Yen continues to dominate the relatively quiet forex markets today, with USD/JPY slipping below the key 150 psychological. The move is largely fueled by rising speculation that BoJ may tighten policy again sooner than expected, a sentiment that’s also reflected in 10-year JGB yield’s rally to another 15-year high. While the base case for BoJ’s next rate hike remains in the second half of the year, traders are increasingly betting on an earlier move—especially if this year’s Shunto wage negotiations deliver wage increases in line with last year’s strong outcomes.

The next major test for Yen will be Japan’s January CPI release in the upcoming Asian session. The market is expecting core CPI to rise slightly from 3.0% to 3.1%. Any upside surprise, particularly if core-core CPI (which excludes fresh food and energy) also rises, could strengthen market conviction that BoJ may need to act sooner than currently anticipated. A hot inflation print, combined with rising wage pressures, would likely push traders to further price in an earlier rate hike and adding to Yen strength.

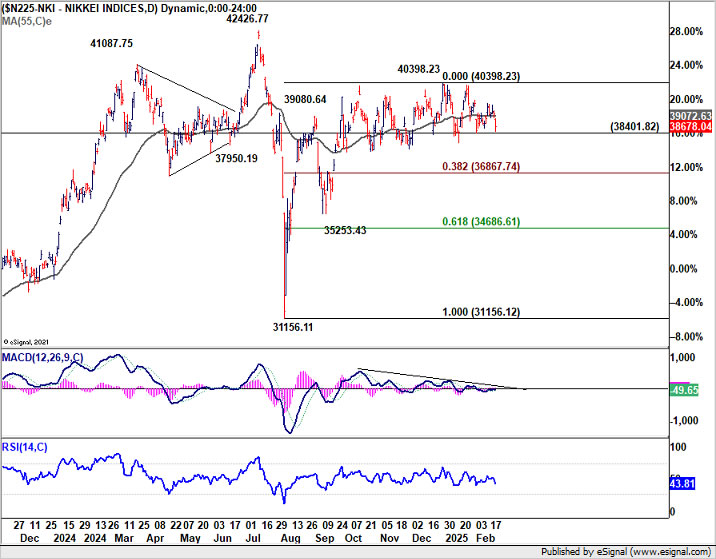

Beyond Yen’s rally, Nikkei 225 is also worth watching, as its technical outlook could provide further signals. Firm break of 38401.82 support could be an earlier sign that corrective rebound from 31156.11 has finally completed. That would set up deeper fall to 38.2% retracement 31156.11 to 40398.23 at 36867.74. If realized, deeper decline in Nikkei should also be accompanied by extended fall in USD/JPY.

In the broader currency market, Aussie ranks as the second-strongest performer today so far, supported by robust employment data and hawkish commentary from a senior RBA official. Kiwi is also firm, after RBNZ Governor Adrian Orr reaffirmed a slower pace of rate cuts ahead. Meanwhile, Dollar is under pressure, ranking as the weakest currency of the day, followed by Sterling and then Euro. Swiss Franc and Loonie are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.40%. DAX is up 0.19%. CAC is up 0.24%. UK 10-year yield is up 0.019 at 4.632. Germany 10-year yield is down -0.005 at 2.555. Earlier in Asia, Nikkei fell -1.24%. Hong Kong HSI fell -1.60%. China Shanghai SSE fell -0.02%. Singapore Strait Times fell -0.17%. Japan 10-year JGB yield rose 0.0106 to 1.450.

US initial jobless claims rise to 219k vs exp 216k

US initial jobless claims rose 5k to 219k in the week ending February 15, above expectation of 216k. Four-week moving average of initial claims fell -1k to 215k.

Continuing claims rose 24k to 1869k in the week ending February 8. Four-week moving average of continuing claims fell -8k to 1863k.

RBA’s Hauser: Rate cut justified, but inflation fight not a done deal

RBA Deputy Governor Andrew Hauser explained the 25bps rate cut to 4.10% earlier this week, highlighting that the decision was influenced by an “alternative version” of the inflation forecast. Under a scenario where rates remained unchanged, inflation would have undershot inflation target midpoint, albeit slightly. This factor played a key role in the board’s decision to ease policy.

However, Hauser struck a cautious tone on further cuts, emphasizing that core inflation at 3.2% remains above target. He reinforced that RBA’s remains “rigorously” focused on controlling price pressures, stating that the battle against inflation is “not a done deal” . He explained that RBA is not “whamming down on the accelerator”, but has simply “eased back on the brake a little bit”.

Regarding the strong January employment report release today, Hauser welcomed the figures, calling them part of a “striking employment growth” trend in Australia. He noted that Australia’s labor market performance stands out internationally, with strong participation rates and employment growth exceeding many other developed economies.

Australia’s employment grows 44k in Jan, outpacing population growth rate

Australia’s employment surged by 44k in January, more than double the expected 20k gain. The increase was driven by a 54.1k rise in full-time jobs, while part-time employment declined by -10.1k. However, the number of unemployed people also grew by 23k.

Employment growth at 0.3% mom matched 2024 monthly average, but outpacing population growth of 0.2%.

Unemployment rate edged up from 4.0% to 4.1%, in line with expectations, as the participation rate hit a record high of 67.3%, up from 67.2% in December. Meanwhile, monthly hours worked fell by -0.4% mom.

RBNZ’s Orr: No more 50bps cuts without a shock, sees stable inflation ahead

RBNZ Governor Adrian Orr reaffirmed that a 50bps rate cut would only happen again in the event of an economic shock, reinforcing the central bank’s guidance for two 25bps cuts in the first half of 2025.

Speaking before a parliamentary committee today, Orr noted that New Zealand is now in an environment of low and stable inflation, though global uncertainty remains a key risk.

He expressed optimism, stating that “GDP growth, employment growth, and low and stable inflation” should support an improving economic environment throughout the year. However, he warned that “geoeconomic fragmentation” is weighing on global growth, leading to increased price volatility in international markets.

RBNZ Chief Economist Paul Conway told the committee that escalating trade tensions will contribute to higher inflation, weaker global growth, and reduced economic efficiency. He stressed that “The best thing we can do is have headline inflation at 2% so that we can sort of absorb that future volatility.”

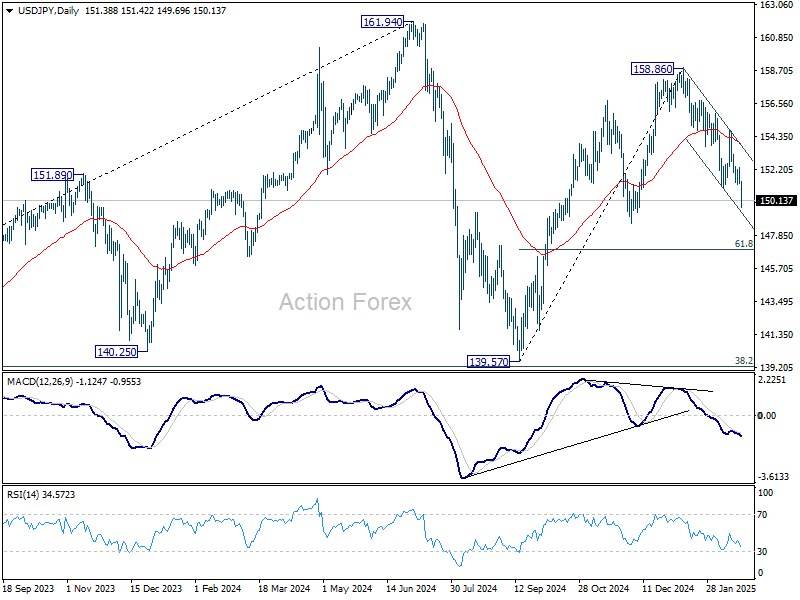

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.06; (P) 151.68; (R1) 152.12; More…

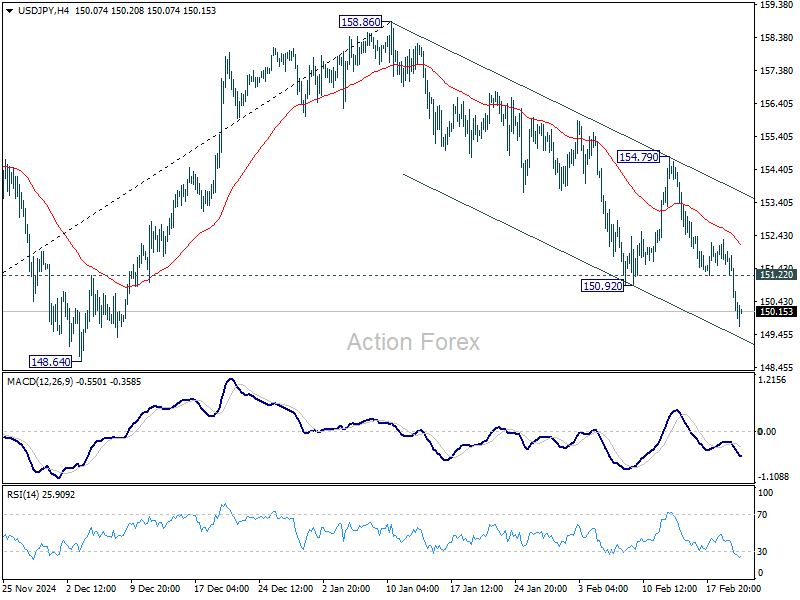

Intraday bias in USD/JPY remains on the downside for the moment. Fall from 158.86 is seen as the third leg of the pattern from 161.94 high. Deeper decline should be seen to 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, above 151.22 minor resistance will turn intraday bias neutral again first. But near term outlook will now stay bearish as long as 154.79 resistance holds.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.