Dollar ended the week as the worst-performing major currency, largely weighed down by strong risk-on sentiment that took hold after President Donald Trump’s first week in office. Investors had anticipated more aggressive trade measures from the new administration, but Trump instead struck a relatively softer tone on tariffs, leading to improved risk appetite in equities and other growth-sensitive assets. Meanwhile, the extended consolidation in US Treasury yields offered little help to the greenback.

The delayed implementation of tariffs has been a major factor buoying market optimism. In the absence of immediate trade disruptions, stocks continued their robust rally, while Treasury yields remained in a rangebound consolidation phase. Until Trump shows concrete follow-through on his tariff threats, the dominant trends of rising equity prices and a softer Dollar appear likely to remain intact.

Among the other major currencies, Yen finished the week as the second worst performer. Briefly, anticipation of a BoJ rate hike lent the yen some support, but once the hike was finally delivered, Yen returned to a downbeat mode as risk-seeking flows dominated. Swiss Franc was also soft, lacking safe-haven demand in this upbeat environment. But Loonie was the third worst performer, dragged down by specific concerns that Trump’s tariff policies would target key Canadian exports.

On the other side of the spectrum, identifying a clear winner among Euro, Sterling, Aussie, and Kiwi is a bit difficult. Sterling may have a slight edge, helped by reduced US trade threats and encouraging PMI reports. Euro is similarly supported by easing tariff concerns and improving economic indicators. At the same time, Aussie and Kiwi have found a boost from Trump’s softer stance on China, coupled with a favorable risk environment. It may take another week or two for these four to sort out their relative strength, but for the moment, they continue to benefit from Dollar weakness and positive sentiment across global markets.

US Stocks Soar to Record as Trump’s First Week Brings Tariff Delays

US stocks extended their strong near-term rally last week, as S&P 500 notched fresh record highs while DOW and the NASDAQ Composite followed closely behind. The robust performance across all three major indexes, which each notched their second consecutive positive week, signals a resurgence in the bull market after a brief December pullback. S&P 500 and Nasdaq rose by 1.7%, while DOW outperformed with a 2.2% weekly gain, reflecting broad-based optimism among investors.

From our perspectives, the major factor driving this renewed optimism is President Donald Trump’s restraint on initiating tariffs, at least so far. Despite months of trade-related rhetoric, the first week of his presidency ended without any clear action to impose levies on major U.S. trading partners, even including China. Trump’s softer tone, particularly when asked about tariffs on China—he told Fox News “I’d rather not have to use it”—has bolstered hopes that strict trade measures might be delayed, imposed in a more controlled way, or even significantly scaled back.

Indeed, the earliest date for tariff implementation against Canada, Mexico, and China is February 1, but there is no guarantee that any decision will be finalized that quickly. Further delays remain plausible. Tariffs on other trading partners might not even come until after a formal review, following the timeline laid out in a presidential memorandum. Given that reports from these reviews are due on April 1, additional tariff changes, if they occur, may not take effect until 30 to 60 days after that date—pushing any significant shifts into late spring or early summer. This timeline has helped calm fears of a near-term inflation spike, which, in turn, reduces the odds of Fed feeling compelled to return to monetary policy tightening.

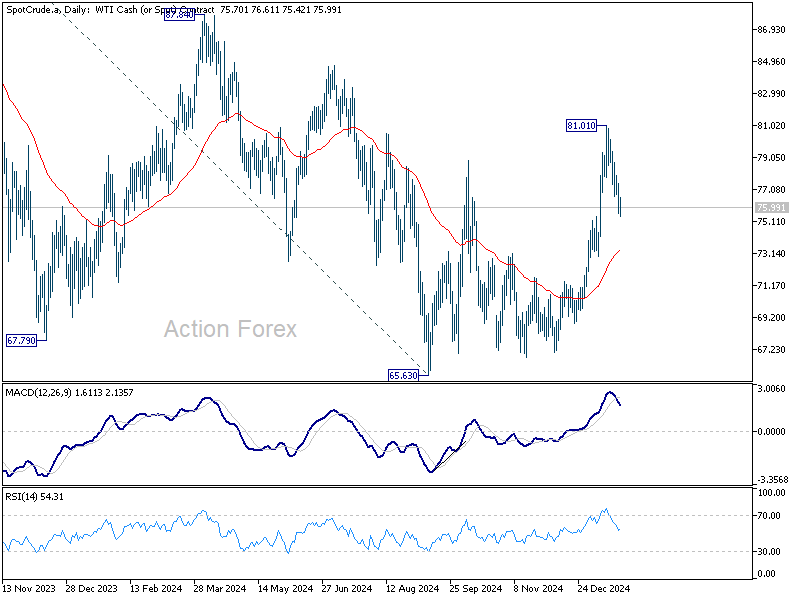

Compounding the positive sentiment is Trump’s commentary at the World Economic Forum in Davos. He emphasized his view that lower oil prices should prompt the Fed to cut interest rates “immediately”—though most economists and market participants view this more as presidential wishful thinking rather than a credible policy signal. In reality, oil prices only retreated slightly last week, and technical indicators still suggest that crude has more room to rise. In particular, WTI (West Texas Intermediate) has maintained the robust uptrend since December, with prospect of continued upside.

Geopolitical factors could also buoy oil prices further, especially ongoing tensions centered on Russia and Iran. According to Citi, “heightened, sustained geopolitical risks in Iran/Russia-Ukraine could potentially wipe out the 2025 oil balance surplus.” Citi went on to revise its quarterly Brent forecasts upward to USD 75 per barrel in the first quarter, USD 68 in the second, USD 63 in the third, and USD 60 in the fourth. These projections suggested that any near term pullback in oil might remain shallow, which complicates the global inflation picture.

Meanwhile, market traders are largely ignoring Trump’s request for Fed to cut rates. Fed funds futures currently project around a 98% probability that the central bank will keep its benchmark rate steady at 4.25-4.50% during the upcoming meeting at the end of January. The futures market also prices in roughly a 70% chance of one more rate cut in June, to a 4.00-4.25% range, but indicates no further easing for the rest of 2025 and well into 2026.

Unless inflation surprises to the upside—whether via unexpected tariff moves or a significant oil price shock—monetary policy looks set to remain on a cautious but steady path down. For now, that sense of stability, combined with a lack of immediate trade disruptions, continues to support the bullish sentiment on Wall Street.

Dollar Index Extends Pullback as Yields Consolidate and Stocks Surge

S&P 500’s up trend resumed last week by breaking through 6099.97 resistance. Further rally is expected as long as 55 D EMA (now at 5938.64) holds, in case of retreat. Next target is 61.8% projection of 5119.26 to 6099.97 from 577.3.31 at 6379.38.

In the bigger picture, the key question is whether S&P 500 could power through long term channel resistance (now at around 6400) and sustain above there. If it could, the up trend could further accelerate towards 138.2% projection of 2191.86 to 4818.62 from 3491.58 at 7121.76 in the medium term

10-year yield recovered after initial dip to 4.552 but overall outlook is unchanged. Consolidation pattern from 4.809 should continue with risk of deeper pull back to 55 D EMA (now at 4.458) and possibly below. But strong support should be seen from 38.2% retracement of 3.603 to 4.809 at 4.348 to contain downside and bring rebound. Rise from 3.603 is expected to resume at a later stage to retest 4.997 high.

Dollar’s correction from 110.17 extend lower and breached 55 D EMA (now at 107.32). While some support might be seen from 55 D EMA to bring recovery, risk will continue to stay on the downside as long as 110.17 holds. Correction/consolidation in yields and strong risk-on sentiment would continue to give Dollar Index some pressure in the near term.

Nevertheless, while deeper fall is in favor, downside should be contained by 38.2% retracement of 100.15 to 100.17 at 106.34 to bring rebound. Rise form 100.15 is expected to resume through 110.17 to retest 114.77 high at a later stage.

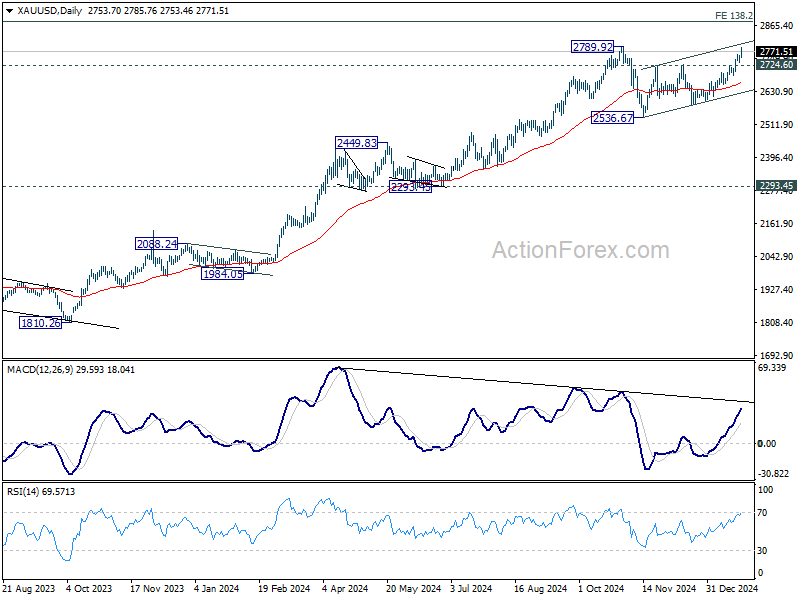

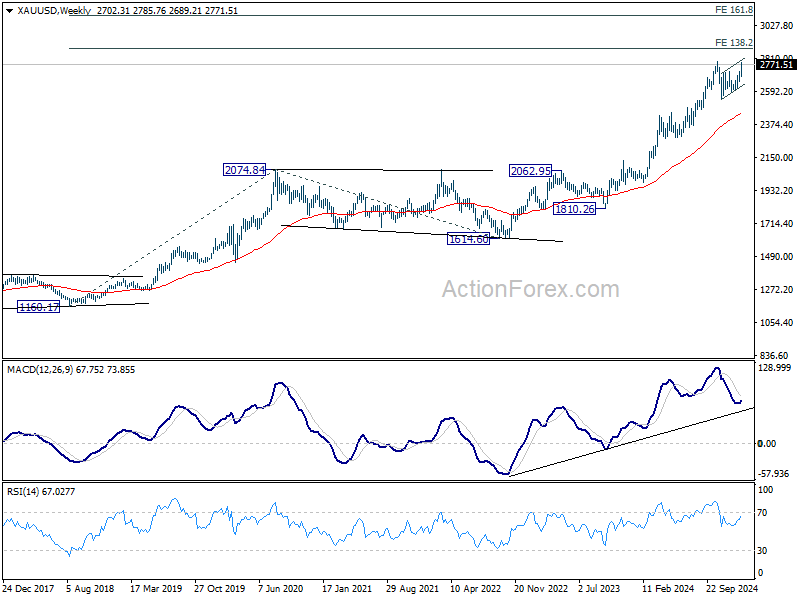

Gold is among the biggest beneficiaries of Dollar’s near term weakness. The pickup in momentum as seen in D MACD is raising the chance of up trend resumption. Decisive break of 2789.92 would extend the long term up trend to 138.2% projection of 1160.17 to 2074.84 from 1614.60 at 2878.67, or even further to 161.8% projection at 3094.53.

Nevertheless, firm break of 2724.60 resistance turned support should revive our original view, and extend the corrective pattern from 2789.92 with a third leg towards 2536.67 support before up trend resumption.

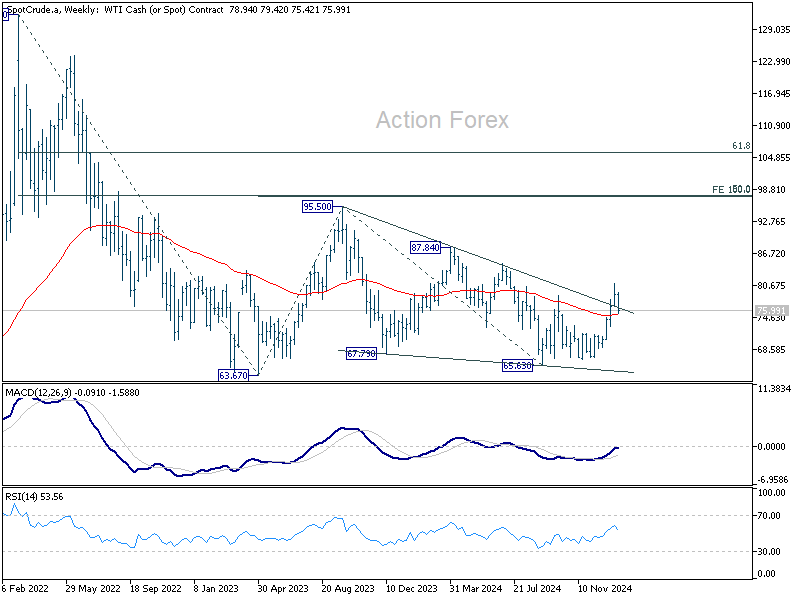

WTI crude oil extended the retreat form 81.01 short term top last week. While deeper fall cannot ruled out, near term outlook will stay bullish as long as 55 D EMA (now at 73.34) holds. Rise from 65.63 is expected to resume through 81.01 at a later stage.

Current preferred interpretation is that consolidation pattern from 95.50 (2023 high) has completed with three waves down to 65.63 (2024 low). Firm break of 87.84 resistance would solidify this bullish case, and at least bring a retest of 95.50 key resistance.

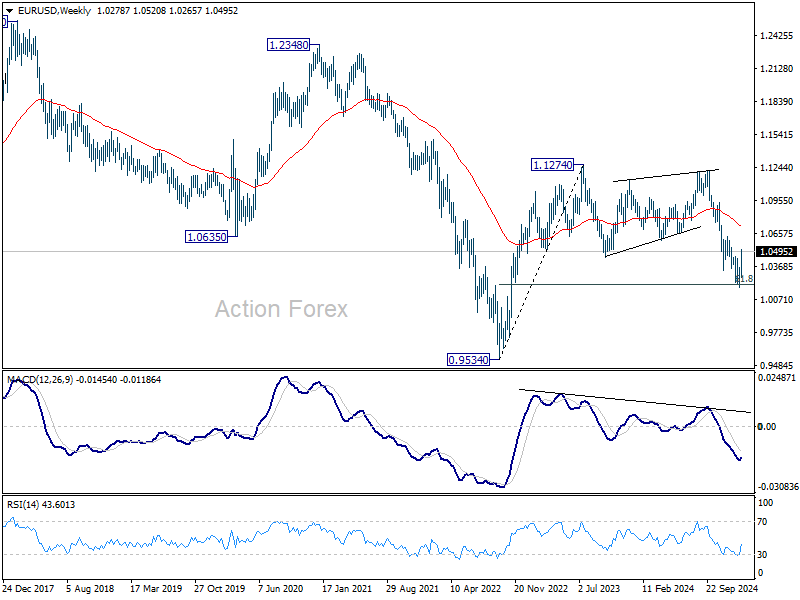

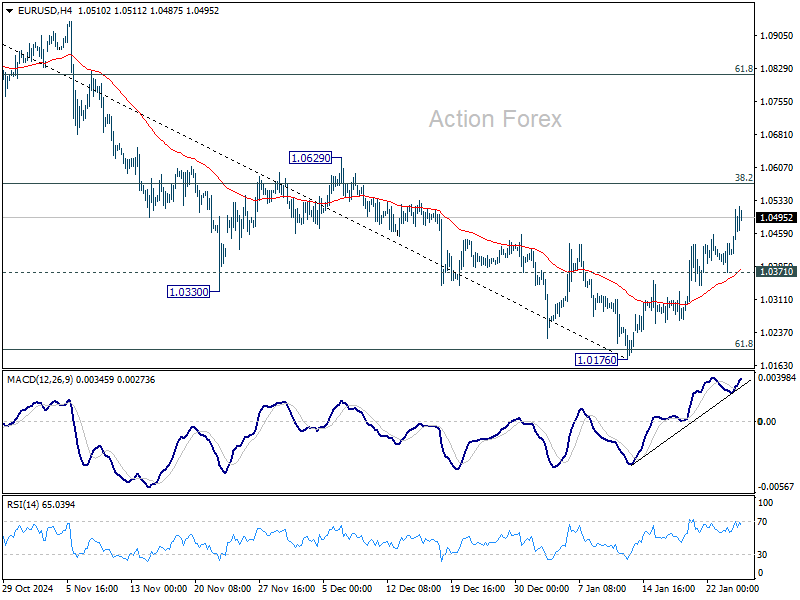

EUR/USD Weekly Outlook

EUR/USD’s rebound from 1.0176 short term bottom accelerated higher last week and there is no sign of topping yet. Initial bias stays on the upside this week for 38.2% retracement of 1.1213 to 1.0176 at 1.0572 sustained break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817. On the downside break of 1.0371 minor support will retain near term bearishness and bring retest of 1.0176 low.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0973). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, eventual downside breakout would be mildly in favor.