Dollar rallied sharply in early US trading after inflation data came in hotter than expected, reinforcing expectations that Fed will maintain its restrictive policy stance for longer than previously anticipated. 10-year Treasury yield surged past 4.6%, extending its strong rebound from earlier in the week. US equity futures plunged, with DOW futures down around -1% as traders reassessed the likelihood of near-term rate cuts. The report shattered market hopes that the Fed might move forward with another rate cut by mid-year, instead strengthening the case for a prolonged pause.

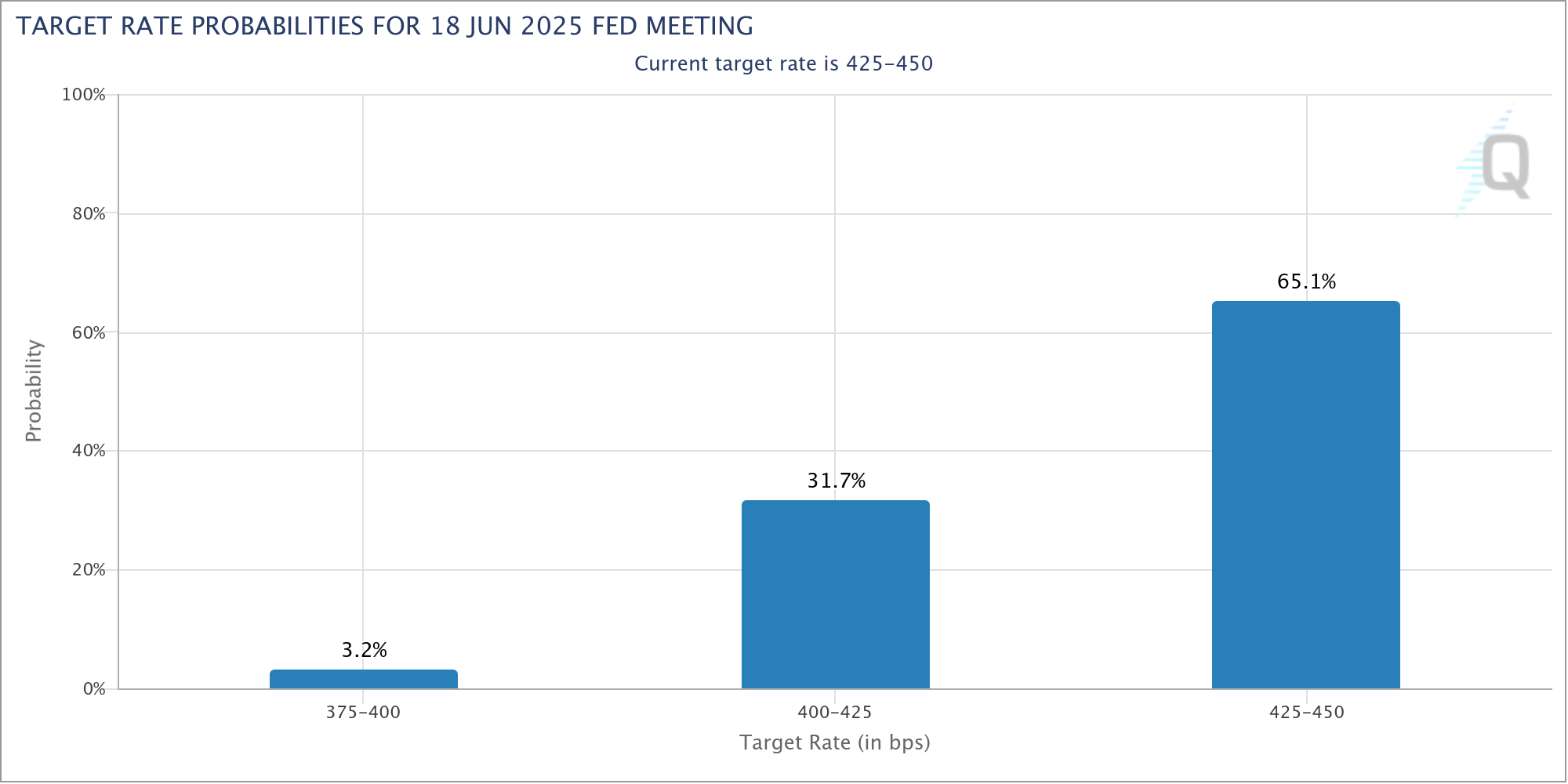

Both headline and core CPI surpassed forecasts, rising more than expected on both a monthly and annual basis. This marks a clear warning sign that inflation pressures remain persistent. Fed fund futures now imply a nearly 65% probability that Fed will keep rates unchanged through June, a notable increase from 50% just a day earlier. While it is still premature, it couldn’t be totally ruled out that another rate hike could be back on the table if inflationary pressures intensifies further.

US trade policy is another key wildcard for future price pressures. President Donald Trump’s tariff war is still in its early stages. Reports indicated that his administration is finalizing details for reciprocal tariffs. Trade analysts suggest that structuring these tariffs might be more challenging than anticipated, potentially delaying their rollout. However, if implemented aggressively, these tariffs could drive further price increases, creating additional inflationary risks that Fed would have to contend with.

The currency markets reacted decisively, with Dollar emerging as the strongest performer for the day, followed by Swiss Franc and Euro. Yen, however, is the worst performer, struggling under the weight of rising US yields. Australian and New Zealand Dollars also faced significant pressure, caught in the wave of risk aversion triggered by inflation fears and concerns over global trade tensions. Meanwhile, Canadian Dollar and British Pound traded with a more neutral stance, positioning in the middle of the performance spectrum.

In Europe, at the time of writing, FTSE flat. DAX is up 0.06%. CAC is down -0.18%. UK 10-year yield is up 0.071 at 4.583. Germany 10-year yield is up 0.043 at 2.477. Earlier in Asia, Nikkei rose 0.42%. Hong Kong HSI rose 2.64%. China Shanghai SSE rose 0.85%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0406 to 1.347.

US CPI rises to 3% in Jan, core CPI up to 3.3%

US headline CPI rose 0.5% mom in January, exceeding expectations of 0.3% mom and marking the fastest monthly pace since August 2023. Core CPI, which strips out food and energy prices, also outpaced forecasts (0.3% mom) at 0.4% mom, the highest since March 2024.

Key inflation drivers for the month included a 0.4% mom increase in shelter costs, a 1.1% mom jump in energy prices, and a 0.4% mom rise in food prices.

On an annual basis, CPI accelerated from 2.9% yoy to 3.0% yoy, beating expectations of 2.9% yoy and extending its upward streak for the fourth consecutive month.

Core CPI also climbed, rising from 3.2% yoy to 3.3% yoy, surpassing the projected 3.1% yoy. Energy prices rose 1.0% yoy, while food costs were up 2.5% yoy.

ECB’s Villeroy warns of negative impact from US tariffs

French ECB Governing Council member Francois Villeroy de Galhau cautioned that US President Donald Trump’s tariffs will “very likely” have a “negative effect” on the economy.

Speaking on France Culture radio, Villeroy criticized “protectionism is a seductive short-term policy, but in the long term it is a losing strategy.”

Despite trade tensions, Villeroy maintained an optimistic view on France’s economic resilience. He reaffirmed that the country is likely to avoid a recession in 2025.

Bank of France indicated on Tuesday that French GDP is on track to expand by 0.1% to 0.2% in the first quarter.

ECB’s Holzmann: Inflation risks rising, rate cuts require patience

Austrian ECB Governing Council member Robert Holzmann emphasized caution regarding rate cuts, citing renewed inflation risks from tariffs.

Speaking to CNBC, Holzmann noted that while inflation pressures had previously “somewhat dissipated,” the latest developments, particularly increased trade frictions, pose fresh threats to price stability. As a result, policymakers must be careful in their approach on policy easing.

Holzmann explained that while increased trade barriers may reduce economic growth, they also contribute to inflationary pressures. “We will have to be more patient,” he stated.

Addressing speculation about a larger 50 basis point rate cut, Holzmann dismissed the idea, arguing that ECB’s mandate is to manage inflation, not stimulate growth.

“Using the interest rate in order to initiate a higher growth is not the way how we should work,” he stated.

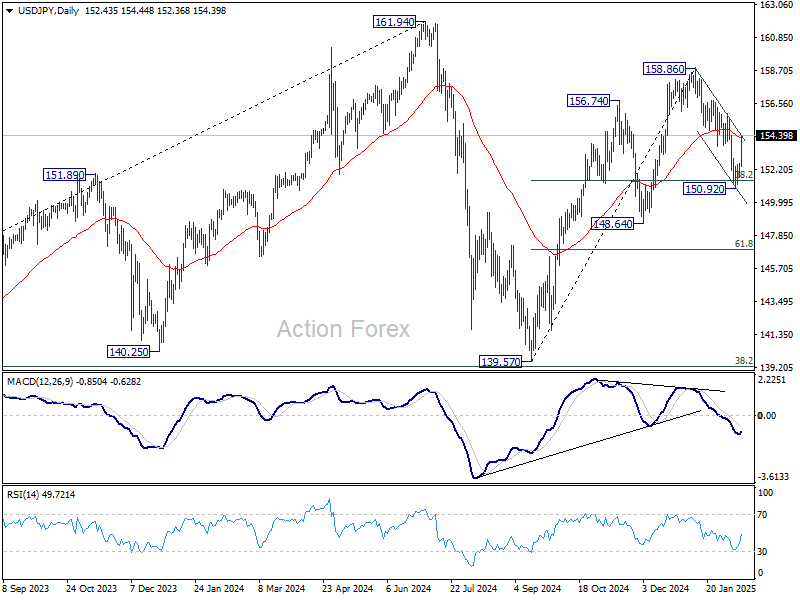

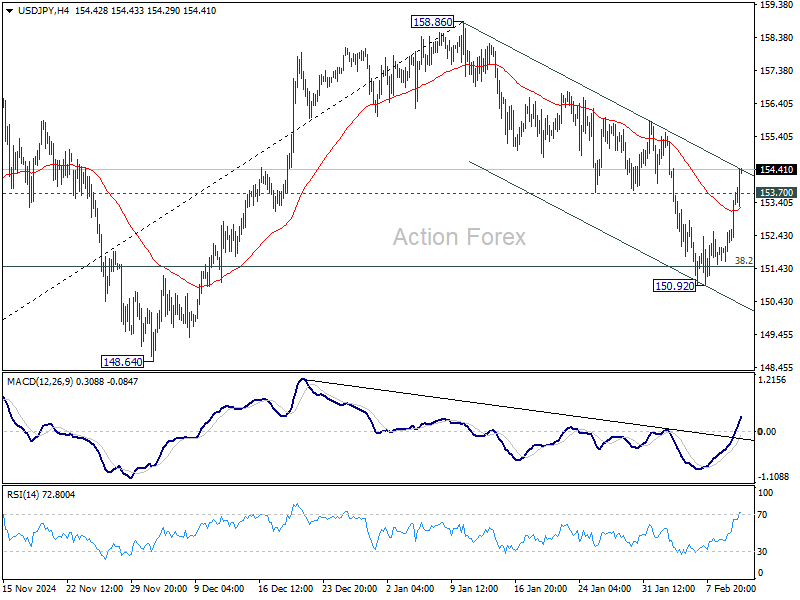

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.90; (P) 152.25; (R1) 152.86; More…

USD/JPY’s strong break of 153.70 support turned resistance should confirm that corrective pull back from 158.86 has completed at 150.92. That came after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.49. Intraday bias is back on the upside for retesting 158.86. Firm break there will resume whole rally from 139.57 to retest 161.94 high. For now, risk will stay on the upside as long as 150.92 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.