Japanese Yen gained significant ground in the Asian session, supported by stronger-than-expected nominal wage growth, which bolstered the likelihood of further BoJ rate hikes. Additionally, continued rise in real wages for the second consecutive month, despite being largely driven by seasonal bonuses, adds to the argument that wage pressures could help sustain inflation near the 2% target.

Supporting this outlook, BoJ monetary affairs director Kazuhiro Masaki told parliament that the central bank is prepared to continue adjusting monetary support and raising rates if underlying inflation progresses toward its 2% target. These remarks reaffirm the expectation that Japan’s interest rate normalization will proceed gradually but steadily this year.

While Yen leads gains in the forex market, overall sentiment is mixed, with trade war concerns temporarily fading into the background. Canadian Dollar is currently the strongest performer this week, followed by Yen and Swiss Franc. Dollar lags behind as the weakest, joined by Euro and New Zealand Dollar. Sterling and Australian Dollar are treading a middle ground .

With trade-related uncertainty easing, attention is now shifting back toward key economic events. US ISM Services PMI is due later today. Tomorrow, BoE is expected to announce a 25bps rate cut, but the MPC voting split and economic projections will be crucial in setting future rate expectations. To close the week, US Non-Farm Payrolls and Canada’s employment report will be in focus on Friday.

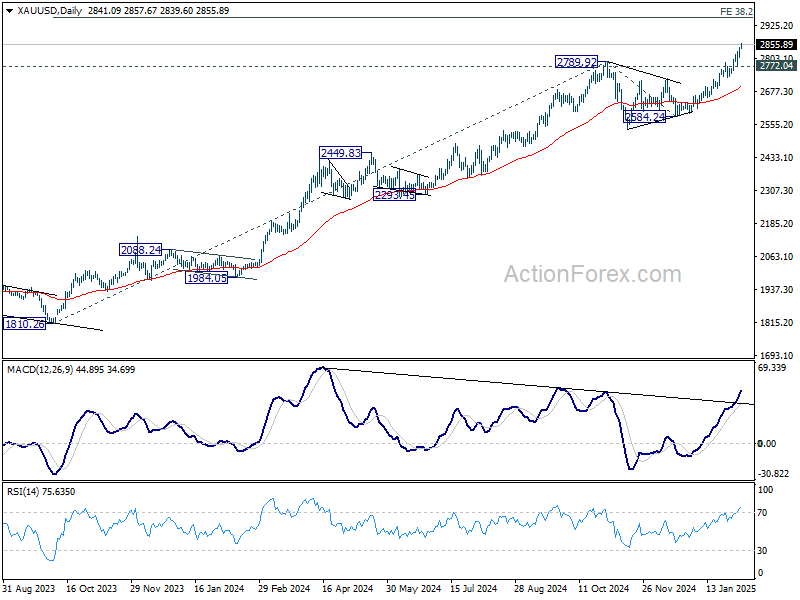

Technically, Gold’s record run continues with strong momentum and remains on track to 3000 psychological level, which is close to 38.2% projection of 1810.26 to 2789.92 from 2584.24 at 3074.07. Attention is on whether Gold would lose momentum on overbought condition as it approaches this level. But in any case, outlook will stay bullish as long as 2772.04 support holds.

In Asia, at the time of writing, Nikkei is down -0.10%. Hong Kong HSI is down -0.69%. China Shanghai SSE is down -0.36%. Singapore Strait Times is down -0.14%. Japan 10-year JGB yield is up 0.0191 at 1.295. Overnight, DOW rose 0.30%. S&P 500 rose 0.72%. NASDAQ rose 1.35%. 10-year yield fell -0.030 to 4.513.

Fed’s Jefferson and Daly signal no urgency for rate cuts

Fed Vice Chair Philip Jefferson reaffirmed the cautious approach to policy easing, stating that while a “gradual reduction” in monetary policy restraint towards neutral remains the most likely scenario, there is no urgency to change the current stance.

“I do not think we need to be in a hurry to change our stance,” he said in a speech overnght.

He emphasized that policy decisions will continue to be guided by incoming data and the evolving economic outlook, noting that monetary policy is “not on a preset course.”

Jefferson outlined a “range of scenarios” for future policy moves. If economic activity remains robust and inflation fails to sustainably decline toward 2% target, Fed could maintain its restrictive stance for longer. Conversely, if the labor market weakens unexpectedly or inflation cools faster than expected, the central bank may need to ease policy at a quicker pace.

Meanwhile, San Francisco Fed President Mary Daly echoed similar sentiments, describing the US economy as “in a very good place.” She emphasized that the central bank is in a strong position to “wait and see” before making any policy moves.

Japan’s nominal wage growth surges 4.8% yoy in Dec, real wages rise for second month

Japan’s labor market showed strong wage growth in December, with labor cash earnings surging 4.8% yoy, significantly above expectations of 3.8% yoy and accelerating from 3.9% yoy in the prior month. This marks the 36th consecutive month of annual wage increases.

Regular pay, which includes base salaries, rose 2.7% yoy, while special cash earnings—mainly reflecting winter bonuses—jumped 6.8% yoy, providing an additional boost to workers’ disposable income.

Real wages, which adjust for inflation, climbed 0.6% yoy, marking the second straight month of positive growth. This improvement comes despite a notable acceleration in consumer inflation, with the price index used to calculate real wages—excluding rent but including fresh food—rising 4.2% yoy, up from 3.4% yoy in November and reaching the highest level since January 2023.

China’s Caixin PMI services PMI drops to 51.0

China’s Caixin Services PMI slipped to 51.0 in January, down from 52.2 and below expectations of 52.3. PMI Composite also edged lower from 51.4 to 51.1, marking a four-month low, as both manufacturing and services sectors struggled to gain momentum.

According to Caixin Insight Group, while supply and demand conditions showed improvement, services growth lagged behind, pointing to weaker consumer activity.

Wang Zhe, Senior Economist added, “Employment in both sectors fell significantly, and overall price levels remained subdued, particularly factory-gate prices in manufacturing.”

New Zealand’s unemployment rate rises to 5.1%

New Zealand’s labor market softened further in Q4, with unemployment rate climbing from 4.8% to 5.1%, in line with expectations and marking the highest level since 2016, excluding the brief spike following the 2020 Covid lockdown.

Employment fell by -0.1% in the quarter, slightly better than the expected -0.2% decline, but still reflecting ongoing weakness in job creation. Meanwhile, wage growth continued to moderate, with the labor cost index rising 0.6% qoq, bringing the annual rate down to 3.3% from 3.8%.

The latest data supports the case for further monetary easing by RBNZ, which remains committed to swiftly bringing the OCR down from the current 4.25% toward neutral level. A 50bps rate cut is still widely anticipated at the upcoming policy meeting this month.

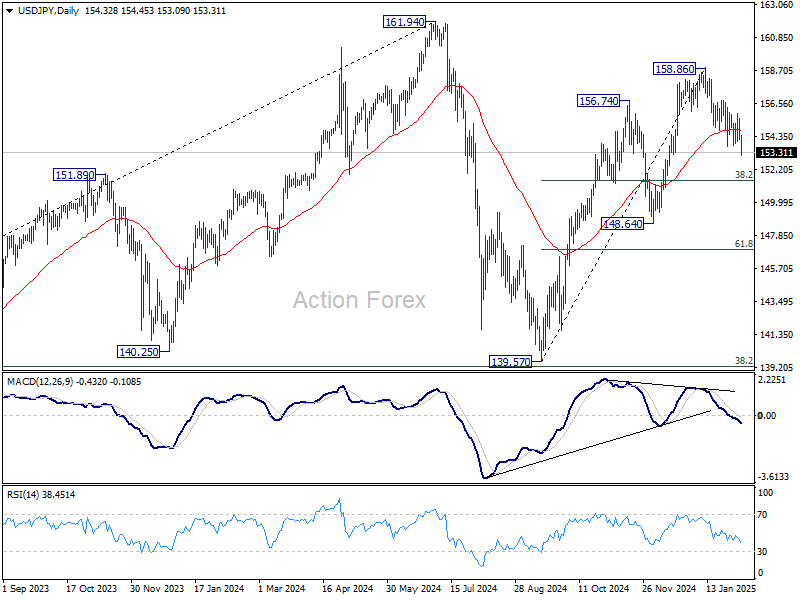

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.84; (P) 154.68; (R1) 155.18; More…

USD/JPY’s fall from 158.86 short term top resumed by breaking through 153.70 and intraday bias is back on the downside. Deeper decline should be seen to 38.2% retracement of 139.57 to 158.86 at 151.49. Strong support could be seen from there to bring rebound. But further fall will remain in favor as long as 155.51 resistance holds, in case of recovery. Sustained break of 151.49 will raise the chance of bearish reversal.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.