Euro’s brief post-election rally faded quickly, as investors welcomed CDU/CSU’s victory but remained cautious due to lingering uncertainties around coalition formation and fiscal policy. While a relatively centrist government comprising CDU and the Social Democrats would provide stability, challenges surrounding the “debt brake” reform and defense spending continue to cloud the outlook.

A coalition with the Greens and Social Democrats would likely be the most market-friendly outcome. However, even with these three parties combined, they fall short of the two-thirds parliamentary majority needed to reform the “debt brake”, which limits Germany’s structural budget deficit to 0.35% of GDP. Meanwhile, far-right AfD remains excluded from coalition talks, as Friedrich Merz has ruled out working with them.

This situation presents a fiscal dilemma for Germany, particularly given geopolitical uncertainties. The government faces pressure to increase both defense spending and broader fiscal stimulus, but policy divisions persist. The Left Party favors loosening the debt brake, but only for social and economic spending, not for increased defense expenditure. These divisions could complicate budget negotiations and delay much-needed investment decisions.

Bundesbank weighed in on the debate today, backing an increase in the government’s deficit cap, citing the need for higher public investment while Germany’s debt ratio remains low. In its monthly report, the Bundesbank argued that adapting the debt brake’s borrowing limit to current economic conditions is justified, but also stressed the importance of reviewing fiscal priorities and ensuring efficient use of financial resources.

In the currency markets, trading remains subdued, with major pairs and crosses confined within Friday’s ranges. Canadian, Australian, and New Zealand dollars are the strongest performers, while Yen is the weakest, followed by Swiss Franc and British Pound. Euro and Dollar are mixed in the middle.

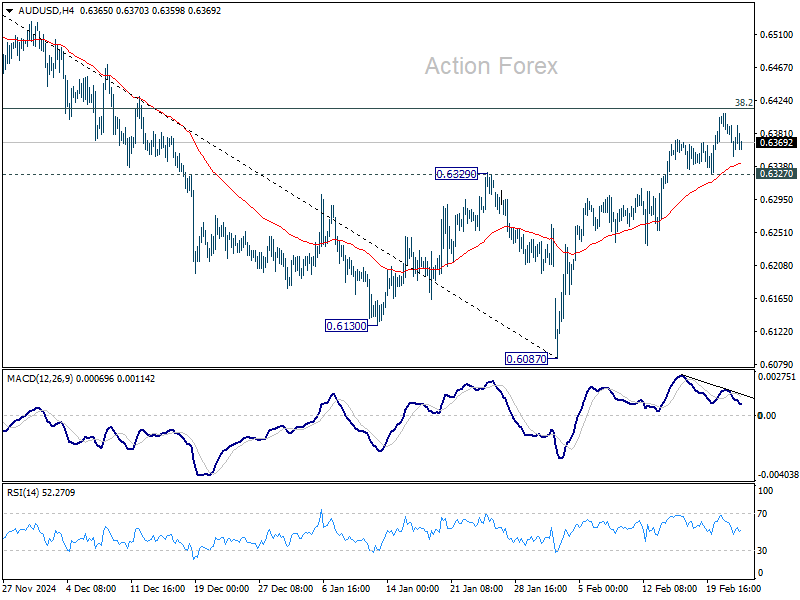

Technically, a major focus is whether the risk market selloff last week would extend today, and its impact in the forex markets. As for AUD/USD, firm break of 0.6327 support will suggest that corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Deeper decline would then be seen back to retest 0.6087, with prospects of resuming the whole fall from 0.6941.

In Europe, at the time of writing, FTSE is down -0.01%/ DAX is up 0.85%. CAC is down -0.22%. UK 10-year yield is up 0.0207 at 4.597. Germany 10-year yield is up 0.020 at 2.493. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -0.58%. China Shanghai SSE fell -0.18%. Singapore Strait Times fell -0.06%.

Eurozone CPI finalized at 2.5% in Jan, core CPI holds at 2.7%

Eurozone headline inflation was finalized at 2.5% yoy in January, ticking up from 2.4% yoy in December. Core CPI, which excludes energy, food, alcohol, and tobacco, remained unchanged at 2.7% yoy.

The largest contributor to Eurozone inflation was the services sector, which added 1.77 percentage points (pp) to the overall rate. Food, alcohol, and tobacco contributed 0.45 pp, while energy added 0.18 pp, and non-energy industrial goods accounted for 0.12 pp.

At the EU level, CPI was finalized at 2.8% yoy. The lowest inflation rates were seen in Denmark (1.4%), Ireland, Italy, and Finland (all 1.7%), indicating softer price pressures in some core economies. On the other hand, Hungary (5.7%), Romania (5.3%), and Croatia (5.0%) recorded the highest inflation levels, underlining regional imbalances in price stability.

Compared to December, inflation fell in eight EU member states, remained unchanged in four, and rose in fifteen.

German Ifo unchanged at 85.2, businesses waiting to see how things develop

Germany’s Ifo Business Climate Index was unchanged at 85.2 in February, falling short of expectations for a rise to 85.8. The data reflects that businesses are still “skeptical” about the outlook, “waiting to see how things develop”, according to the Ifo Institute.

Current Assessment Index dropped from 86.0 to 85.0, missing the forecasted 86.5. However, Expectations Index showed slight improvement, rising from 84.3 to 85.4, exceeding the consensus of 85.2.

Sector-wise, the manufacturing index improved from -24.8 to -22.1, and trade sentiment rebounded from -29.5 to -26.2. The construction sector also saw a marginal improvement, rising from -28.1 to -27.6. However, services weakened, falling from -2.2 to -4.3.

New Zealand retail sales rises 0.9% qoq in Q4, ex-auto sales jumps 1.4% qoq

New Zealand’s Q4 retail sales volume rose 0.9% qoq to NZD 25B, surpassing expectations of 0.6% qoq. Excluding autos, sales jumped 1.4% qoq, well above the 0.3% qoq forecast.

Sales volume growth was broad-based, with 10 of 15 industries posting gains. The largest increases came from electrical and electronic goods (+5.1%), department stores (+4.2%), and accommodation (+7.6%). Meanwhile, food and beverage services rose 2.3%, but pharmaceutical and other retailing declined -3.4%.

Retail sales value climbed 1.4% qoq to NZD 30B, with 11 of 15 sectors reporting gains. Price effects were evident, particularly in accommodation (+11%), food and beverage services (+3.3%), and department stores (+2.9%).

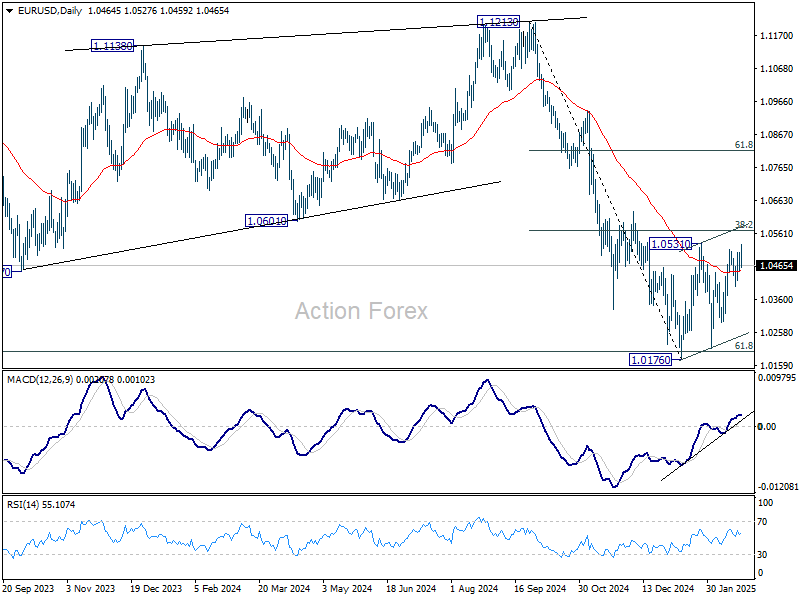

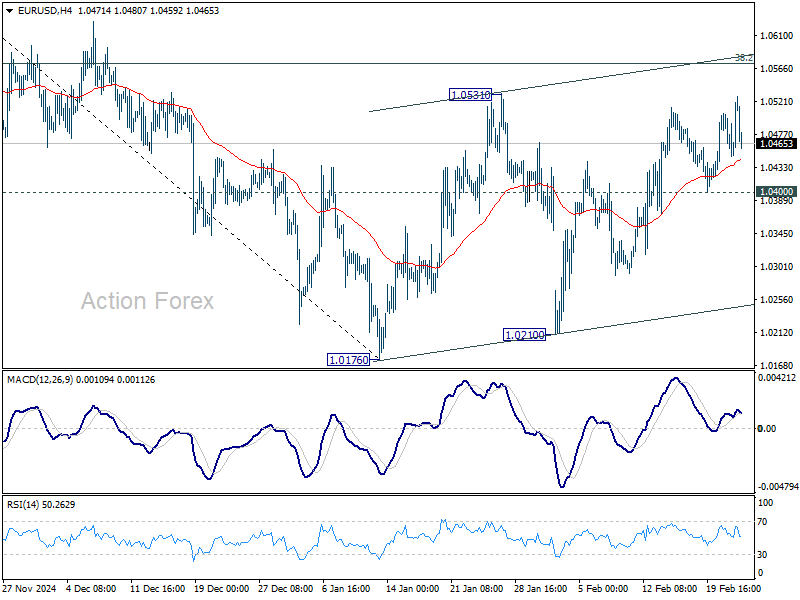

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0436; (P) 1.0474; (R1) 1.0499; More…

EUR/USD’s rally attempt today quickly lost momentum and intraday bias stays neutral. Outlook is unchanged that price actions from 1.0176 are forming a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.