The forex markets remain subdued in Asian session, with all major pairs and crosses confined within yesterday’s tight ranges, and many still constrained within last week’s bounds. Among the majors, Australian Dollar is showing slight strength supported by hawkish RBA minutes, followed by Swiss Franc and Canadian Dollar. Meanwhile, Japanese Yen lags as the weakest performer, trailed by the Dollar and New Zealand Dollar, with Sterling and Euro positioned in neutral territory. However, the lack of clear directional movement reflects the ongoing consolidative phase.

Today’s primary focus will be on Canada’s inflation data. October’s headline CPI is projected to rise to 1.9%, while CPI common is expected to remain steady at 2.1%. These results would reinforce expectations that the BoC will maintain its swift easing path, likely cutting rates again by 50 bps at its December 11 meeting. October’s BoC rate cut and minutes highlighted the need for aggressive easing due to labor market softness and a requirement to stimulate growth to absorb economic slack. Market participants anticipate this approach to continue.

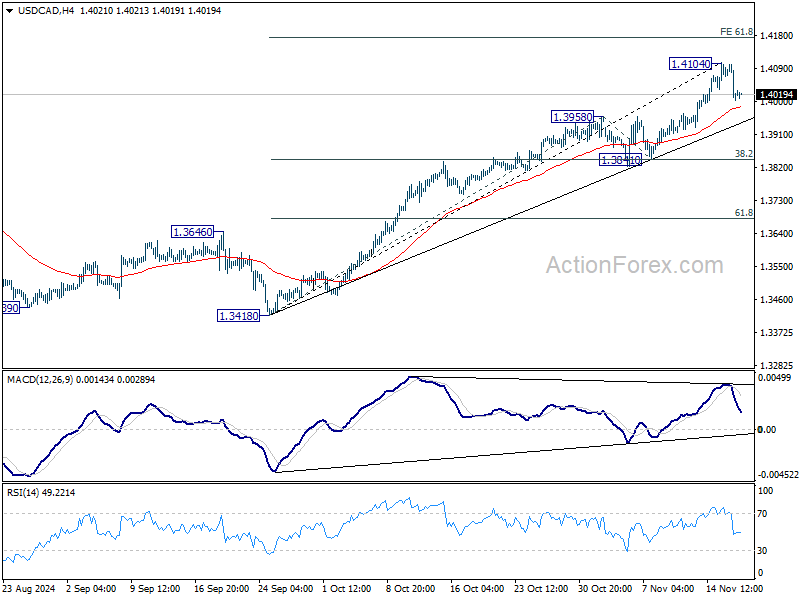

Technically, a temporary top was formed at 1.4104 in USD/CAD with current retreat. But consolidations should be relatively brief as long as 1.3958 resistance turned support holds. Break of 1.4104 will resume larger up trend to 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. However, firm break of 1.3958 will indicate that lengthier consolidation is underway, with risk of deeper pullback to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842).

In Asia, at the time of writing, Nikkei is up 0.36%. Hong Kong HSI is up 0.03%. China Shanghai SSE is down -0.92%. Singapore Strait Times is up 0.73%. Japan 10-year yield is down -0.0055 at 1.071. Overnight, DOW fell -0.13%. S&P 500 rose 0.39%. NASDAQ rose 0.60%. 10-year yield fell -0.014 to 4.414.

RBA minutes highlight need for multiple good quarterly inflation reports before easing

In the minutes from the November meeting, RBA emphasized “minimal tolerance” for a prolonged period of high inflation, acknowledging the already “lengthy period” of elevated prices. They underscored the need to observe “more than one good quarterly inflation outcome” before concluding that a sustainable disinflation trend was underway.

Members discussed various scenarios that could challenge the forecasts, necessitating adjustments in policy.

One critical scenario revolved around weaker consumption. If consumption proved “persistently and materially weaker” than anticipated and threatened to significantly lower inflation, RBA suggested that a rate cut might be warranted. Conversely, stronger recovery in consumption could mean the current monetary stance would need to “remain in place for longer”.

The labor market also featured prominently in deliberations. Should employment conditions ease more sharply than expected, resulting in rapid disinflation, the Board acknowledged that looser monetary policy might become appropriate. On the other hand, if the economy’s supply capacity turned out to be “materially more limited” than assumed, a tighter stance could be required.

External risks were also assessed, including potential major shifts in US economic policy following the presidential election, uncertainty around the scope of China’s anticipated stimulus measures, and the broader implications of rising global government debt levels.

BoE’s Greene cautions against aggressive rate cuts amid persistent services inflation and wage growth

BoE MPC member Megan Greene warned during an event overnight that services inflation remains stubbornly high, with wage growth exceeding levels consistent with the 2% inflation target. “There’s some risk that wage growth might be stickier than we would hope,” she said, adding that this could keep both services and overall inflation elevated.

Greene emphasized the importance of a cautious approach, stating that “the risk of cutting too early or too aggressively is a greater risk than going a bit more slowly.”

Feedback from firms suggests wage growth could settle closer to 4%, well above the desired level. Companies may respond to higher costs by increasing prices, reducing employment or hours, investing in productivity-enhancing capital, or absorbing costs into profit margins, she noted.

She also highlighted the UK’s vulnerability to external shocks as an open economy. “Historically speaking, about a third of the moves in our curve in the UK were influenced by things happening outside the UK. Now it’s about half.”

Greene pointed to the outsized influence of the US Treasury curve, describing it as a “drunken dragon” that heavily impacts the UK market, especially amid global geopolitical risks and shifts in US economic policy under the president-elect.

Looking ahead

Eurozone CPI final and Swiss trade balance will be released in European. Canada CPI will take center stage later in the day. US will release building permits and housing starts.

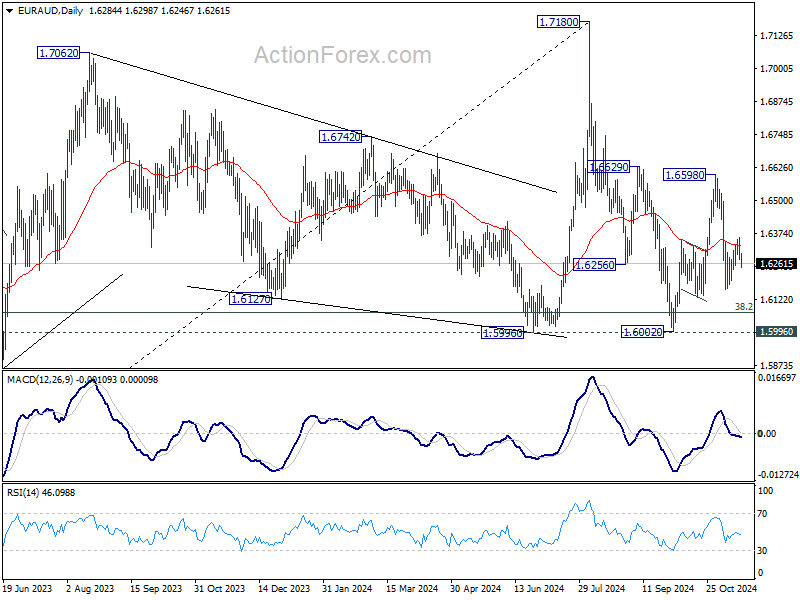

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6253; (P) 1.6307; (R1) 1.6340; More…

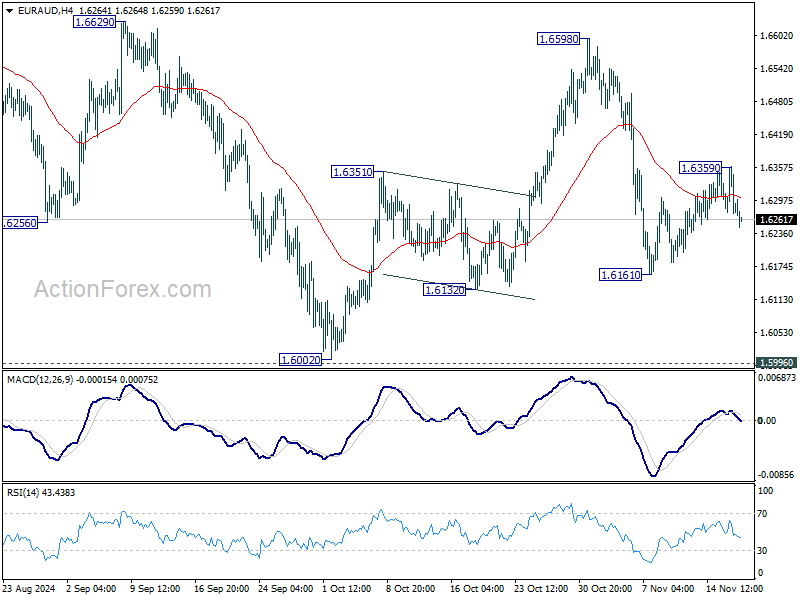

EUR/AUD weakens notably after failing to sustain above 55 D EMA, but downside is held well above 1.6161 temporary low. Intraday bias stays neutral and risk remains on the downside for the moment. On the downside, below 1.6161 will target a test on 1.5996/6002 key support zone. Nevertheless, break of 1.6359 will turn bias to the upside for stronger rebound towards 1.6598 resistance instead.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.