Yen continues to dominate the forex market this week, additionally supported by further decline in US and European benchmark yields overnight. The persistent strength in Yen is being reinforced by hawkish rhetoric from a known hawkish BoJ board member, who reiterated calls for a gradual rate hike toward the 1% neutral level. While this stance isn’t new, the reaffirmation signals a continued push within the BoJ for higher rates. Recent economic data, including strong wage growth and Tokyo inflation, have provided additional support for the case of tighter monetary policy. As a result, Yen remains anchored as a favored currency, particularly amid falling yields in global markets.

Meanwhile, market attention shifts to the British Pound ahead of today’s BoE policy announcement. A widely expected 25bps rate cut is already priced in, but the key drivers for Sterling will be the updated economic forecasts, voting split, and guidance from Governor Andrew Bailey. The ongoing debate over stagflation risks in the UK could lead to a further division within the Monetary Policy Committee. Any significant disagreement among policymakers would add further uncertainty to BoE’s rate path and could lead to Sterling volatility.

Across the broader forex market, Yen remains the best performer of the week, followed by Canadian Dollar and Swiss Franc. On the other end of the spectrum, Dollar remains under pressure as the weakest currency, trailed closely by Euro and New Zealand Dollar. The Australian Dollar and Sterling are hovering in the middle.

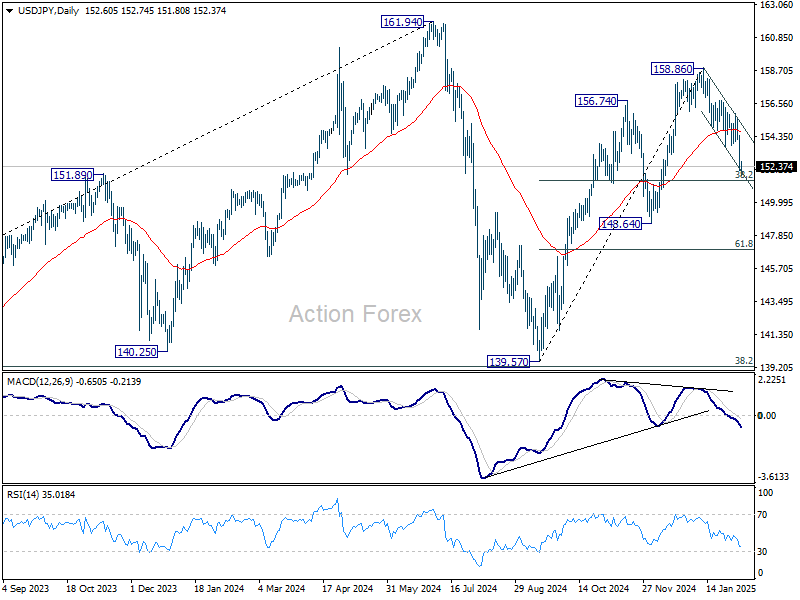

Technically, the anticipated rebound in US 10-year yields from 55 D EMA failed to materialize, with the yield accelerated further overnight to close at 4.422. The next key support level lies at 38.2% retracement of 3.603 to 4.809 at 4.348. Strong rebound from this level, coupled with decisive break above 4.590 resistance, would help reaffirm the broader bullishness. However, a clear break below 4.348 would shift the focus toward the 61.8% retracement level at 4.063%, raising the risk of a deeper correction. Extended fall in 10-year yield could drag USD/JPY through corresponding 38.2% retracement of 139.57 to 158.86 at 151.49 too.

In Asia, at the time of writing, Nikkei is up 0.55%. Hong Kong HSI is up 0.64%. China Shanghai SSE is up 0.81%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is down -0.012 at 1.272. Overnight, DOW rose 0.71%. S&P 500 rose 0.39%. NASDAQ rose 0.19%. 10-year yield fell -0.091 to 4.422.

BoE to cut 25bps, focus on MPC split and stagflation risks

BoE is widely expected to lower interest rates by 25bps to 4.50% today, marking its third cut in the current cycle. The central bank is likely to maintain a cautious stance, reinforcing its guidance of a “gradual” approach, which suggests a pace of four quarter-point cuts throughout 2025.

The Monetary Policy Committee’s vote split will be a key focus, as divisions among policymakers could influence BoE’s forward guidance. Known hawk Catherine Mann may dissent and argue for keeping rates steady, while dovish member Swati Dhingra could push for a more aggressive 50bps cut. A wider split would highlight internal uncertainty over the pace of easing.

Alongside the rate decision, BoE will release its updated quarterly Monetary Policy Report, which is expected to reflect downward revisions to growth projections for 2025-2027. However, inflation forecasts, at least for 2025, could be revised higher. Such a combination would reinforce concerns over stagflation, a scenario where sluggish growth coincides with persistent inflationary pressures.

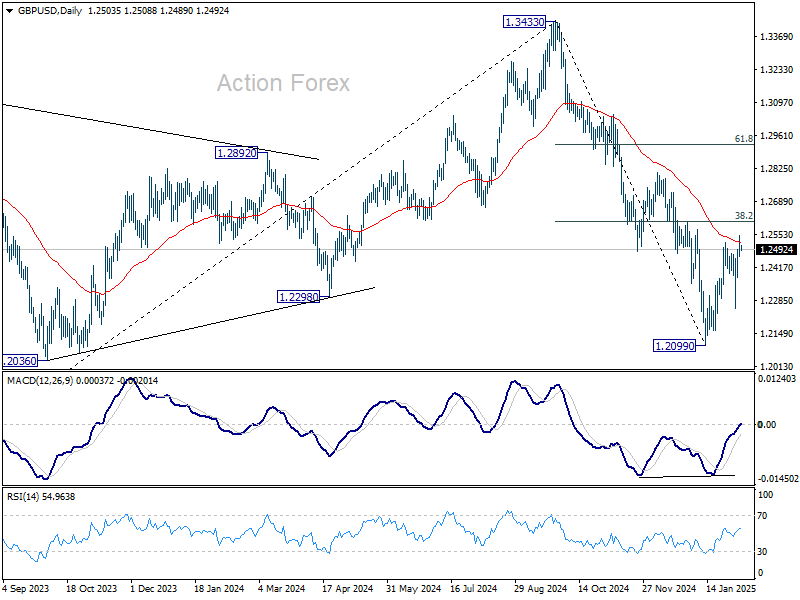

GBP/USD is hovering near a critical technical resistance zone ahead of BoE decision. The zone include 55 D EMA (now at 1.2522) and 38.2% retracement of 1.3433 to 1.2099 at 1.2609. Firm rejection from this zone would reinforce the view that recent price action from 1.2099 remains corrective, keeping the broader bearish trend intact. In this case, decline from 1.3433 should resume through 1.2099 low at a later stage.

BoJ’s Tamura advocates rate hike to 1% by late fiscal 2025

BoJ board member Naoki Tamura, a known hawk, reinforced his stance on the need for tighter monetary policy, stating that Japan’s short-term interest rates should rise to at least 1% by the second half of fiscal 2025 to mitigate inflation risks.

Tamura explained that inflationary pressures are mounting, necessitating a shift away toward a more neutral rate. He highlighted that by late fiscal 2025, the Japanese economy is expected to reach a point where the 2% inflation target can be considered sustainably achieved, supported by broad-based wage increases, including among smaller firms.

“Bearing in mind that short-term interest rates should be at 1% by the second half of fiscal 2025, I think the Bank needs to raise rates in a timely and gradual manner, in response to the increasing likelihood of achieving its price target,” he said.

Australia’s NAB business confidence improves, but profitability weakens

Australia’s NAB Business Confidence rose from -7 to -4 in Q4, reflecting a slight improvement in sentiment. However, Business Conditions remained unchanged at 3, as trading conditions slipped from 6 to 5, and profitability turned negative from 0 to -1. Employment conditions as steady at 3.

Forward-looking indicators showed a mixed picture. Expected business conditions for the next three months edged lower, but sentiment for the 12-month horizon improved by five points, aligning with a three-point increase in capital expenditure plans, suggesting firms are cautiously optimistic about long-term prospects.

Cost pressures moderated, with labor cost growth slowing to 0.9% qoq from 1.2%, and purchase costs easing to 0.7% qoq from 1.0%. Retail price growth also softened to 0.5% qoq from 0.7%, though overall product price growth remained stable at 0.4% qoq, indicating ongoing margin pressure despite easing input costs. Wage costs remained the top concern for businesses, while demand constraints and labor shortages persisted as key challenges.

Goolsbee warns Fed may struggle to distinguish tariff-driven inflation from overheating

Chicago Fed President Austan Goolsbee cautioned that a “series of new challenges to the supply chain”, ranging from natural disasters to trade policy shifts, could create fresh inflationary pressures.

He highlighted the increasing risks from events like tariffs and trade wars, hurricanes, port closures, geopolitical tensions, and labor strikes, all of which could complicate the inflation outlook in 2025.

A key concern for Fed, Goolsbee noted, is differentiating between inflation stemming from economic overheating versus price increases caused by new tariffs. This distinction will be critical in determining the Fed’s policy response.

Goolsbee also compared the current situation to the 2018 trade tensions under President Donald Trump, noting that while companies previously shifted production out of China, further adjustments could be more challenging this time. The remaining imports from China may be less replaceable.

“In that case, the impact on inflation might be much larger this time,” Goolsbee noted.

Separately, Fed Vice Chair Philip Jefferson signaled that the central bank is in no rush to adjust its policy stance as it assesses the economic impact of the Trump administration’s policy policies on tariffs, immigration, deregulation and taxes. “We can be patient and wait to see the net effect of any policy changes by the current administration,” he said.

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.66; (P) 153.06; (R1) 154.00; More…

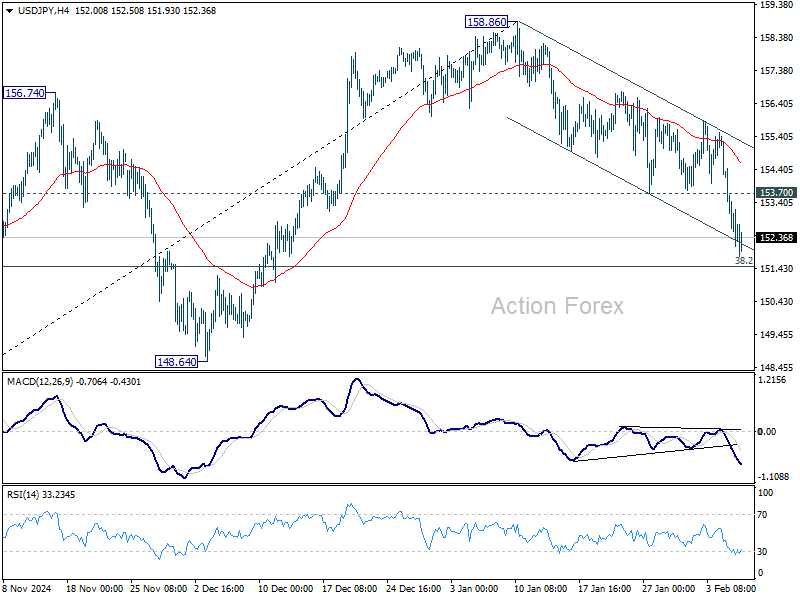

USD/JPY’s fall from 158.86 is in progress and intraday bias stays on the downside for 38.2% retracement of 139.57 to 158.86 at 151.49. Strong support could be seen from there to complete the corrective fall from 158.86. Break of 153.70 minor resistance will turn intraday bias back to the upside for rebound. However, sustained break of 151.49 will raise the chance of bearish reversal.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.