While Yen remains the worst performer of the week so far, it has stabilized as the markets await the highly anticipated BoJ rate hike in the upcoming Asian session. Expectations for this rate move were well set by comments from BoJ Governor Kazuo Ueda last week. Risks from US political developments—specifically tariff policies under President Donald Trump—have now been set aside too, clearing the way for BoJ to proceed with its monetary normalization. Policy rate should be raised by 25bps to 0.50%.

The question now centers on how BoJ will portray Japan’s economic outlook and its policy path for the year. With signs of resurgent inflationary pressures, it’s unlikely that Ueda will strike a dovish tone. In fact, Japan’s upcoming CPI datad ue tomorrow too—expected to show core inflation rising for a second month to 3% in December—will support that view.

Ueda’s comments in the post meeting press conference could be cautiously optimic. On the one hand, he would reiterate international uncertainties, and refrain from committing to a specific timeline for policy normalization. But the view towards domestic wage development could be upbeat. Inflation forecasts could also be raised in the new quarterly economic outlook report. Both would be seen as hawkish, albeit mildly. Currently, markets are seeing the chances of another hike in the middle of the year, and probably one more by the year-end to bring interest rate to a more neutral setting at 1.00%.

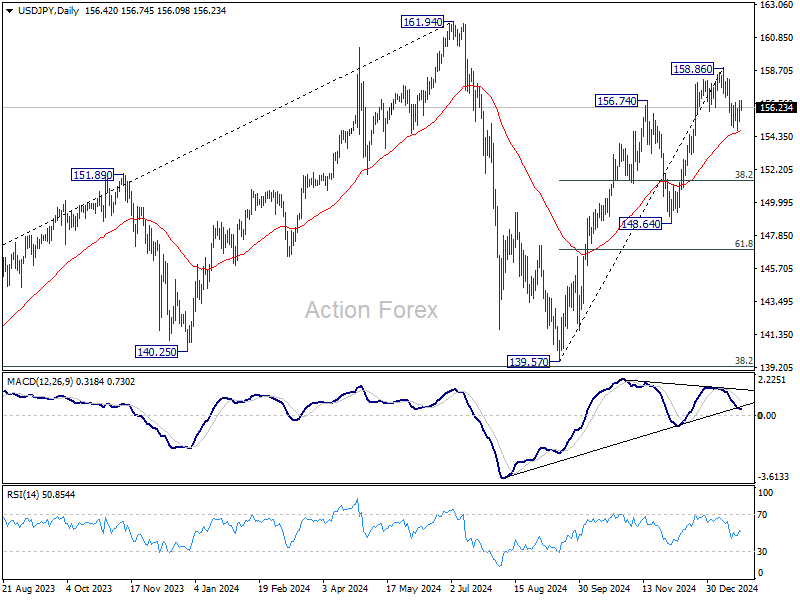

USD/JPY would be logically a pair to pay attention to. Price actions from 158.86 are seen as developing in to a corrective pattern for sure. While initial support was seen above 55 D EMA (now at 154.67) to slow the pull back, a hawkish BoJ hike tomorrow could push USD/JPY lower towards 38.2% retracement of 139.57 to 158.86 at 151.49.

Conversely, a robust rebound—even if BoJ sounds hawkish—might suggest that the correction from 158.86 is already done, and the rally from 139.57 could be ready to resume.

Overall for the week so far, the rankings in the performance ladder didn’t chance much as trading has been rather subdued after volatility on Monday. Kiwi is currently the strongest, followed by Euro and then Aussie. Yen is the worst, followed by Dollar and then Loonie. Sterling and Swiss Franc are stuck in the middle.

Canada’s retail sales stagnate in Nov as core sales down -1% mom

Canada’s retail sales were flat in November, falling short of the expected 0.2% mom increase. The data revealed mixed performance across sectors, with declines in six out of nine subsectors.

Sales at food and beverage retailers dropped by -1.6% mom, driving much of the weakness in the report. However, gains in motor vehicle and parts dealers (+2.0% mom) and gasoline stations and fuel vendors (+0.7% mom) helped offset the broader declines, preventing an outright contraction in overall retail activity.

Core retail sales, which exclude the more volatile categories of motor vehicles and gasoline, declined by a notable -1.0% mom.

US initial jobless claims rises to 223k, above exp 220k

US initial jobless claims rose 6k to 223k in the week ending January 18, above expectation of 220k. Four-week moving of initial claims rose 750 to 213.5k.

Continuing claims rose 46k to 1899 in the week ending January 11, highest since November 13, 2021. Four-week moving average of continuing claims rose 500 to 1866k.

Japan posts first trade surplus in six months

Japan recorded a trade surplus of JPY 130.9B in December, the first surplus in six months, driven by a 2.8% yoy rise in exports to JPY 9.91T. Imports also jumped, rising 1.8% yoy to JPY 9.8T.

However, exports to the two largest trading partners saw declines, with shipments to China falling by -3.0% yoy and to the US by 2.1% yoy.

On a month-on-month seasonally adjusted basis, exports rose 6.3% mom to JPY 9.44T. Imports increased 2.2% mom to JPY 9.47T, resulting in a seasonally adjusted trade deficit of JPY 33B.

For the entirety of 2024, Japan’s trade deficit narrowed significantly, shrinking by 44% from the previous year to JPY -5.33T. Exports reached a record high of JPY 107.09T, up 6.2%, bolstered by strong demand for vehicles and semiconductor-related products. Imports also rose by 1.8% to JPY 112.42T.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0368; (P) 1.0401; (R1) 1.0461; More…

Intraday bias in EUR/USD remains neutral for the moment. On the upside, firm break of 1.0435 resistance will extend the rebound from 1.0176 to 38.2% retracement of 1.1213 to 1.0176 at 1.0572. Rejection by 1.0435 will keep the correction from 1.0176 relatively short. Firm break of 1.0176 will resume whole fall from 1.1213.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.