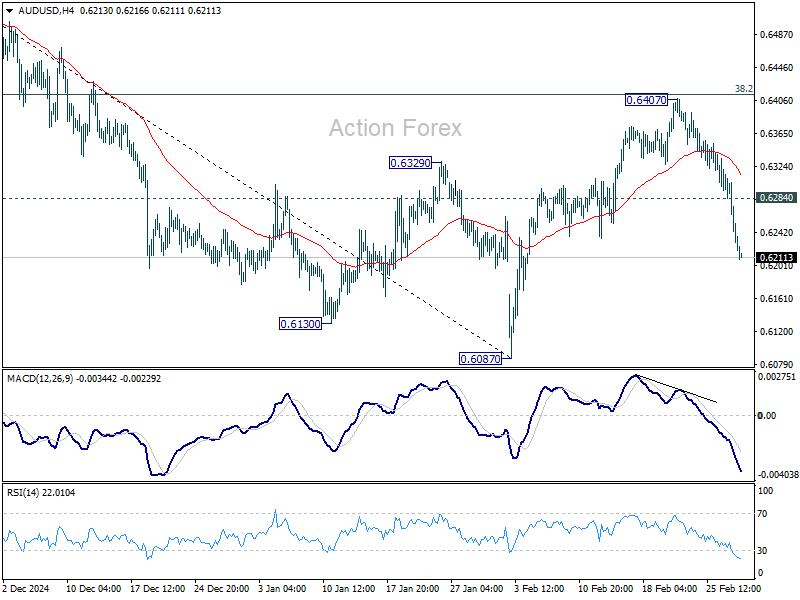

AUD/USD’s fall from 0.6407 accelerated lower today and intraday bias stays on the downside for retesting 0.6087 low. Decisive break there will resume larger decline from 0.6941. On the upside, above 0.6284 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.