Australian Dollar initially dipped after RBA’s widely expected rate cut, but the move was short-lived as the currency quickly stabilized. RBA’s cautious tone on further easing provided underlying support for the Aussie. The central bank made it clear that while policy easing has begun, it is not committing to a rapid or continuous rate-cut cycle.

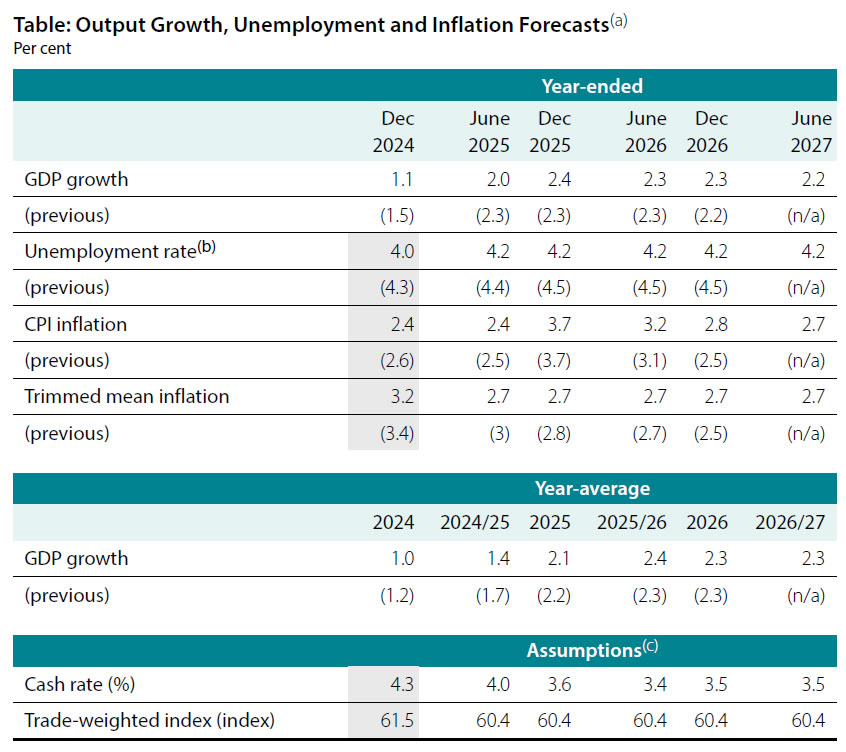

The updated economic projections justify RBA’s cautious stance. Trimmed mean CPI is expected to stay at 2.7% throughout the forecast horizon, remaining above the midpoint of the RBA’s 2-3% inflation target. Meanwhile, the unemployment rate forecast was lowered to 4.2% and is expected to hold steady, indicating a persistently tighter-than-expected labor market.

RBA’s own cash rate assumptions suggest a drop to 3.60% by the end of 2025, implying just two more cuts before a prolonged pause. This guidance is against expectations for an aggressive easing cycle and could help limit AUD downside in the near term.

In the broader currency market, Dollar leads as the strongest performer of the day so far, recovering some of last week’s losses. Loonie follows as second, while Aussie holds third place. In contrast, Kiwi is the weakest, followed by Yen and Euro. Swiss Franc and Sterling are hovering in the middle of the pack.

Market focus now shifts to key upcoming economic data releases, including UK GDP, German ZEW economic sentiment, and Canadian CPI.

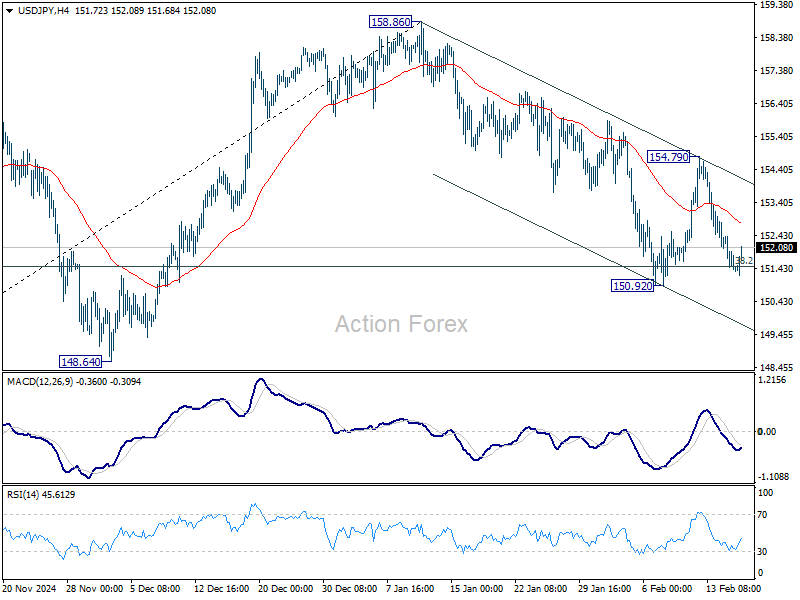

Technically, a main focus for today is whether USD/JPY could stage an extended rebound after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.4 for the second time. Firm break of 55 4H EMA (now at 152.08) will be the first signal of bottoming. Firm break of 154.79 resistance will revive near term bullishness for resuming the rally from 139.57 at a later stage.

In Asia, at the time of writing, Nikkei is up 0.68%. Hong Kong HSI is up 1.94%. China Shanghai SSE is up 0.29%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is up 0.0158 at 1.408.

RBA cuts rates, but warns against easing too much too soon

RBA lowered its cash rate target by 25bps to 4.10%, as widely anticipated, but signaled a cautious approach to further easing.

In its statement, the central bank emphasized that monetary policy will remain restrictive even after today’s reduction, warning that if rates are “eased too much too soon”, disinflation progress could stall and inflation could settle above the midpoint of the target range.

RBA acknowledged that some upside risks to inflation “appear to have eased”, and disinflation may be unfolding “a little more quickly than earlier expected”. However, it maintained that “risks on both sides” remain.

While today’s cut reflects the central bank’s confidence in recent progress, policymakers remain “cautious about the outlook”, reinforcing the idea that future easing will be data-dependent rather than pre-committed.

In the new economic projections:

- Headline CPI is now projected to rise to 3.7% by the end of 2025, before gradually easing to 2.8% by the end of 2026 (raised from 2.5%), and settling at 2.7% by mid-2027.

- Trimmed mean CPI is expected to remain at 2.7% throughout 2025, 2026, and mid-2027.

- Unemployment rate forecast was lowered to 4.2% across the projection horizon

- Year-average GDP growth was revised down by 0.1% to 2.1% for 2025, while 2026 remains unchanged at 2.3%, with growth expected to hold steady at 2.3% into 2026/2027.

- Cash rate assumptions suggest an average rate of 3.6% in 2025, followed by 3.5% in 2026.

Fed’s Waller downplays tariff impact, warns against policy paralysis

Fed Governor Christopher Waller downplayed concerns that tariffs would have a significant, lasting impact on inflation, stating that their effect is likely to be “modest” and “non-persistent.” As a result, he favors “looking through” these effects when setting policy.

In a speech overnight, he emphasized that while economic uncertainty remains, Fed cannot afford to fall into a “recipe for policy paralysis” by waiting for absolute clarity regarding the administration’s policies.

However, he conceded that tariffs could have a larger impact than expected, depending on their size and implementation. At the same time, he pointed out that other policies under discussion could have positive supply-side effects, helping to ease inflationary pressures.

Waller defended Fed’s decision to hold rates steady in January, arguing that the current economic data “are not supporting a reduction in the policy rate at this time.”

He left the door open for future rate cuts, stating that “if 2025 plays out like 2024, rate cuts would be appropriate at some point this year.”

Looking ahead

UK employment data is the main focus in European session, along with German ZEW economic sentiment. Later in the data, attention will be on Canada CPI. US will release Empire state manufacturing index and NAHB housing index.

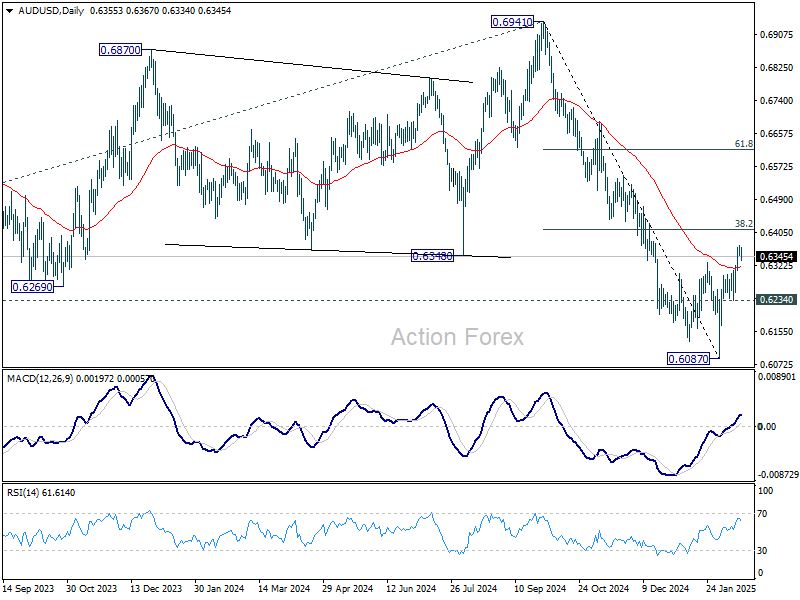

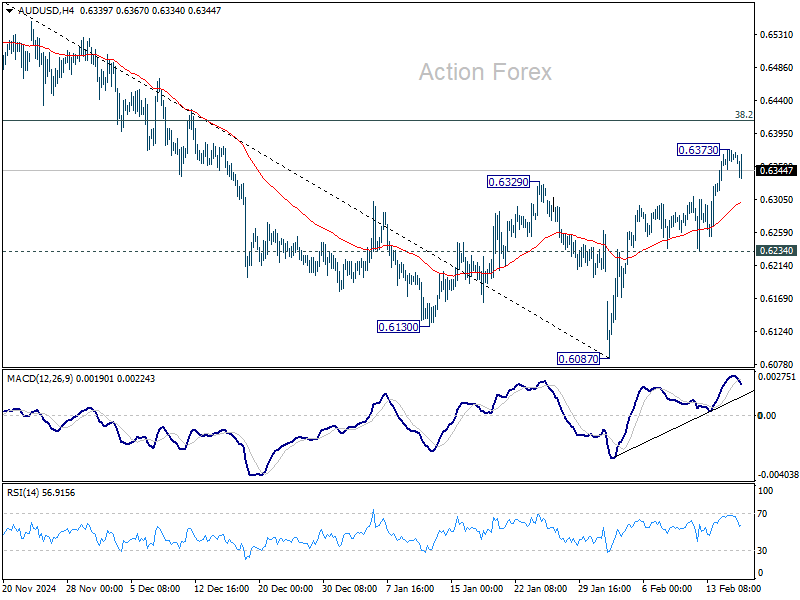

AUD/USD Daily Report

Daily Pivots: (S1) 0.6345; (P) 0.6359; (R1) 0.6372; More...

Intraday bias in AUD/USD is turned neutral as rebound from 0.6087 lost moment, as seen in 4H MACD, after hitting 0.6373. On the downside, break of 0.6234 support will suggest that the rebound has completed as a correction, and turn bias back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 38.2% retracement of 0.6941 to 0.6087 at 0.6413, will pave the way back to 61.8% retracement at 0.6615.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6504) holds.