Dollar’s selloff is accelerating as the week draws to a close, with investors continuing to react to the evolving trade policy stance from the White House. Wall Street posted broad gains overnight, as markets took relief in the fact that US President Donald Trump’s much-anticipated reciprocal tariff plan did not impose immediate trade restrictions. Instead, the administration will conduct a detailed review of tariff disparities before deciding on specific measures.

Despite the optimism in US equities, risk-on sentiment was not fully carried over into Asian session. While Hong Kong stocks extended recent strong gains, other major indexes struggled for direction, reflecting lingering caution. Investors remain wary of how the tariff situation will unfold, particularly as Trump’s trade team begins its assessment of countries with large trade surpluses with the US. This process is expected to take weeks, leaving room for further volatility in global markets.

The immediate focus now shifts to US retail sales data for January, which will provide fresh insights into consumer spending. Yet the figures are unlikely to have a significant impact on Fed expectations even with a major surprise. Fed has emphasized that its next move will be dictated by sustained trends rather than single data points. As a result, the Dollar’s downside pressure may persist, with market sentiment favoring risk assets.

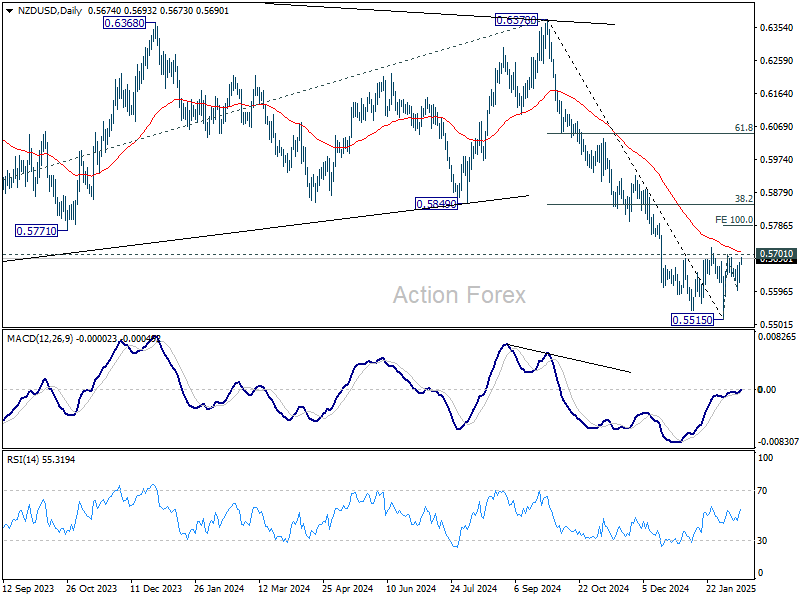

Among major currencies, New Zealand Dollar is leading the pack, buoyed by surprisingly strong manufacturing data. The economy is responding well to RBNZ’s aggressive rate cuts last year. While the central bank is still expected to deliver another 50bps reduction next week as the march to neutral continues, the resurgence in manufacturing could mean the central bank may not need to push rates into stimulatory territory.

Technically, as NZD/USD rebounds, focus is now on 0.5701 resistance. Firm break there will resume the rise from 0.5515, as a correction to fall from 0.63780. Further rally should then be seen to 38.2% retracement of 0.6378 to 0.5515 at 0.5848.

In Asia, at the time of writing, Nikkei is down -0.35%. Hong Kong HSI is up 2.48%. China Shanghai SSE is up 0.25%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is up 0.0018 at 1.351. Overnight, DOW rose 0.77%. S&P 500 rose 1.04%. NASDAQ rose 1.50%. 10-year yield fell -0.0112 to 4.525.

S&P 500 nears record high as Trump’s reciprocal tariff plan delays immediate action

U.S. stocks closed higher overnight as President Donald Trump unveiled his long-awaited reciprocal tariff plan without enforcing immediate measures. The market responded favorably to the lack of fresh tariffs, easing concerns about an abrupt escalation in trade tensions. In turn, Treasury yields and the U.S. dollar moved lower, reflecting a shift in sentiment away from safe-haven assets.

Trump’s directive instructs his administration to begin assessing tariff discrepancies between the US and its trading partner, including evaluation of non-tariff barriers. Also, the White House appears to be taking a targeted approach, prioritizing countries with large trade surpluses and high tariff rates on US exports.

Howard Lutnick, Trump’s nominee for Commerce Secretary, will lead the study, with findings expected by April 1. This extended timeline gives markets some breathing room and suggests that while trade tensions remain a concern, abrupt disruptions are unlikely in the near term.

Equities responded positively to the development, with S&P 500 rebounding strongly and edging closer to its all-time high of 6128.18. Technically, firm break of 6128.18 will resume the long term up trend, with 618% projection of 5119.26 to 6099.97 from 5773.31 at 6379.38 as next target.

NZ BNZ manufacturing rises to 51.4, first expansion in nearly two years

New Zealand’s manufacturing sector finally returned to expansion in January, with BusinessNZ Performance of Manufacturing Index surging from 46.2 to 51.4. This marks the first expansion in 23 months and the highest reading since September 2022. While the rebound is a positive sign for the economy, the index remains below its long-term average of 52.5, suggesting that the sector has yet to regain full strength.

Encouragingly, all sub-indexes entered expansionary territory. Production saw a significant jump from 42.7 to 50.9. Employment also rose from 47.7 to 50.2. New orders climbed from 46.8 to 50.9, while finished stocks and deliveries improved to 51.9 and 51.7, respectively.

BNZ’s Senior Economist Doug Steel highlighted the significance of the data, noting that the sector is “shifting out of reverse and into first gear.” He acknowledged the improvement as a relief after two difficult years but cautioned that the PMI still lags behind its historical average.

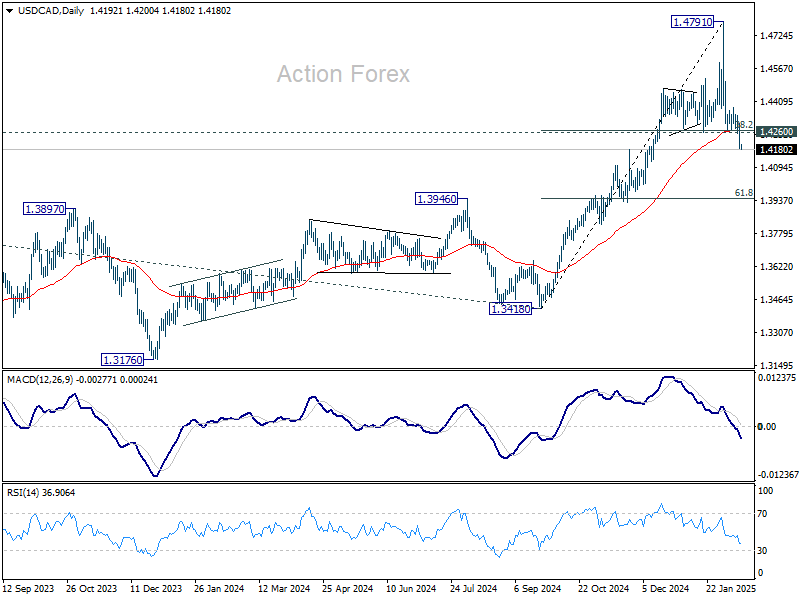

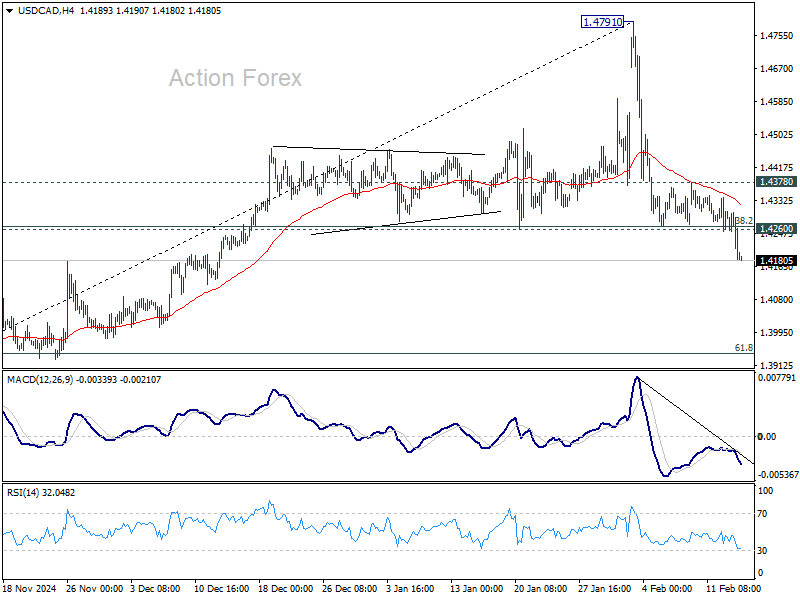

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4147; (P) 1.4229; (R1) 1.4274; More…

USD/CAD’s fall from 1.4791 resumed by breaking through 1.4260 cluster support decisively. The development suggests that deeper corrective is underway and turn intraday bias to the downside for 1.3946 cluster support (61.8% retracement at 1.3942). For, risk will stay on the downside as long as 1.4378 resistance holds, in case of recovery.

In the bigger picture, long term up trend is tentatively seen as resuming with breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.