Yen remains the standout performer, even though momentum had moderated slightly. Discussions surrounding BoJ’s next move continue to dominate, particularly in a low-activity session with both US and Canadian markets closed for holidays.

After stronger than expected Japanese Q4 GDP report, market expectations for a July rate hike to 0.75% have strengthened to around 80%. However, the timeline could shift sooner if results from the upcoming Shunto wage negotiations indicate stronger-than-expected wage growth.

Looking further ahead, some analysts see BoJ’s policy rate reaching 1% by year-end, which would mark the lower bound of its own estimated neutral rate range of 1-2.5%. This shift in policy expectations has kept Yen well-supported against its peers for now.

In the upcoming Asian session, focus is turning toward RBA, which is widely anticipated to begin its easing cycle with a 25bps rate cut to 4.10%. A Reuters poll of economists showed that 31 out of 41 analysts expect another quarter-point cut in Q2, bringing rates down to 3.85%.

Among major Australian banks, ANZ, CBA, NAB, and Westpac all foresee a 25bps cut tomorrow, but their forecasts for cumulative cuts in 2025 vary between 50 and 100 basis points. Market participants will closely watch the RBA’s guidance and updated economic forecasts for further clues on the policy path ahead.

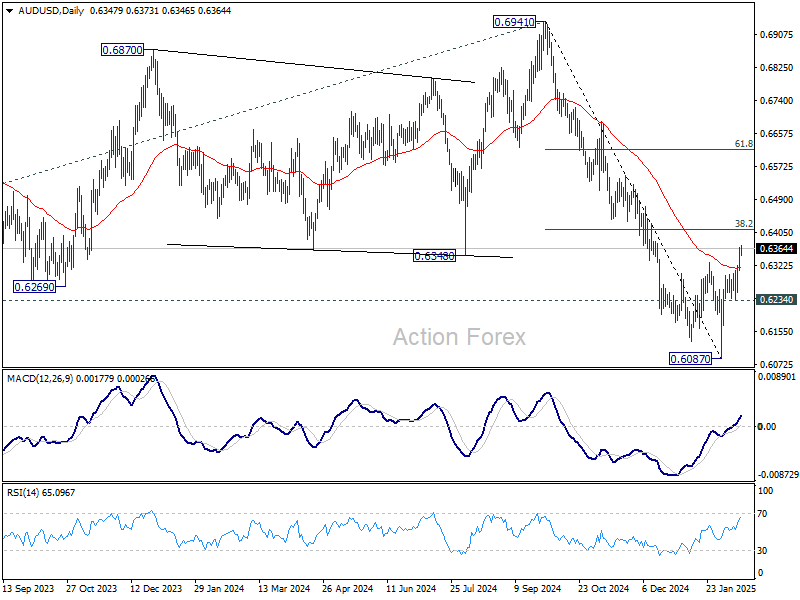

Technically, AUD/USD’s rebound from 0.6087 is seen as a corrective move only, probably the first leg of a consolidation pattern to the decline from 0.6941. Strong resistance should be seen from 38.2% retracement of 0.6941 to 0.6087 at 0.6413 to limit upside. However, sustained break there could bring stronger rise to 61.8% retracement at 0.6615, even still as a correction.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.93%. CAC is up 0.11%. UK 10-year yield is up 0.0414 at 4.551. Germany 10-year yield is up 0.056 at 2.490. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI fell -0.02%. China Shanghai SSE rose 0.27%. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield jumped 0.0362 to 1.393.

BoE’s Bailey sees ongoing gradual disinflation, warns of two-sided risks

BoE Governor Andrew Bailey reaffirmed today that the UK remains on “gradual disinflation” path, noting that the lingering effects of past economic shocks are slowly fading.

However, he emphasized that risks are “two-sided,” as highlighted in the BoE’s latest minutes, where differences within the committee surfaced.

On Q4 GDP data, which came in stronger than expected, Bailey downplayed its impact, stating that the economy has been “quite static” since late spring 2024.

Regarding the US government’s evolving stance on tariffs, Bailey expressed concerns about economic fragmentation, warning that such shifts could harm global growth.

However, he acknowledged that the inflationary impact from tariffs remains “ambiguous,” as it depends on factors such as “redirection of trade” and retaliatory measures.

He reiterated that risks exist on both sides, justifying the BoE’s use of “careful” alongside “gradual” in its policy guidance.

Eurozone goods exports rises 3.1% yoy in Dec, imports rises 3.8% yoy

Eurozone goods exports rose 3.1% yoy to EUR 226.5B in December. Goods imports rose 3.8% yoy to EUR 211.0B. Trade balance recorded EUR 15.5B surplus. Intra-Eurozone trade rose 1.7% yoy to EUR 191.5B.

In seasonally adjusted term, goods exports fell -0.2% mom to EUR 240.8B. Goods imports fell -0.8% mom to EUR 226.2B. Trade balance reported EUR 14.6B surplus, smaller than expectation of EUR 15.0B. Intra-Eurozone trade rose 0.6% mom to EUR 213.1B.

Japan’s Q4 GDP beats forecasts with 0.7% qoq growth

Japan’s economy expanded by 0.7% qoq in Q4 2024, surpassing market expectations of 0.3% qoq and improving from the previous quarter’s 0.4% qoq rise. On an annualized basis, GDP grew 2.8%, significantly above 1.0% forecast and accelerating from Q3’s 1.7% pace.

Private consumption, which accounts for over half of Japan’s economic output, edged up by 0.1% qoq, defying expectations of a -0.3% qoq contraction. However, it slowed sharply from the 0.7% qoq increase recorded in Q3, reflecting a cautious spending environment.

Capital spending improved by 0.5% qoq, reversing the -0.1% qoq decline in Q3, but fell short of the anticipated 1.0% qoq rise.

Price pressures continued climbing, with the GDP deflator inching up from 2.4% yoy to 2.8% yoy.

Despite the strong Q4 performance, full-year 2024 GDP growth slowed sharply to 0.1%, a steep decline from the 1.5% expansion in 2023.

NZ BNZ services rises to 50.4, stabilization rather than elevation

New Zealand BusinessNZ Performance of Services Index climbed from 48.1 to 50.4 in January, marking a return to expansion after four consecutive months of contraction. While this signals some improvement, the index remains below its long-term average of 53.1.

A closer look at the components reveals a mixed picture. Activity/sales saw a notable rebound, rising from 46.5 to 54.0, while new orders/business ticked up slightly from 49.4 to 50.0. Stocks/inventories also edged into expansion territory at 50.1, up from 48.9. However, employment continued to struggle, slipping from 47.4 to 47.1. Supplier deliveries showed minimal improvement, moving from 47.7 to 47.8.

Despite the headline figure turning positive, sentiment remains weak. The proportion of negative comments rose to 61.9% in January, up from 57.5% in December and 53.6% in November. Respondents cited economic uncertainty and broader downturn concerns as key issues.

BNZ’s Senior Economist Doug Steel noted that the PSI reflects “stabilization rather than elevation,” highlighting that while the upward move is a positive sign, the sector is far from robust growth.

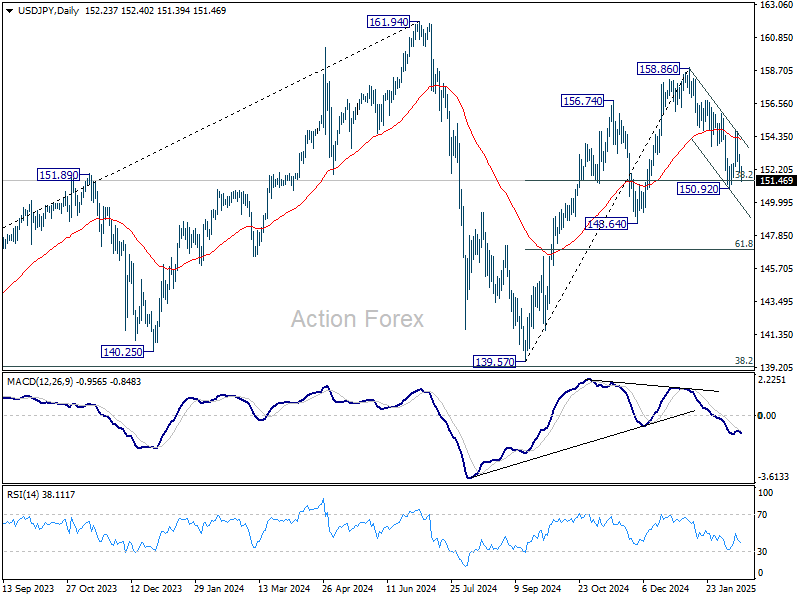

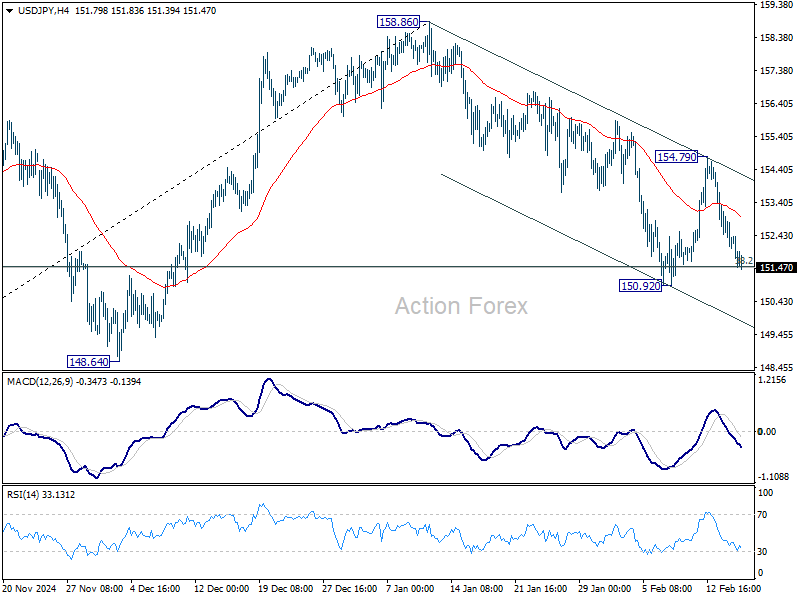

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.49; (R1) 152.96; More…

Intraday bias in USD/JPY remains neutral with focus on 38.2% retracement of 139.57 to 158.86 at 151.4. Strong rebound from there will maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.