Global markets remain stable as US session begins, with sentiment lifted by the delay of tariffs on Canada and Mexico. Nonetheless, investors remain cautious about ongoing tensions between the US and China, as Washington’s additional 10% tariffs on Chinese imports have taken effect. So far, there has been no scheduled phone call between US President Donald Trump and Chinese President Xi Jinping, raising uncertainty over whether negotiations will take place anytime soon.

China responded swiftly with retaliatory tariffs of up to 15% on U.S. coal and liquefied natural gas, along with a 10% increase in duties on crude oil, farm equipment, and select automobiles, set to begin on February 10. Additionally, Beijing has opened an antitrust investigation into Google, signaling that trade tensions may extend beyond tariffs and into regulatory action against US firms operating in China.

Unlike the previous trade disputes during Trump’s first term, the current tariff measures appear to be more of a bargaining tool for non-trade-related concessions, making a near-term resolution less likely. Given Beijing’s firm stance, the US may keep the tariffs in place while shifting focus to another geopolitical or economic issue. As a result, investors should prepare for prolonged trade frictions, with potential spillover effects into other sectors.

In the markets, one development to note is the strong bounce in US 10-year yield as safe-haven flows reversed. Technically, 55 D EMA (now at 4.478) could be a spot to provide enough support to end the corrective pull back from 4.809. Break of 4.664 resistance would argue that rise from 3.603 is ready to resume through 4.809. In case the correction extends, downside should be contained by 38.2% retracement of 3.603 to 4.809 at 4.348. Dollar would likely follow yield for its next move, in particular in USD/JPY.

In Europe, at the time of writing, FTSE is down -0.10%. DAX is up 0.22%. CAC is up 0.36%. UK 10-year yield is up 0.062 at 4.551. Germany 10-year yield is up 0.038 at 2.429. Earlier in Asia, Nikkei rose 0.72%. Hong Kong HSI rose 2.83%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.0265 to 1.276.

BoJ’s Ueda prioritizes underlying inflation trends, not short-term volatility

BoJ Governor Kazuo Ueda reiterated the central bank’s commitment to achieving its 2% inflation target on a sustained basis, emphasizing that the focus remains on underlying inflation rather than temporary price fluctuations.

Speaking before parliament, Ueda highlighted that BoJ filters out one-off factors such as fuel and volatile fresh food prices when assessing inflation trends.

However, he acknowledged “that process at times could be difficult”, reinforcing the need for careful analysis before making policy adjustments.

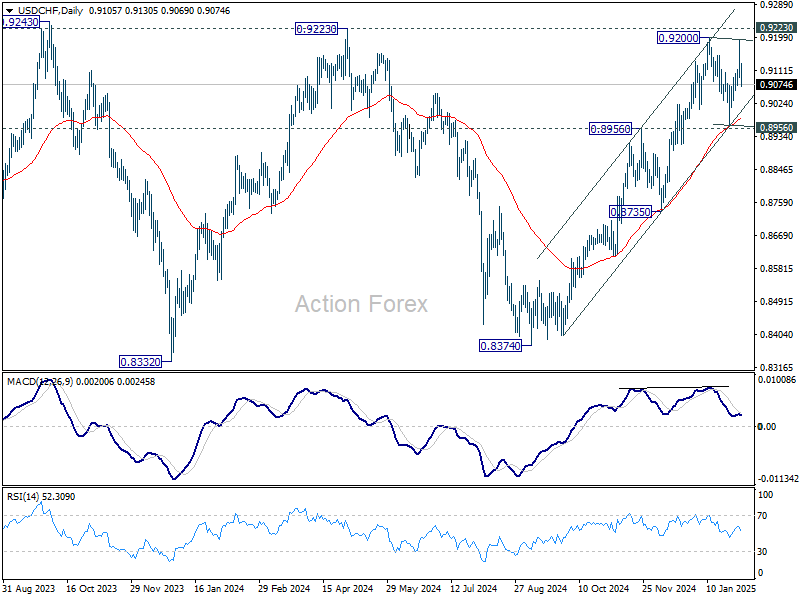

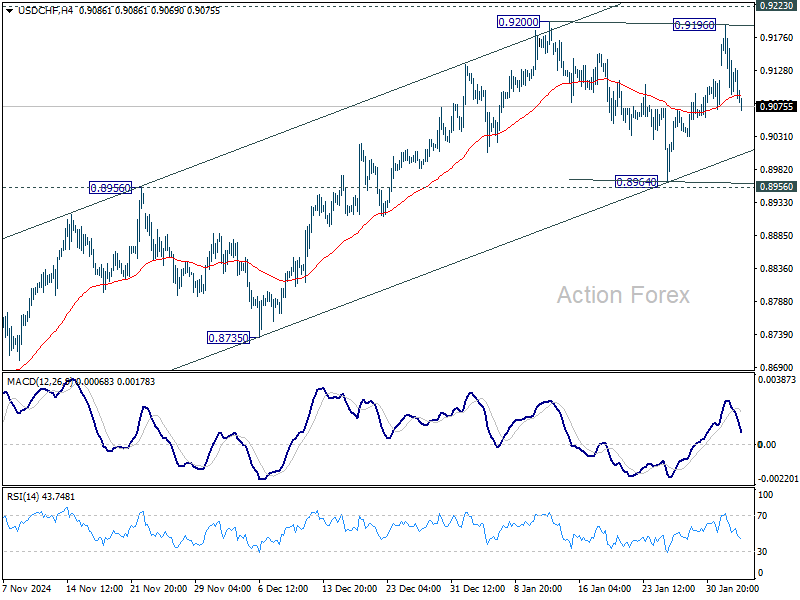

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9065; (P) 0.9131; (R1) 0.9169; More…

USD/CHF dips mildly today as consolidation from 0.9200 extends with another downleg. Deeper fall could be seen but outlook will stay bullish as long as 0.8956/64 support holds. Firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.