Dollar weakened notably against European majors and Yen as markets transitioned into US session, despite subdued overall trading activity. The decline was largely driven by extended fall in US 10-year Treasury yield, which hit its lowest level since mid-December.

Beyond geopolitical and trade war concerns, market focus has turned toward whether slowing US consumption and softer economic data could force Fed to resume rate cuts sooner than expected, even as inflation remains elevated. Fed funds futures now price in a near 65% chance of a 25bps rate cut in June, a notable increase from 45% just a week ago.

The next catalyst for Dollar’s direction will be consumer confidence report, set for release shortly. However, Dollar’s next moves may not be straightforward, as risk aversion—if it intensifies—could provide some support due to safe-haven demand. US stocks, particularly the tech-heavy NASDAQ, could be vulnerable on the upcoming Nvidia earnings report later in the week.

For now, commodity currencies are under the most pressure, with Kiwi leading the declines. On the other hand, Swiss Franc is the strongest performer, followed closely by Sterling and Euro. Dollar and Yen are positioned in the middle.

Looking ahead to the Asian session, Australia’s monthly CPI reading will draw attention. Consensus suggests inflation might edge up from 2.5% to 2.6% in January, supporting RBA’s cautious stance even after it initiated its easing cycle earlier this month. Still, a downside surprise would provide RBA with added confidence to proceed with additional rate cuts if economic conditions worsen.

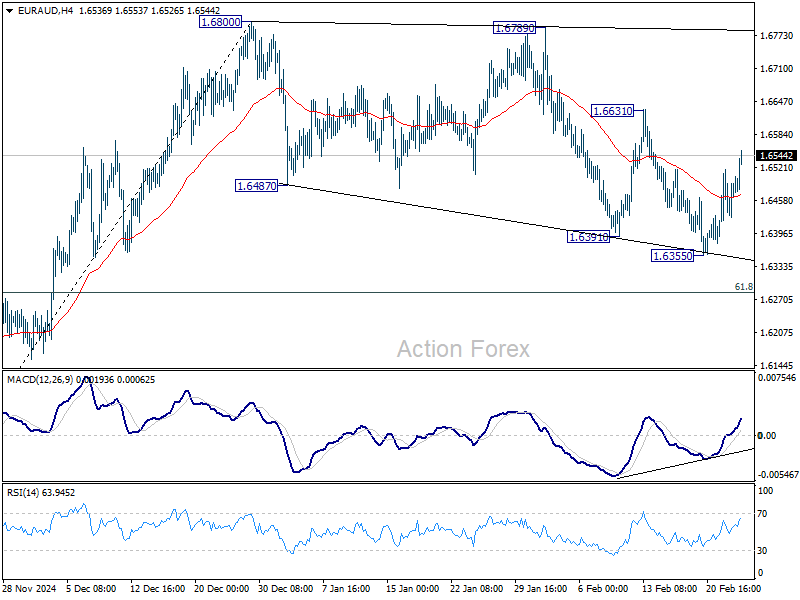

Technically, EUR/AUD’s rebound is gaining some momentum today. Firm break of 1.6631 resistance will argue that the corrective pattern from 1.6800 has completed, and larger rise from 01.5963 is finally ready to resume through 1.6800.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.43%. CAC is up 0.04%. UK 10-year yield is down -0.0475 at 4.525. Germany 10-year yield is down -0.0012 at 2.479. Earlier in Asia, Nikkei fell -1.39%. Hong Kong HSI fell -1.32%. China Shanghai SSE fell -0.80%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield fell -0.0511 to 1.376.

ECB’s Nagel expects more rate cuts Amid encouraging price trends

German ECB Governing Council member Joachim Nagel indicated that incoming data suggests the central bank is on track to achieve its inflation target this year, opening the door for further rate cuts.

Speaking today, Nagel stated, “This would allow us on the Governing Council to lower the key interest rates further,” reinforcing expectations that ECB will continue its gradual easing cycle.

However, Nagel also cautioned against premature optimism, highlighting “persistently elevated core inflation and the undiminished strength of services inflation.”

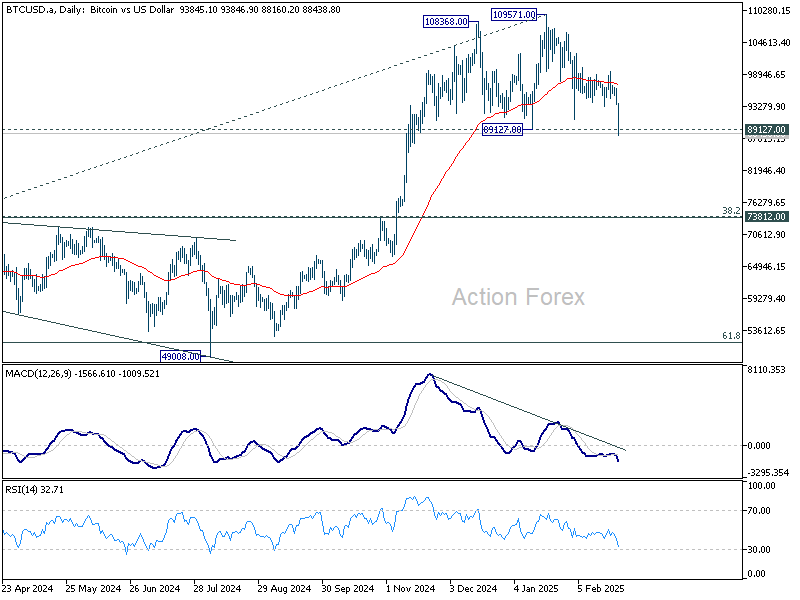

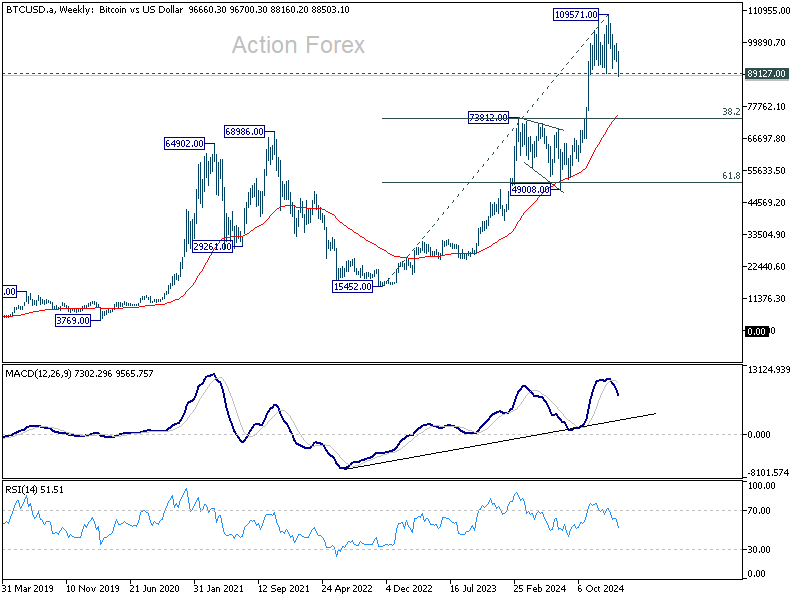

Bitcoin breaches 90K, double top breakdown could trigger deep correction

Bitcoin’s selloff intensified today, plunging below the 90k mark and hitting its lowest level since November. The immediate catalyst appears to be last week’s massive hack of USD 1.5B worth of Ether from cryptoexchange Bybit—an incident researchers have labeled the biggest crypto heist on record.

Although Bybit has announced that it fully restored the stolen Ether, market sentiment remains firmly negative, as traders grow wary of systemic risks and question the exchange’s ability to prevent future breaches.

Technically, Bitcoin now hovers at a critical juncture. The key 89,127 support level is under heavy pressure, and decisive break there would complete a double top pattern (108368, 108571). Such a development would strongly indicate that a larger-scale correction is underway.

In the bearish scenario, Bitcoin could be entering a correction of the entire rally from 15,452 (2022 low). The correction could target 73,812 cluster support (38.2% retracement of 15,452 to 109,571 at 73,617) before completion.

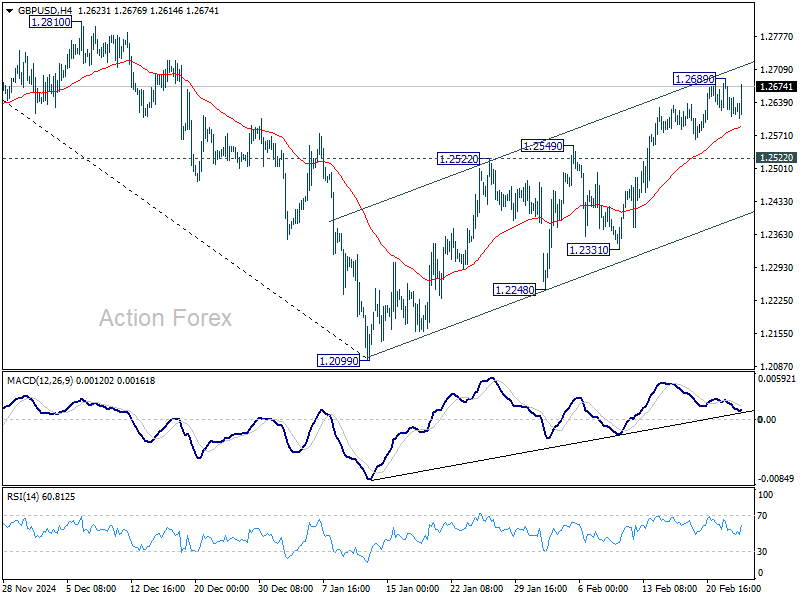

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2643; (R1) 1.2673; More…

Intraday bias in GBP/USD stays neutral at this point. Further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.