Euro posted notable gains today as lifted by encouraging Eurozone PMI data that suggests the region is beginning the year on firmer footing. Private sector activity showed cautious growth, with reduced drag from manufacturing and moderate expansion in services. Most surprisingly, Germany, which struggled throughout 2024, returned to expansion. Sterling also gained on better PMI readings even though stagnation risks persist, particularly due to accelerated job cuts in the UK.

Dollar extended its decline as risk-on sentiment dominated markets, despite US equity indices taking a breather after strong rallies earlier this week. The greenback is currently the weakest performer for the day, followed by Yen, which gave back its brief gains following BoJ’s widely anticipated rate hike. The Swiss Franc also underperformed, completing a trio of safe-haven currencies that lagged behind in today’s risk-driven market environment.

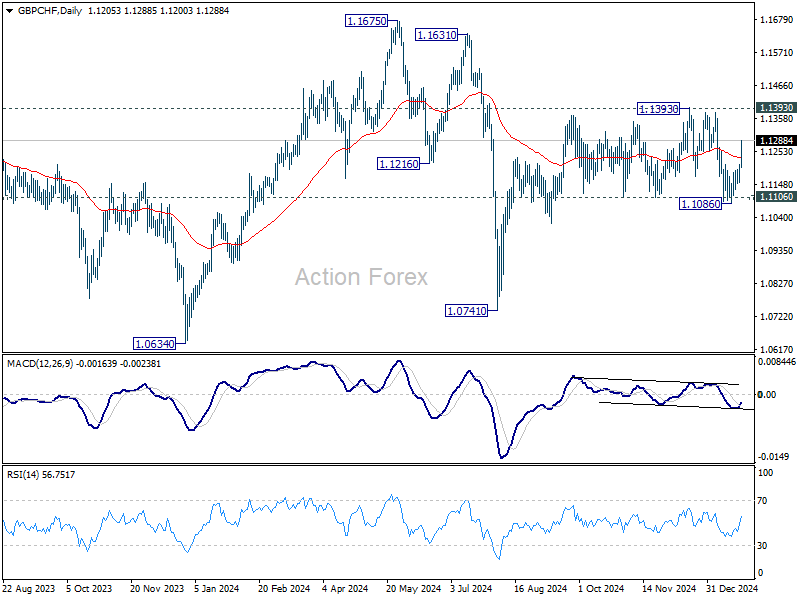

Technically, Swiss Franc’s weakness warrants closer attention. The strong rally in GBP/CHF today suggest that fall from 1.1393 has completed at 1.1086 after defending 1.1106 support. The development keeps the rally from 1.0741 alive. Retest of 1.1393 would be seen next, and firm break there will extend the rise towards 1.1675 high.

In Europe, at the time of writing, FTSE is down -0.75%. DAX is down -0.20%. CAC is up 0.36%. UK 10-year yield is down -0.001 at 4.639. Germany 10-year yield up 0.028 at 2.579. Earlier in Asia, Nikkei fell -0.07%. Hong Kong HSI rose 1.86%. China Shanghai SSE rose 0.70%. Singapore Strait Times fell -0.06%. Japan 10-year JGB yield rose 0.0255 to 1.235.

US PMI composite falls to 9-mth low, optimism holds despite slowing growth and rising costs

US PMI data for January painted a mixed picture. PMI Manufacturing rose from 49.4 to 50.1, reaching a seven-month high and signaling a return to slight expansion. However, PMI Services dropped sharply from 56.8 to 52.8, a nine-month low, dragging PMI Composite down from 55.4 to 52.4, also a nine-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlighted that US businesses are starting 2025 in an “upbeat mood,” with optimism about the new administration driving stronger economic growth. Despite the slowdown in output growth, “sustained confidence” among businesses suggests this deceleration may be temporary. Encouragingly, hiring has surged, with job creation reaching its fastest pace in two and a half years, signaling resilience in the labor market.

However, inflationary pressures are resurfacing, posing risks to the economic outlook. Companies have reported “supplier-driven price hikes” and “wage growth amid poor staff availability.” Inflation in input costs and selling prices has been “broad-based across goods and services,” which, if sustained, could fuel concerns about hawkish policy approach from the Fed.

UK PMI composite edges higher to 50.9, but stagflation risks cloud economic outlook

UK PMI Composite rose slightly from 50.4 to 50.9 in January, indicating marginal growth. Manufacturing PMI improved from 47.0 to 48.2, while services PMI ticked up from 51.1 to 51.2. Despite these increases, the overall outlook remains gloomy, with underlying concerns about economic weakness and inflationary pressures persisting.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, warned that the data “add to the gloom” surrounding the UK economy.

Companies are cutting jobs at the fastest rate since the global financial crisis in 2009, reflecting falling sales and bleak business prospects. Business optimism remains at its lowest levels in two years, accompanied by subdued activity across sectors.

Inflationary pressures have also “reignited,” creating what Williamson described as a “stagflationary environment” and a “policy quandary” for BoE.

Eurozone PMI composite hits 50.2 as Germany returns to growth

Eurozone PMI data for January showed cautious improvement, with PMI Composite rising from 49.6 to 50.2, a five-month high, signaling a return to marginal growth. Manufacturing PMI increased to 46.1, its highest in eight months, while services PMI slipped slightly to 51.4 but remained in expansion.

Germany led the improvement, with its PMI Composite climbing from 48.0 to 50.1, marking a seven-month high and a return to expansionary territory. Meanwhile, France lagged behind, with its PMI Composite increasing to 48.3 but remaining below the 50 threshold, indicating continued contraction.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the data as “mildly encouraging.” He noted that the private sector had entered a phase of cautious growth, with reduced drag from manufacturing and moderate expansion in services. Germany’s strong rebound played a key role in offsetting the continued weakness in France.

Inflationary pressures, however, remain a concern ahead of next week’s ECB meeting. Input prices in manufacturing rose for the first time in four months, driven by a weaker euro and Germany’s increased CO2 tax. In the services sector, cost inflation persisted, largely due to higher wages. Selling prices in services also remained elevated.

Due to persistent inflation risks and the fragile state of the economy, ECB is likely stick to its gradual pace of cutting interest rates.

BoJ delivers expected rate hike, upgrades core inflation forecasts

BoJ raised its uncollateralized overnight call rate by 25bps to 0.50% as widely expected, marking the highest level since 2008. The decision, made by an 8-1 vote, saw dissent from board member Nakamura Toyoaki, who advocated for a delay until March.

In the new economic projections, core CPI forecasts were significantly revised upward from 1.9% to 2.4% for fiscal 2025, and slightly from 1.9% to 2.0% for fiscal 2026. Core-core CPI (excluding energy and fresh food) forecast was also raised from 1.9% to 2.1% for fiscal 2025, remaining unchanged at 2.1% for fiscal 2026. Real GDP growth projections were left steady at 1.1% for fiscal 2025 and 1.0% for fiscal 2026.

At the post-meeting press conference, Governor Kazuo Ueda downplayed the sharp inflation forecast revisions, stating, “The rise in underlying inflation is moderate. I don’t think we are seriously behind the curve in dealing with inflation.”

He reiterated the importance of a gradual approach to policy adjustments, and there no “preset idea” on the timing and pace of rate hikes. He also highlighted the estimated neutral range of 1%-2.5%, emphasizing that the current rate of 0.5% still has “some distance” to reach neutral.

Also released, CPI core (ex-food) jumped from 2.7% yoy to 3.0% yoy in December, marking the highest rate in 16 months. CPI core-core (ex-food & energy) was unchanged at 2.4% yoy. Headline CPI rose from 2.9% yoy to 3.6% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0379; (P) 1.0409; (R1) 1.0445; More…

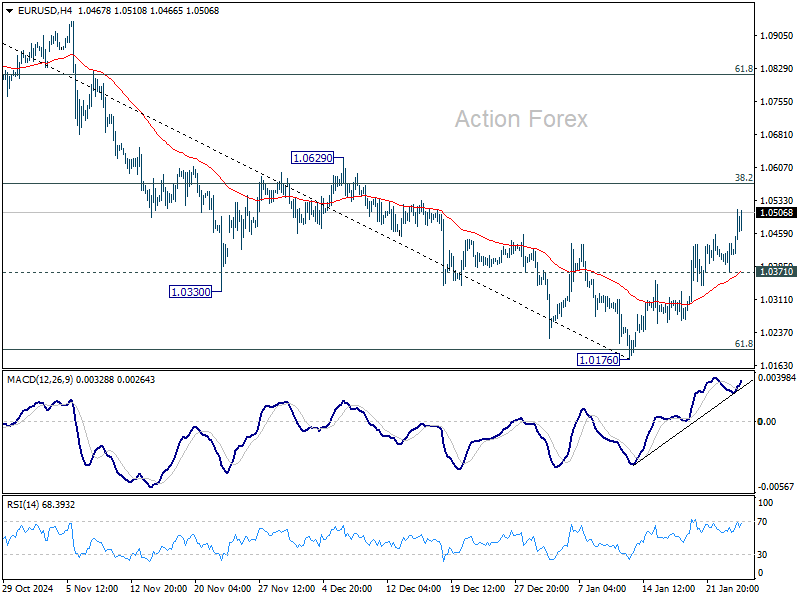

Intraday bias in EUR/USD remains on the upside as rebound from 1.1076 is in progress. Strong resistance might be seen from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. Break of 1.0371 minor support will bring retest of 1.0176 low. However, sustained break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.