Australian Dollar staged an impressive rebound today, driven by robust employment data that surprised markets and cast doubt on the likelihood of a February rate cut by RBA. The stronger-than-expected labor market performance challenges the dovish sentiment established earlier in the week when RBA softened its inflation vigilance stance.

In the aftermath of RBA meeting, market participants had sharply increased their bets on a February rate cut, with swaps pricing in a 75% probability. However, today’s data shifted the narrative, bringing those odds down to around 50%.

The report highlighted the ongoing tightness in the labor market, suggesting that immediate easing may not be necessary. Still, the ultimate decision hinges on Q4 CPI data, set for release in late January. Without clear progress on disinflation, the RBA may opt to maintain its cautious approach, delaying any action until May until further confidence on inflation is gained.

In currency markets, Aussie leads gains today, followed by Kiwi and Euro. On the other hand, Dollar is the weakest performer, with Yen and Swiss Franc also under pressure. Sterling and the Canadian Dollar are mixed in the middle. Traders are now shifting their attention to SNB and ECB rate decisions scheduled later in the day.

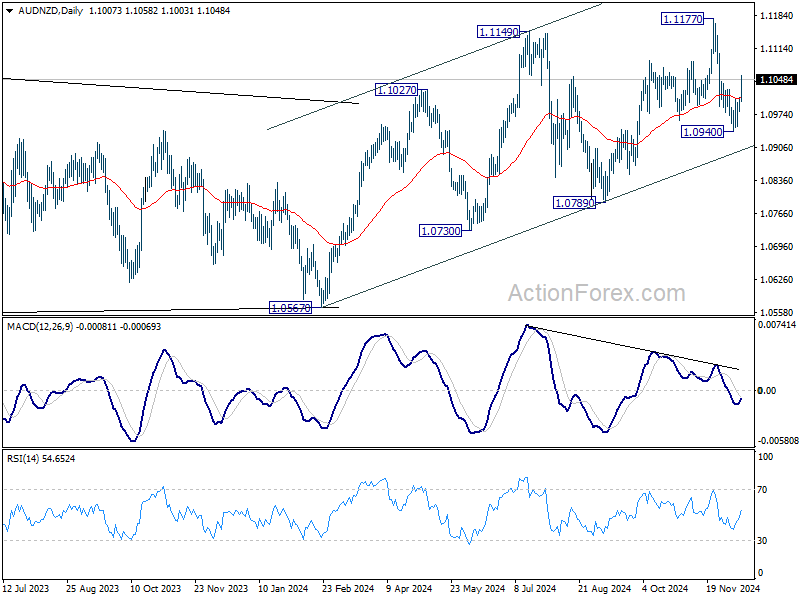

Technically, AUD/NZD’s strong rebound today suggests that pull back from 1.1177 might have completed at 1.0940 already. The development also keeps the up trend from 1.0567 alive. Nevertheless, while further upside is likely in the near term, AUD/NZD’s upside would likely be capped by 1.1177 resistance to extend sideway consolidations first.

In Asia, Nikkei rose 1.21%. Hong Kong HSI is up 1.63%. China Shanghai SSE is up 0.85%. Singapore Strait Times is up 0.35%. Japan 10-year JGB yield fell -0.0228 to 1.049. Overnight, DOW fell -0.22%. S&P 500 rose 0.87%. NASDAQ rose 1.77%. 10-year yield rose 0.50 to 4.271.

Australia’s employment data beats expectations, unemployment drops below to 3.9%

Australia’s labor market showed surprising resilience in November as employment grew by 35.6k, surpassing expectations of a 29.6k increase. The standout figure was the 52.6k gain in full-time jobs, offsetting a decline of -17k in part-time positions.

Unemployment rate fell significantly, dropping from 4.1% to 3.9%, well below the anticipated 4.2%. However, a slight dip in the participation rate, from a record high of 67.1% to 67.0%, tempered the optimism.

Employment-to-population ratio nudged up to 64.4%, matching levels from a year ago and maintaining its position 2.2% above pre-pandemic levels. Monthly hours worked showed no growth, indicating stability in workforce activity despite the overall gains in employment.

David Taylor, Head of Labour Statistics at the ABS, noted that an unusually high number of unemployed individuals transitioned into employment during November. This dynamic contributed to both the rise in job creation and the sharp fall in unemployment. Taylor also highlighted the role of population growth, which has bolstered labor supply and helped maintain the balance between employment growth and demographic expansion.

SNB and ECB in spotlight as markets gauge depth of cuts and dovish signals

Today’s focus is firmly on the monetary policy decisions from SNB and ECB, with markets eager to gauge not just the magnitude of the expected rate cuts but also the tone of their forward guidance. Both central banks are expected to ease, but the precise depth of the cuts and their outlook on future policy will drive market reactions.

SNB is widely anticipated to cut its policy rate by 25bps 1.00% to 0.75%. However, speculation of a more aggressive 50bps cut persists, with financial market pricing increasingly leaning toward this scenario.

SNB has considerable room to maneuver, given Switzerland’s inflation rate of just 0.7%—the lowest among major economies. However, with rates already close to zero, SNB must balance immediate economic support with preserving policy ammunition for the future.

After all, today’s move will not mark the end of the easing cycle of SNB, as economists project further reductions through 2025, driving the policy rate to 0.25% or even zero by the end of next year.

For ECB, the debate has also revolved around the scale of its next move. Recent speculation about a 50bps cut has largely been dismissed following comments from ECB officials, leaving a 25bps reduction in the Deposit Rate to 3.00% as the more probable outcome.

However, market participants are paying close attention to the tone of ECB’s statement and press conference. With inflation expected to settle earlier at target by mid-2025 amid weak economic activity, ECB would signal explicitly the need for sustained easing into next year.

Investors currently expect a cut at every meeting until mid-2025, with the Deposit Rate potentially reaching 1.75% by year-end. However, such an aggressive pace could bring rates below the neutral level.

In terms of market impact, EUR/CHF is the currency pair to watch. Outlook is clearly bearish with EUR/CHF staying well below falling 55 D EMA. However, in case of another dive, 0.9209 key support might continue to provide support for a bounce a second time, barring any drastic surprises. Meanwhile, there would be no clear confirmation of bullish reversal until decisive break of 55 D EMA (now at 0.9362).

Elsewhere

In addition to ECB and SNB, Canada building permits, US PPI and jobless claims will also be featured.

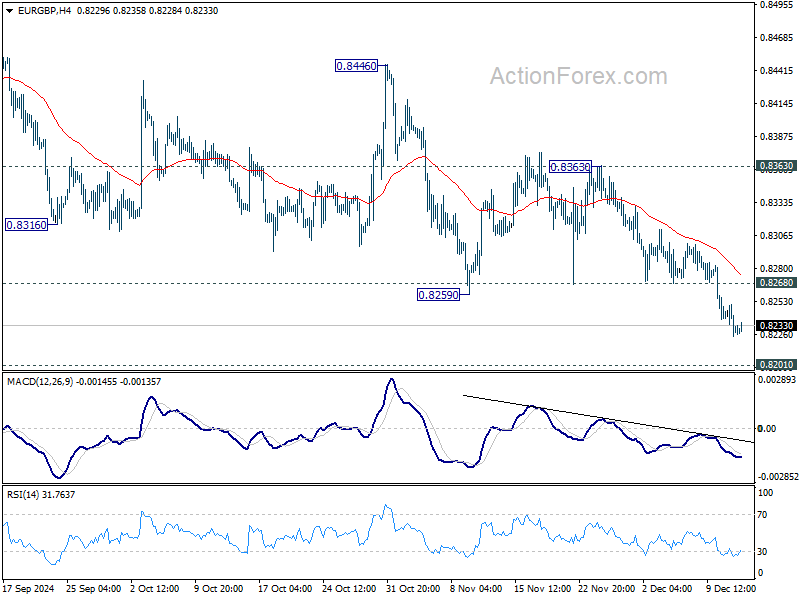

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8221; (P) 0.8236; (R1) 0.8248; More…

EUR/GBP’s down trend is still in progress and intraday bias stays on the downside for 0.8201 key support. Strong support could be seen there to bring rebound. On the upside, above 0.8268 minor resistance will turn intraday bias neutral first. Further break of 0.8363 resistance will be the first signal of bullish trend reversal. However, sustained break of 0.8201 will carry larger bearish implications.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.