Trading in the forex markets has been relatively subdued today, with major currency pairs and crosses remaining within Friday’s range. There was some initial reactions to the latest news of US tariffs on metals, but the impact has faded quickly. Dollar is currently mildly stronger in tight range and Yen is on the softer side. Broader market sentiment also appears stable, as European equities trade in positive territory and US futures indicate a slightly higher open. Meanwhile, Gold is the standout asset, continuing its record-breaking rally with steady momentum.

Looking ahead, Australian consumer and business confidence data will be a key focus in the upcoming Asian session. Market expectations for RBA to begin rate cuts at its February 17-18 meeting have surged, with a 93% probability priced into money markets. The country’s major banks are also aligning with this view, citing the softer-than-expected Q4 trimmed mean CPI as a signal that inflation is sustainably cooling. The upcoming sentiment indicators will provide further clues on whether consumers and businesses are adjusting expectations for looser monetary policy.

Technically, AUD/JPY is back pressing 61.8% projection of 102.39 to 95.50 from 98.75 at 94.49, after prior recovery was rejected by 55 4H EMA. Sustained break of 94.49 will pave way to 100% projection at 91.86. Also, outlook will stay cautiously bearish as long as 96.74 resistance holds, in case of recovery.

In Europe, at the time of writing, FTSE is up 0.68%. DAX is up 0.47%. CAC is up 0.21%. UK 10-year yield is down -0.029 at 4.452. Germany 10-year yield is down -0.008 at 2.367. Earlier in Asia, Nikkei rose 0.04%. Hong Kong HSI rose 1.84%. China Shanghai SSE rose 0.56%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0136 to 1.316.

Eurozone Sentix rises to -12.7, but inflation keeps ECB in check

Eurozone investor sentiment showed signs of improvement in February, with the Sentix Investor Confidence Index rising from -17.7 to -12.7, surpassing expectations of -16.4. This also marks the highest reading since July 2024, signaling a tentative shift in market sentiment. Current Situation Index also improved, climbing from -29.5 to -25.5, while Expectations Index made an even more notable leap from -5 to 1, also reaching its highest level since July last year.

Sentix noted that the Eurozone economy is “trying to emerge from the crisis,” with some early signs of stabilization. However, Germany’s economic struggles continue to act as a drag on the broader region, described as a “lead weight” on the bloc’s recovery. Despite this, optimism is growing that a potential shift in German leadership could usher in a more pro-business policy stance, which could help lift economic prospects in the months ahead.

One key takeaway from the report is the diminishing likelihood of aggressive monetary easing from ECB. With investor sentiment improving and the economic outlook brightening, “hopes of more significant support measures from the ECB are also dwindling.”

Inflation outlook remains a lingering concern, preventing ECB from committing to deeper rate cuts. Sentix’s “Inflation” theme index remained at -11 points, signaling persistent price pressures.

China’s CPI picks up to 0.5%, but factory prices remain stuck in deflation

China’s consumer inflation accelerated at the start of 2025, with CPI rising from 0.1% yoy to 0.5% yoy in January, slightly exceeding market expectations of 0.4%. This marked the fastest annual increase in five months. On a monthly basis, CPI surged 0.7% mom, the strongest rise in over three years.

Core inflation, which strips out food and fuel prices, edged up from 0.4% yoy to 0.6% yoy, reflecting a modest pickup in underlying demand. Food prices climbed by 0.4% yoy, while non-food categories also posted a 0.5% yoy increase.

However, despite these gains, consumer inflation remains well below the government’s target, with full-year 2024 CPI growth coming in at just 0.2%, the lowest since 2009, and reinforcing the persistent weakness in domestic consumption.

Meanwhile, producer prices remained firmly in deflationary territory. PPI held steady at -2.3% yoy in January, missing expectations of a slight improvement to -2.2% yoy. This marks the 28th consecutive month of factory-gate deflation, highlighting ongoing struggles within the manufacturing sector and pricing pressures stemming from weak external demand and excess capacity.

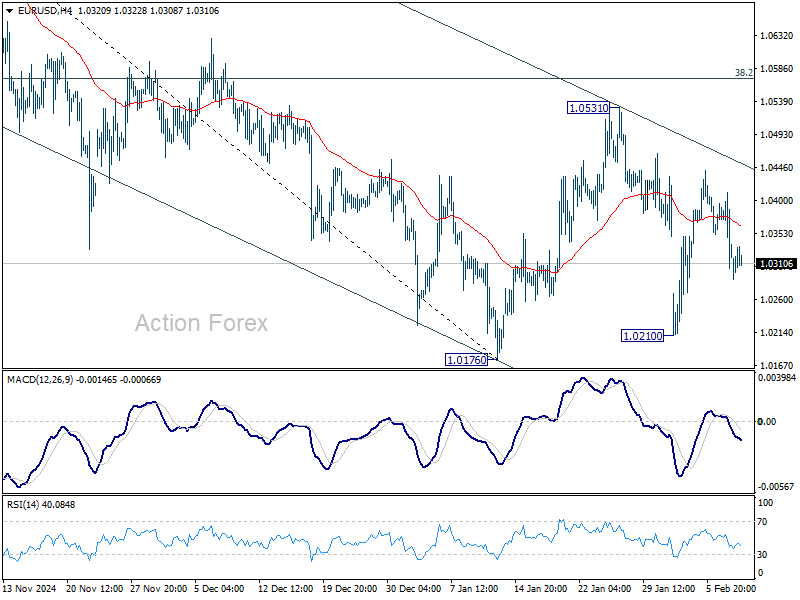

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0289; (P) 1.0345; (R1) 1.0383; More…

EUR/USD is still bounded in consolidation from 1.0176 and intraday bias remains neutral. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.