Sterling continues to trade under pressure following a week of disappointing UK economic data, with weak December retail sales completing a trio of negative reports that also included lower-than-expected GDP growth and CPI readings. The data has reinforced market expectations that BoE would ease monetary policy in 2025, as the economy struggles under the new measures of the government’s Autumn Budget.

Current interest rate futures are pricing in just two 25bps rate cuts for the year, but a recent Reuters poll (January 10–15) suggests greater dovish sentiment among economists. Of the 63 surveyed, 38 anticipate four rate cuts in 2025, which would bring the Bank Rate down to 3.75%. Immediate action is expected at the February 6 policy meeting, with all 65 participants in the survey forecasting a 25 bps cut.

However, elevated core inflation, which remains stubbornly high at 3.2%, limits BoE’s room to signal further easing ahead. This hesitation risks limiting both business confidence and broader economic morale, even on a psychological level.

In Asia, the market reaction to China’s 2024 GDP report has been notably subdued. The data showed that China’s economy met its official growth target of 5%, despite skepticism from analysts over the credibility of the figure. Yet, stocks in both China and Hong Kong posted only modest gains, reflecting tepid investor sentiment. Australian and New Zealand Dollars remained range-bound, with the latter under particular strain following weak manufacturing data.

In the currency markets, Pound ranks as the week’s worst performer for the week so far, trailed by Dollar and Canadian Dollar. The greenback is consolidation recent gains ahead of the inauguration of US President-elect Donald Trump on Monday. In contrast, Yen is the strongest currency, buoyed by increasing speculation of rate hike from BoJ next week. Australian and New Zealand Dollars follow, recovering slightly from earlier losses in the month, while Euro and Swiss Franc are stuck in middle positions.

Technically, NZD/JPY is still struggling to break through 86.71 support despite trying to break through twice. Yet, outlook is staying bearish with clear rejection by 55 D EMA. Fall from 92.45 could be the second leg of the sideway pattern from 83.02, based on current momentum. Firm break of 86.71 will bring deeper decline to 83.02, where strong support is expected to contain downside and bring near term reversal.

UK retail sales fall -0.3% mom in Dec, down -0.8% qoq in Q4

UK retail sales volumes declined by -0.3% mom in December, significantly missing expectations for 0.4% mom increase. The drop was primarily driven by reduced supermarket sales, partially offset by a rebound in non-food stores such as clothing retailers, which saw recovery after recent declines.

On a quarterly basis, sales volumes in Q4 fell -0.8% qoq compared with Q3, highlighting a slowdown in consumer activity. However, year-on-year, Q4 sales volumes rose 1.9% compared to the same period in 2023.

China’s Q4 GDP growth surpasses expectations, full-year growth hits 5% target

China’s economy ended 2024 on a strong note, with GDP expanding by 5.4% yoy in Q4, beating market expectations of 5.0%. This marked a significant acceleration from 4.6% in Q3, 4.7% in Q2, and 5.3% in Q1. The robust Q4 performance pushed full-year GDP growth to 5.0%, aligning with the government’s target of “around 5%.”

December’s economic indicators also showed positive momentum. Industrial production surged 6.2% yoy, exceeding the forecast of 5.4%. Retail sales grew by 3.7% yoy, marginally beating expectations of 3.5%. However, fixed asset investment lagged, rising only 3.2% year-to-date, just below the 3.3% forecast.

Despite the upbeat data, concerns remain. Statistics Bureau spokesperson Fu Linghui acknowledged lingering weakness in consumer spending and cautioned that in 2025, the “unfavorable impact of external factors may deepen.”

BNZ PMI at 45.9: NZ manufacturing completes 2024 fully in contraction

New Zealand’s BNZ Performance of Manufacturing Index rose marginally in December, increasing from 45.2 to 45.9. While this marks a slight improvement, the sector remains in a prolonged contraction, far below the long-term average of 52.5 since the survey’s inception. December also marked the 22nd consecutive month of contraction, a record-breaking trend for the PMI.

Catherine Beard, Director of Advocacy at BusinessNZ, noted that 2024 was unprecedented, as it was the first year in the survey’s history with all 12 months in contraction. By comparison, the next closest period was 2008 during the Global Financial Crisis, which saw nine months of contraction.

Breaking down the December data, production dropped further, slipping from 42.3 to 41.9. Employment showed modest improvement, rising from 46.9 to 47.6, while new orders also edged up from 44.5 to 46.5. However, finished stocks fell significantly, declining from 49.2 to 45.9, and deliveries dipped slightly below the neutral 50 mark, moving from 50.0 to 49.8.

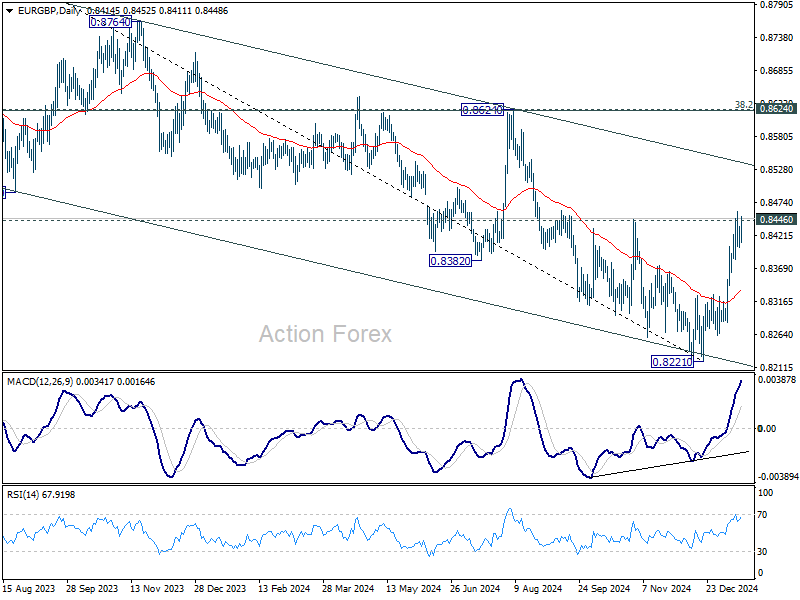

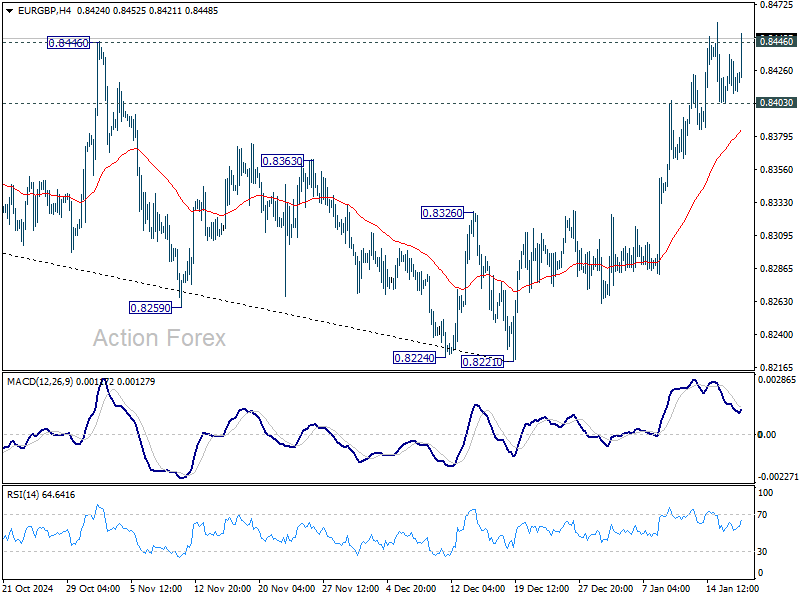

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8404; (P) 0.8421; (R1) 0.8435; More…

Intraday bias in EUR/GBP remains neutral first with focus on 0.8446 resistance. Decisive break there will resume the rally from 0.8221 to 0.8624 cluster resistance zone. On the downside, however, break of 0.8403 minor support will indicate rejection by 0.8446, and turn bias back to the downside for 55 D EMA (now at 0.8332).

In the bigger picture, considering bullish convergence condition in D MACD, decisive break of 0.8446 resistance and 55 W EMA (now at 0.8446) should confirm medium term bottoming at 0.8221, just ahead of 0.8201 key support (2022 low). Further rally should be seen towards 0.8624 key resistance, even as a correction to the down trend from 0.9267 (2022 high). Overall, however, medium term outlook will be neutral at best until decisive break of 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621). Risk will stay on the downside even in case of strong rebound.