Commodity currencies found significant support today after China pledged to intensify its economic stimulus efforts, aiming to secure next year’s growth targets. Australian Dollar led the charge, followed by New Zealand Dollar and Canadian Dollar, as risk-sensitive assets reacted positively to the news. Meanwhile, Hong Kong’s HSI surged, reflecting optimism in the region, though gains were just modest in Chinese Yuan.

China’s announcement comes just ahead of the Central Economic Work Conference, an annual meeting that sets the nation’s key policy priorities for the year ahead. State media highlighted President Xi Jinping’s directive for “full preparation” to meet economic targets for 2025, emphasizing the need to tackle “uncertainties and challenges.” Xi also promised “proactive” fiscal measures and “moderately loose” monetary policy, complemented by enhanced counter-cyclical adjustments. However, markets were left waiting for concrete details, which are unlikely to surface before the parliamentary session in March.

The market reaction was pronounced, with risk-sensitive currencies outperforming while traditional safe havens like the Japanese Yen, Swiss Franc, and Euro lagged. Yen, in particular, is the day’s weakest performer so far, reflecting a shift away from defensive positioning. Dollar and British Pound are mixed in the middle.

On the technical front, Hong Kong HSI’s strong rebound today now supports that case that corrective fall from 23241.74 has completed with three waves down to 19054.40. That came after drawing support form 50% retracement of 14794.16 to 23241.74 at 19054.40, as well as medium term rising channel. Next target is 21355.44 resistance. Firm break there will argue that the up trend form 14794.16 is ready to resume. If realized, the bullish development in HSI could help floor AUD/USD’s decline above 0.6169 key support (2022 low).

In Europe at the time of writing, FTSE is up 0.56%. DAX is down -0.08%. CAC is up 0.52%. UK 10-year yield is down -0.021 at 4.259. Germany 10-year yield is down -0.015 at 2.099. Earlier in Asia, Nikkei rose 0.18%. Hong Kong HSI rose 2.76%. China Shanghai SSE fell -0.05%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield fell -0.0111 to 1.042.

Eurozone Sentix plunges to -17.5 amid economic and political turmoil

Investor sentiment in the Eurozone deteriorated sharply in December, with the Sentix Investor Confidence Index dropping to -17.5 from -12.8, significantly below expectations of -13.1. This marks the weakest reading since November 2023. Current Situation Index fell to -28.5, the lowest since November 2022, while Expectations Index slipped to -5.8 from -3.8. .

Germany remains a key drag, with its Current Situation Index sinking to -50.8, the lowest since June 2020, reflecting the persistence of recessionary pressures. The announcement of new Bundestag elections failed to inspire optimism, while France’s ongoing government crisis has added another layer of economic uncertainty. Sentix highlighted that “the two largest countries in the Eurozone are dragging down the EU economy.”

ECB faces increasing pressure as investors expect stronger monetary support for the faltering economy. However, inflation concerns persist, with Sentix’s inflation barometer holding at -12 points, signaling continued unease. This dual challenge highlights a conflict for ECB as it balances the need for economic stimulus with inflationary risks.

China’s CPI falls to 0.2% yoy in Nov, PPI down -2.5% yoy, deflation pressures persist

China’s CPI decelerated from 0.3% yoy to 0.2% yoy in November, below market expectations of 0.5% yoy, and marking its lowest level in five months. Persistent deflationary pressures highlight the urgency for stronger fiscal measures to reinvigorate the economy.

Food prices was the primary driver of inflation, surging by 1% yoy, with notable increases in vegetable and pork prices at 10% yoy and 13.7% yoy, respectively. However, core inflation, which excludes volatile food and energy prices, edged up only marginally to 0.3% yoy from 0.2% yoy.

Meanwhile, PPI improved, registering a -2.5% yoy decline in November compared to -2.9% in October, beating expectations of -2.9% yoy. While this marked the 26th consecutive month of negative readings, the moderation was attributed to a combination of existing and incremental policy measures alongside a recovery in domestic demand for industrial goods.

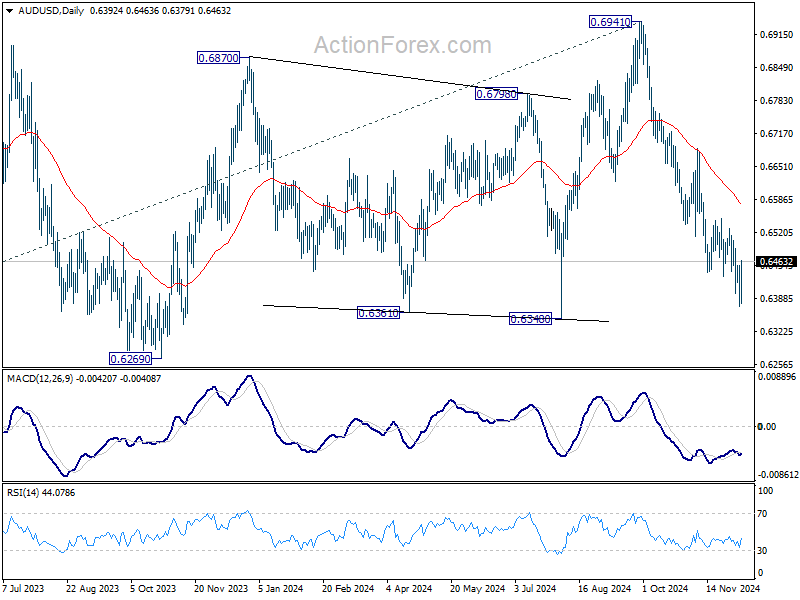

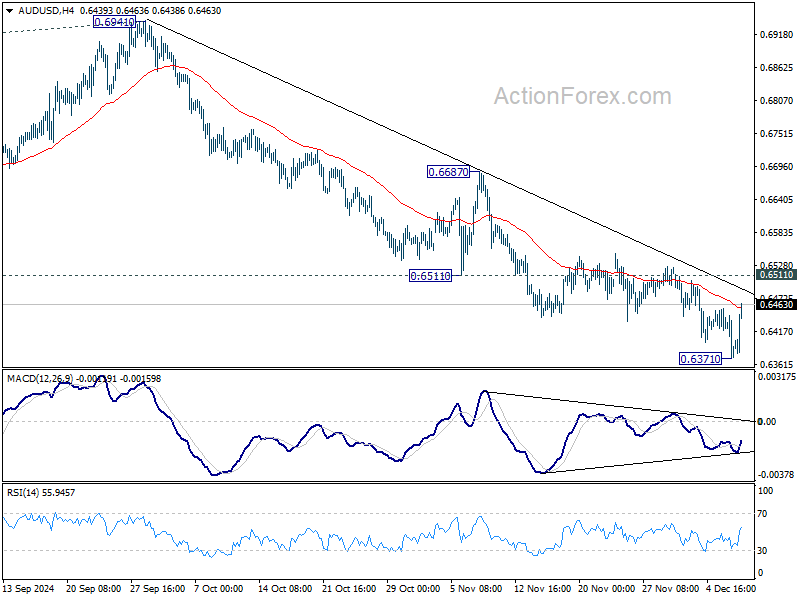

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6356; (P) 0.6407; (R1) 0.6441; More...

A temporary low should be in place at 0.6371 with today’s rebound and intraday bias is turned neutral first. Some consolidations would be seen but further decline is expected as long as 0.6511 support turned resistance holds. On the downside, below 0.6371 will resume the fall from 0.6941 to 0.6348 support, and then 0.6269. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.6511 will confirm short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6575) next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.