Dollar surged sharply across the board in early US session trading after US President Donald Trump reinforced his tariff plans, clarifying uncertainties that had lingered in the market. In a Truth Social post, Trump confirmed that the tariffs on Canada and Mexico will “go into effect, as scheduled” on March 4. Additionally, China will face an extra 10% tariff on the same date. The April 2 reciprocal tariff announcement will also remain “in full force and effect,” he stated.

Market reaction was swift, with the greenback rallying against all major peers, even as incoming US economic data provided a mixed picture. January durable goods orders came in stronger than expected, but only driven largely by transportation equipment. Also, the labor market flashed a potential warning sign, as initial jobless claims surged to their highest level since December.

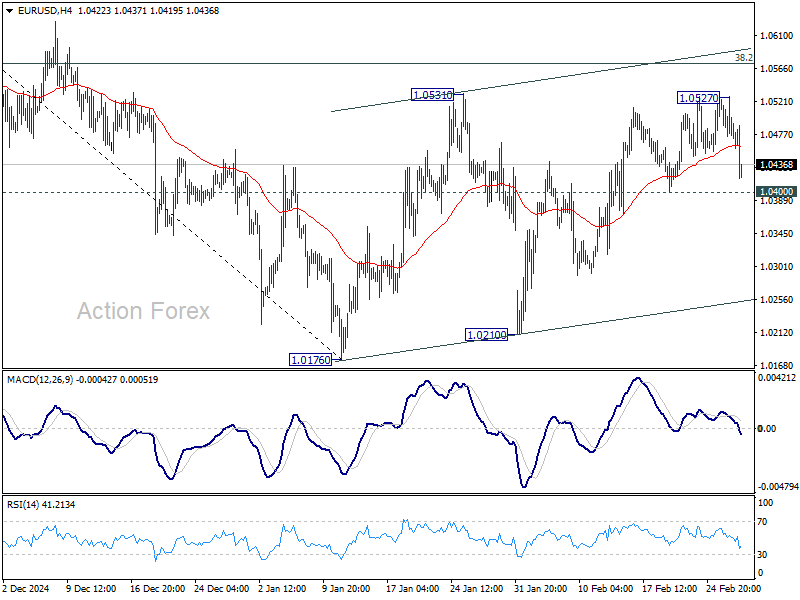

Yen and Swiss Franc are on the softer side today as US and European benchmark yields rebounded. However, neither currency showed a strong directional push. Euro, on the other hand, appears increasingly vulnerable, particularly against the British Pound. The latest selloff in EUR/GBP looks poised to gain further traction, as Eurozone fundamentals remain weak and tariff threats linger.

For the week so far, Dollar is now the strongest one with today’s rally. Sterling is sitting as the second, followed by Yen. Kiwi and Aussie are the worst performers for now, followed by Loonie. Euro and Swiss Franc are mixed in the middle.

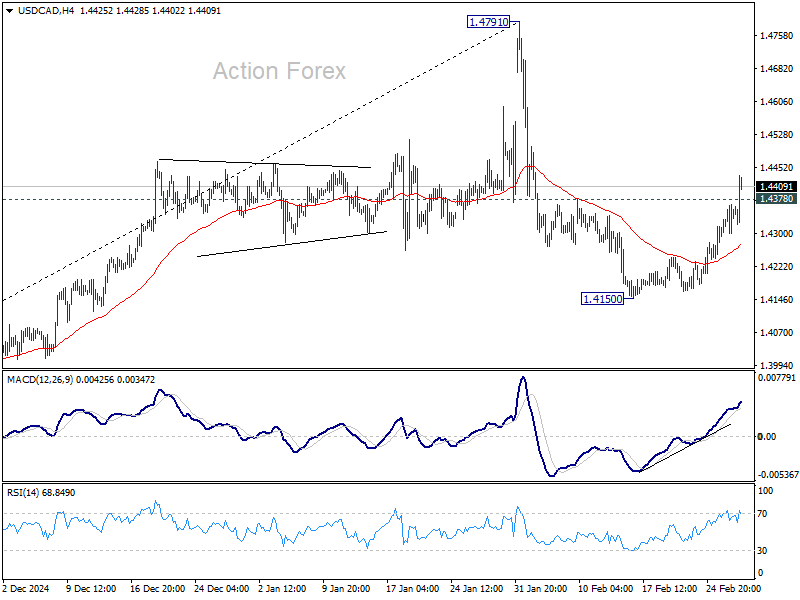

Technically, USD/CAD’s strong break of 1.4378 resistance suggests that corrective pullback from 1.4791 has already completed at 1.4150. Further rise is expected as long as 55 4H EMA (now at 1.4275) holds, for retesting 1.4791 high. Strong resistance might be seen there to limit upside on first attempt.

However, the final implementation of tariffs on Canada might provided the needed fuel to power USD/CAD through 1.4791 to resume the larger up trend.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is down -1.20%. CAC is down -0.77%. UK 10-year yield is up 0.014 at 4.520. Germany 10-year yield is up 0.002 at 2.438. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI fell -0.29%. China Shanghai SSE rose 0.23%. Singapore Strait Times rose 0.34%. Japan 10-year JGB yield rose 0.003 to 1.396.

US durable goods orders rise 3.1% mom, led by transportation equipment

US durable goods orders rose 3.1% mom to USD 286.0B in January, well above expectation of 2.0% mom. Transportation equipment led the increase by 9.8% to USD 96.5B.

Ex-transport orders was flat at 189.5B, below expectation of 0.4% mom. Ex-defense orders rose 3.5% mom to USD 268.7B.

US initial jobless claims jump to 242k, above expectation 220k

US initial jobless claims rose 22k to 242k in the week ending February 22, above expectation of 220k. Four-week moving average of initial claims rose 8.5k to 224k.

Continuing claims fell -5k to 1862k in the week ending February 15. Four-week moving average of continuing claims rose 3k to 1865k.

ECB Minutes: No room for forward guidance as caution prevails

ECB’s January 29-30 meeting account revealed that policymakers saw a “clear case” for a 25bps rate cut. Members agreed that disinflation is “well on track”, and confidence in inflation converging to target has grown.

However, the accounts highlighted several lingering uncertainties that warranted a cautious approach going forward. Policymakers emphasized the need to maintain a data-dependent stance, with “no room for forward guidance” at this stage.

Upside risks to inflation remained from elevated energy and food prices, strong wage growth, and persistent services inflation.

ECB also flagged geopolitical tensions, fiscal policy concerns within Eurozone, and global trade uncertainties as downside risks to growth, “which typically also implied downside risks to inflation over longer horizons.”

Swiss GDP expands 0.2% qoq in Q4, driven by domestic demand

Switzerland’s economy maintained steady growth in Q4, with GDP expanding 0.5% qoq when adjusted for sporting events. Without the adjustment, GDP rose 0.2% qoq, in-line with expectations.

Private consumption increased by 0.5%, supported by higher spending on health, recreation, and culture. Government consumption also grew at the same pace, slightly exceeding historical trends.

Investment in equipment rebounded 1.0%, breaking a two-quarter decline, largely due to higher spending on aircraft and other volatile categories.

The increase in domestic demand also led to a 0.9% rise in imports of goods and services, with foreign trade contributing positively to GDP growth.

RBA’s Hauser: Global uncertainty justifies rate cut, but more easing depends on disnflation evidence

RBA Deputy Governor Andrew Hauser told the parliament today that mounting global uncertainty had a chilling effect on economic activity, which played a role in the board’s decision to cut the cash rate by 25 bps this month.

He noted that businesses are becoming increasingly cautious, delaying investment projects and expansion plans as they wait for clearer economic signals, “just to see how things pan out.”

This hesitation, he suggested, made a slight easing of monetary policy a “sensible” response to support economic stability.

However, Hauser emphasized that further rate cuts are not guaranteed and will depend on incoming inflation data. Policymakers remain optimistic about further disinflation but need to see clear evidence before committing to additional policy easing.

NZ ANZ business confidence rises to 58.4, on the path to recovery

New Zealand’s ANZ Business Confidence rose from 54.4 to 58.4 in February. However, the Own Activity Outlook, slipped slightly from 45.8 to 45.1, highlighting that while sentiment is improving, actual activity remains uncertain.

Pricing and cost indicators painted a mixed picture. Inflation expectations for the next year eased from 2.67% to 2.53% and cost expectations fell from 73.6 to 71.3. But wage expectations remained elevated at 79.2 despite fall from 83.1, and pricing intentions ticked up from 45.7 to 46.2.

ANZ noted that the economy is on the “path to recovery,” supported by lower interest rates and stronger-than-expected commodity export prices. However, the bank cautioned that the next phase of growth remains “a point of debate.”

The pace of expansion will depend on how households perceive current interest rates, the extent to which global uncertainty influences business investment, and whether firms push forward despite challenges. Additionally, potential labor shortages could emerge as a key constraint on further growth.

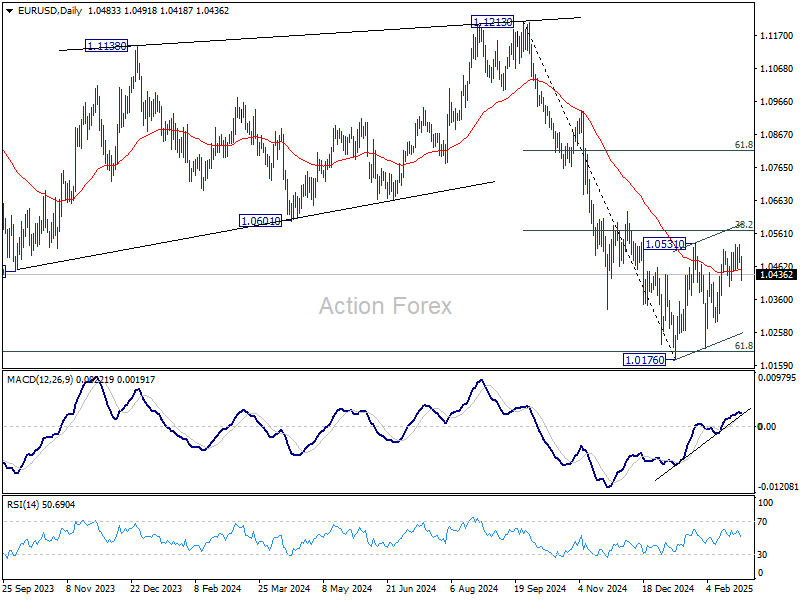

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0464; (P) 1.0496; (R1) 1.0518; More…

EUR/USD dips notably in early US session but stays above 1.0400 support. Intraday bias stays neutral first. Firm break of 1.0400 should indicate that corrective pattern from 1.0400 has completed. Intraday bias will be back on the downside for retesting 1.0176/0210 support zone. Overall, near term outlook will stay bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds in case of another recovery.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.