The Euro rebounded broadly today, buoyed by reassurances from a number of ECB officials that the central bank remains committed to a gradual approach to policy easing. Yesterday’s 25bps rate cut appears to have had solid consensus backing, with no indications that a more aggressive 50bps cut was even seriously debated. Despite recent economic softness in the Eurozone, ECB is maintaining a measured strategy without overreacting to weak activity data. Though the Euro remains lower against the Dollar for the week, its recovery against Sterling and Swiss Franc adds momentum to its performance.

Sterling, however, faced a challenging session after UK GDP data revealed a contraction for October, undermining confidence in the government’s recent pledge to boost economic growth. While this setback adds pressure to an already fragile outlook, it is unlikely to shift BoE’s stance on policy easing significantly. A BoE survey released today highlighted that long-term inflation expectations have risen to 3.4% in November, the highest level since May 2022, up from 3.2% in August. Additionally, the survey revealed that 33% of respondents expect interest rates to rise in the next 12 months, compared to 29% in the previous quarter. These findings suggest BoE will maintain its gradual approach to rate adjustments.

Overall for the week so far, Dollar is currently the strongest, followed by Aussie, and then Loonie. Yen is the worst, followed by Swiss Franc, and then Kiwi. Euro and Sterling are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 0.08%. CAC is up 0.22%. UK 10-year yield is up 0.0185 at 4.383. Germany 10-year yield is up 0.371 at 2.248. Earlier in Asia, Nikkei fell -0.95%. Hong Kong HSI fell -2.09%. China Shanghai SSE fell -2.01%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield fell -00103 to 1.041.

ECB officials signal more rate cuts Ahead, gradual path to neutral

A day after ECB reduced its deposit rate by 25 basis points to 3.00%, key ECB officials provided insights into the central bank’s outlook, reinforcing expectations for further easing in 2025. Comments from various members of the Governing Council suggest a shared commitment to a cautious but consistent approach to policy normalization.

French ECB Governing Council member François Villeroy de Galhau explicitly stated, “There will be more rate cuts next year, more rate cuts plural,” emphasizing alignment with market forecasts. The swap market currently prices around 120 basis points of rate reductions by the end of 2025.

Similarly, Spanish member José Luis Escrivá noted the prevailing consensus for “moves of 25 basis points downwards,” allowing for regular assessment of disinflationary progress.

Irish ECB member Gabriel Makhlouf highlighted the clarity in the rate trajectory while maintaining a data-driven approach: “The exact pace and number of further reductions depend on inflation outturns continuing to move in line with our projections.”

Portuguese member Mário Centeno added that rates could approach the 2% level within a few quarters, barring new economic shocks.

Comments from Luxembourg’s Gaston Reinesch pointed to the possibility of reaching a 2.5% deposit rate by early spring, implying consecutive 25bps cuts in January and March.

Latvian member Martins Kazaks kept the door open for larger adjustments if warranted, while Austria’s Robert Holzmann reiterated alignment with forecasts, noting that rates would ultimately settle closer to neutral.

Eurozone industrial production stagnates in Oct

Eurozone industrial production stagnated in October, recording 0.0% mom growth, in line with expectations. The data reflects mixed performance across sectors. While output for capital goods rose by 1.7%, intermediate goods production remained unchanged. On the downside, energy production dropped sharply by -1.9%, while durable and non-durable consumer goods contracted by -1.8% and -2.3%, respectively,.

Across the broader EU, industrial production showed a modest increase of 0.3% mom, driven by strong gains in select countries. Ireland led the pack with a 5.7% increase, followed by Denmark at 5.4% and Poland at 3.5%. However, significant declines were observed in Lithuania (-7.5%), Belgium (-6.2%), and Croatia (-3.9%).

UK economy contracts -0.1% mom in Oct, dragged down by weak production

UK GDP fell by -0.1% mom in October, disappointing expectations for 0.1% mom growth. The decline was primarily driven by a -0.6% mom contraction in production output, with no growth observed in services and a -0.4% mom decline in construction output.

On a rolling three-month basis, GDP showed a marginal increase of 0.1% in the period ending October, compared to the prior three-month period. This modest growth was supported by a 0.1% expansion in services and a 0.4% rise in construction output. However, production output contracted by -0.3%, weighing on overall performance.

Japan’s Tankan Survey: Manufacturing Confidence Improves to 14

Confidence among Japan’s major manufacturers showed a modest recovery in Q4, breaking a two-quarter decline. The Tankan large manufacturing index rose to 14 from 13, slightly exceeding market expectations. However, the outlook dipped marginally from 14 to 13, though still better than the anticipated 11.

In contrast, the non-manufacturing sector, which includes services, saw its index decline to 33 from 34, marking the first deterioration in two quarters. The outlook for non-manufacturers held steady at 28.

On a bright note, large Japanese companies across sectors plan to boost capital expenditure by 11.3% in the fiscal year ending March 2025. This is a notable increase from the 10.6% projection in the September survey and surpasses market forecasts of 9.6%.

NZ BNZ PMI falls to 45.5, 21st month of contraction

New Zealand’s BNZ Performance of Manufacturing Index dipped from 45.7 to 45.5 in November, marking its lowest reading since July 2024 and extending the contraction streak to 21 consecutive months. Despite some improvement in select components, the sector remains under significant strain, highlighting the challenges of achieving a meaningful turnaround.

Production weakened further, dropping from 44.0 to 42.5, signaling continued struggles in output. New orders also plunged from 48.5 to 44.8, underlining the persistent lack of demand. In contrast, employment improved modestly from 46.0 to 46.9, and finished stocks edged higher from 47.8 to 49.3. Deliveries saw the most notable recovery, rising from 44.9 to 49.9, yet still narrowly missed returning to expansion territory.

The sentiment among respondents remains predominantly negative, with 56% of comments in November reflecting pessimism, slightly up from 53.5% in October. Recurring concerns revolve around weak order volumes and the enduring pressures of high living costs. However, this negativity has moderated from its peak of 71.1% in mid-2024, suggesting some stabilization.

Doug Steel, Senior Economist at BNZ, noted that while manufacturers are beginning to show improved confidence about the future, “the main message of a manufacturing sector still under significant pressure remains. There is scant evidence of a general turnaround in activity to date.”

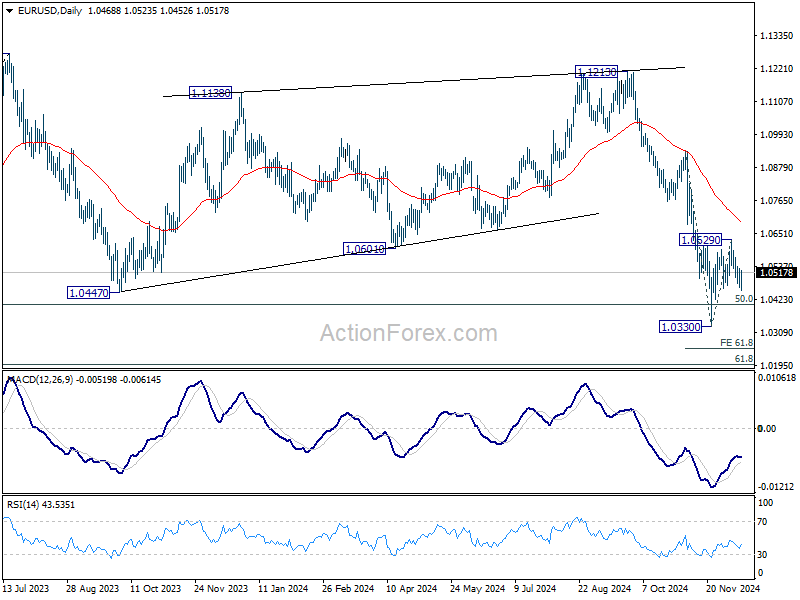

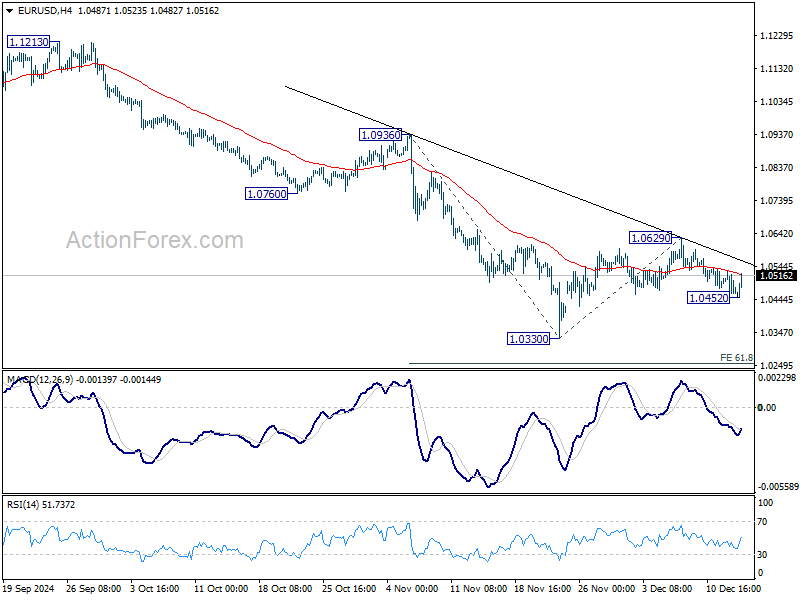

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0443; (P) 1.0487; (R1) 1.0510; More…

EUR/USD recovered notably after dipping to 1.0452 briefly and intraday bias is turned neutral again. Outlook is unchanged that corrective rise from 1.0330 should be completed at 1.0629, and further decline is expected. Below 1.0452 will bring retest of 1.0330, and then resume the fall form 1.1213 to 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.