The forex markets remain rather indecisive today. Traders are paring back expectations for BoE rate cuts after UK inflation surged to a 10-month high. A March rate cut is now off the table, and markets are no longer fully pricing in two BoE cuts this year. However, this shift has provided only minimal support for the British pound, as broader market sentiment remains cautious.

Meanwhile, Dollar is mildly firmer but lacks strong upside momentum. Traders are now focused on FOMC minutes, which are expected to reaffirm that Fed is in no rush to cut rates. Current Fed funds futures show a 55% probability that rates will remain at 4.25-4.50% through the first half of 2025, a view that is unlikely to change much without further clarity on President Donald Trump’s fiscal and trade policies.

In the commodities market, Gold surged to a record high, approaching the critical 3000 psychological level for another attempt. This marks a key inflection point—a decisive break above 3,000 could pave the way to 61.8% projection of 1810.26 to 2789.92 from 2584.24 at 3189.66.

However, failure to sustain gains above 3000 could lead to deeper pullback. Firm break 2876.93 support should set up correction back towards 2789.92 resistance turned support instead.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is down -1.16%. CAC is down -0.84%. UK 10-year yield is up 0.0696 at 4.629. Germany 10-year yield is up 0.058 at 2.558. Earlier in Asia, Nikkei fell -0.27%. Hong Kong HSI fell -0.14%. China Shanghai SSE rose 0.81%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.0038 to 1.440.

ECB’s Schnabel: Rate Cut Pause May Be Approaching

ECB Executive Board member Isabel Schnabel suggested in an FT interview that the central bank is approaching a point where it “may have to pause or halt” rate cuts.

While she refrained from making a firm prediction for upcoming policy meetings, she acknowledged that the ECB needs to “start that discussion”.

Schnabel highlighted that the degree of monetary restriction “has come down significantly”, to the extent that policymakers can “no longer say with confidence” that ECB’s stance remains restrictive.

She defended the ECB’s gradual and cautious approach, arguing that domestic inflation remains high, wage growth is still elevated, and energy price shocks continue to impact inflation expectations.

ECB’s Panetta: Eurozone economic weakness more persistent than expected

Italian ECB Governing Council member Fabio Panetta acknowledged that economic weakness in the Eurozone is proving “more persistent than we expected”, as the long-anticipated consumption-driven recovery has yet to materialize.

After two consecutive quarters of stagnation, he noted that “tensions in the manufacturing sector, employment is giving signs of weakening”

Panetta also highlighted the downside risks to inflation stemming from weak growth. However, he also noted that upside inflation risks remain, primarily from energy costs.

UK CPI surges to 3.0%, highest since March 2024

UK headline CPI accelerated to 3.0% yoy in January, up from 2.5% yoy and exceeding market expectations of 2.8% yoy. This marks the highest inflation level since March 2024, reinforcing concerns that price pressures remain persistent.

Core inflation also surged, with CPI excluding energy, food, alcohol, and tobacco rising to 3.7% yoy, up from 3.2% yoy in December.

Meanwhile, CPI goods inflation edged higher from 0.7% yoy to 1.0% yoy, while CPI services inflation climbed from 4.4% yoy to 5.0% yoy.

RBNZ cuts by 50bps, signals further easing through 2025

RBNZ cut the Official Cash Rate (OCR) by 50bps to 3.75%, as widely expected, while maintaining a clear easing bias.

The central bank stated that “if economic conditions continue to evolve as projected, the Committee has scope to lower the OCR further through 2025.” According to the latest projections, the OCR is expected to decline to 3.1% by year-end and remain at that level until early 2028.

RBNZ acknowledged that economic activity remains subdued, though it expects growth to recover in 2025, driven by lower interest rates encouraging spending. However, elevated global economic uncertainty is likely to weigh on business investment. The bank also noted that inflation is expected to be volatile in the near term, influenced by a weaker exchange rate and higher petrol prices.

Regarding global risks, the RBNZ flagged concerns and warned that higher global tariffs could slow growth in key trading partners, dampening demand for New Zealand exports and weakening domestic economic momentum over the medium term.

However, the impact on inflation is “ambiguous”, depending on factors such as trade diversion, supply-chain adjustments, and financial market reactions.

Australian wages growth slow 0.7% qoq, pressures easing

Australia’s wage price index rose 0.7% qoq in Q4, marking a slowdown from 0.9% qoq and missing expectations of 0.8% qoq. This matches the lowest quarterly growth since March 2022, reinforcing signs that wage pressures are easing, albeit still elevated.

On an annual basis, wages increased 3.2% yoy, making it the slowest pace since Q3 2022. Private sector wage growth came in at 3.3% yoy, the weakest since Q2 2022. Public sector wages rose 2.8% yoy, falling below 3% for the first time since Q2 2023.

BoJ’s Takata: Gradual policy shifts should continue beyond January hike

BoJ Board Member Hajime Takata emphasized the need for the central bank to continue to “implement gear shifts gradually, even after the additional rate hike decided in January 2025”, to mitigate the risk of rising prices and financial market overheating.

Takata noted in a speech today that as “positive corporate behavior” persists, BoJ should consider a “further gear shift” in policy.

He highlighted three key risks that could drive prices above BoJ’s baseline scenario: a stronger wage-price cycle, inflationary pressures from domestic factors, and market volatility, especially in the exchange rates, stemming from a recovery in the US economy.

Nevertheless, due to uncertainties surrounding the US economy and the challenge of identifying the neutral interest rate, Takata advocated for a “vigilant approach”.

Japan’s trade deficit widens as imports surge, exports to China drop

Japan’s trade deficit expanded sharply in January, reaching JPY -2.759T, the largest shortfall in two years, as imports surged 16.7% yoy, far exceeding the expected 9.3% yoy gain.

Meanwhile, exports rose 7.2% yoy, falling slightly short of the 7.7% yoy forecast, with strong shipments to the U.S. (+18.1% yoy) offset by a -6.2% yoy decline in exports to China.

On a seasonally adjusted basis, exports declined -2.0% mom to JPY 9.253T, while imports climbed 4.7% mom to JPY 10.109T, leading to a JPY -857B trade deficit.

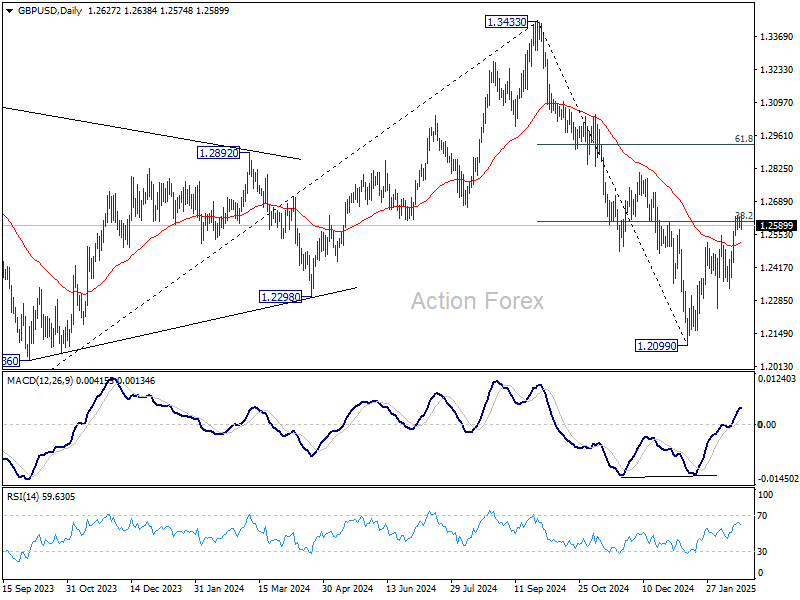

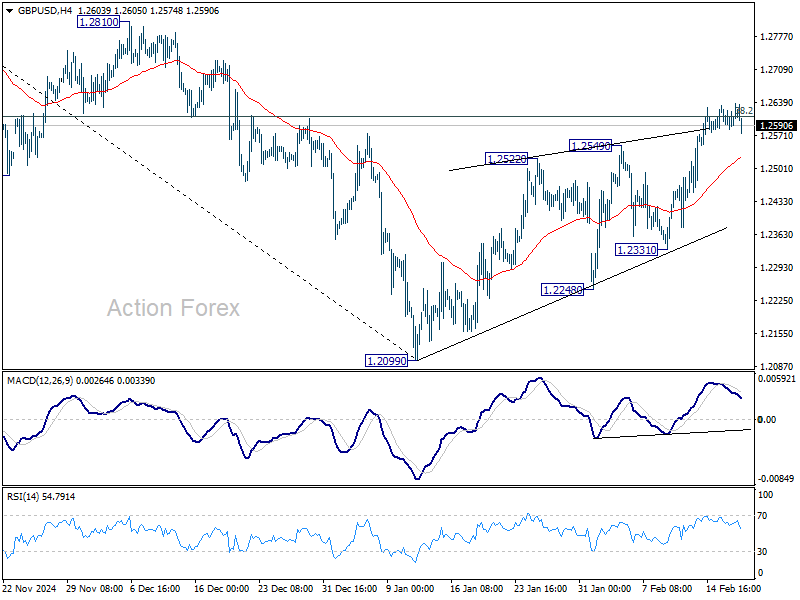

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2587; (P) 1.2609; (R1) 1.2637; More…

GBP/USD dips mildly today but stays in established tight range. Intraday bias remains neutral, and focus stays on 38.2% retracement of 1.3433 to 1.2099 at 1.2609. Rejection by this level will keep near term outlook bearish. Break of 1.2331 support will suggest that the rebound from 1.2099 has completed as a correction, and bring retest of 1.2099 low. However, firm break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.