Yen weakened broadly during the Asian session today, as traders expressed disappointment with BoJ Governor Kazuo Ueda’s remarks. Ueda repeated familiar stances on monetary policy but refrained from offering any signals regarding a December rate hike. This lack of clarity left markets unimpressed. However, the currency’s losses have been modest so far, with its direction remains closely tied to overall risk sentiment. Yen showed strength late last week, buoyed by the sharp selloff in US equity markets, where island reversal patterns emerged in S&P 500 and NASDAQ. Should this negative stock market sentiment persist, it could provide a fresh catalyst for Yen appreciation in the near term.

Meanwhile, Kiwi is facing selling pressure, ranking among the weakest performer today so far. The disappointing services index reading from New Zealand added to the currency’s challenges. Expectations are firm for RBNZ to deliver another 50pbps rate cut next week. A significant factor influencing this expectation is RBNZ’s meeting calendar, as it will not convene again until mid-February 2025. This December/January gap could prompt the central bank to frontload further easing.

As for the month so far, Dollar is sitting at the top of the performance table, followed by Canadian Dollar, and then Yen. Euro is the worst performer, followed by Swiss Franc and then Sterling. Aussie and Kiwi are mixed in the middle. The Pound and Loonie will look into this week’s CPI data for the next month. Meanwhile, Euro would hope to have some help from Eurozone PMI data.

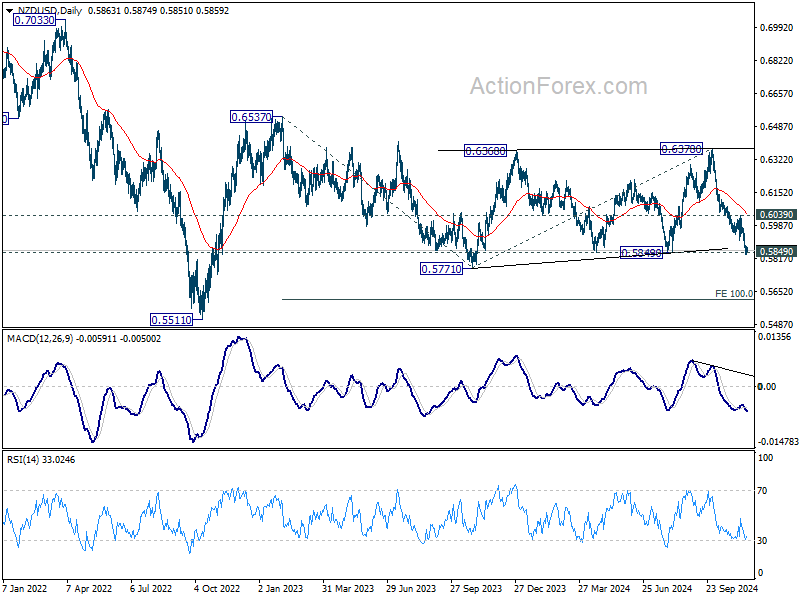

Technically, NZD/USD is now pressing 0.5849 structural support as fall from 0.6378 extended last week. Decisive break there will likely resume the whole down trend from 0.6537 (2023 high) through 0.5771 support to 100% projection of 0.6537 to 0.5771 from 0.6378 at 0.5612. In any case, near term outlook will stay bearish as long as 0.6039 resistance holds.

In Asia, at the time of writing, Nikkei is down -1.04%. Hong Kong HSI is up 0.84%. China Shanghai SSE is up 0.27%. Singapore Strait Times is down -0.05%. Japan 10-year JGB yield is down -0.0019 at 1.073.

BoJ’s Ueda Highlights wages as key inflation driver, reaffirms tightening path

BoJ Governor Kazuo Ueda reiterated in a speech today that the central bank remains committed to its gradual policy tightening path, conditional on the realization of its economic and price outlook. However, the timing of adjustments will depend on evolving “economic activity and prices” as well as “financial conditions.”

Ueda stated that monetary policy decisions would hinge on assessments at each Monetary Policy Meeting, taking into account the latest data and projections. Key considerations include underlying inflation trends and financial conditions, with a focus on balancing risks to economic activity.

On inflation, Ueda highlighted that the effects of previous cost pass-throughs from higher import prices are waning. However, he noted that “inflationary pressure stemming from wage increases is projected to strengthen” as economic activity and wage growth remain robust.

While underlying inflation currently lags the 2% target, it is expected to rise moderately and align with the price stability target in the second half of the projection period through fiscal 2026.

NZ BNZ services rises to 46, still extremely challenging conditions

New Zealand’s BusinessNZ Performance of Services Index rose slightly from 45.7 to 46.0 in October. Despite the marginal improvement, the index stayed well below the 50 threshold, indicating ongoing contraction in the sector for a fourth consecutive month. The result also falls significantly short of the long-term average of 53.1.

The proportion of respondents reporting negative sentiment increased from 58.5% to 59.1%. Concerns about the cost of living and broader economic challenges continued to dominate.

BNZ Senior Economist Doug Steel emphasized the sector’s struggles, stating that “although it is contracting at a much slower pace than it was in June (when the PSI was 41.1), the PSI has been hovering between 45 and 46 over the last four months.” He noted that while some business surveys indicate an improving outlook, current conditions remain “extremely challenging”.

Inflation Data and PMIs in Focus

This week, market focus shifts to inflation data from the UK, Canada, and Japan, alongside key PMI releases from major economies. Central banks’ paths remain under scrutiny, with inflation trends and economic activity offering crucial insights.

In the UK, the unexpected September GDP contraction and rise in unemployment rate may embolden dovish voices within BoE. However, a departure from the current “gradual approach” to policy adjustments appears unlikely at this juncture give the inflation risks

UK headline CPI is expected to jump from 1.7% to 2.2% in October, surpassing 2% target again, while core CPI is likely to remain elevated above 3%. BoE Governor Andrew Bailey previously noted that services inflation is declining only gradually, with substantial relief not expected until 2025. Adding complexity, uncertainties linked to measures in the Autumn Budget reinforce the central bank’s cautious stance.

In Canada, October’s inflation data is expected to show headline CPI rising from 1.6% to 1.9%, while core measures may hold steady or edge lower. These dynamics provide BoC ample room to proceed further with its easing cycle. Markets anticipate another 50bps rate cut in December, bringing the policy rate closer to a neutral level from its current 3.75%.

Japan’s inflation data presents a contrasting narrative. CPI core inflation is projected to decline for the second consecutive month, from 2.4% to 2.2%, reflecting the waning effects of prior cost-push pressures. While BoJ Governor Kazuo Ueda has reaffirmed the central bank’s commitment to gradual tightening, he remains non-committal about the timing of further rate hikes. Wage growth in 2025 will be critical to shaping BoJ’s future policy, but for now, attention remains on trends in services and core-core inflation as indicators of underlying price stability.

PMI data from Australia, Japan, the Eurozone, the UK, and the US will also draw significant attention. The Eurozone, in particular, is under scrutiny after recent ECB meeting accounts highlighted downside risks to inflation stemming from sluggish economic activity. Failure of PMI figures to signal an economic rebound could solidify expectations for another ECB rate cut in December.

On the central bank front, RBA minutes could offer insights into the board’s decision to maintain its vigilance on inflation risks. Speculation is mounting that RBA may delay its first rate cut from February to May 2025. The minutes will likely provide clarity on whether this stance is gaining broader support within the board.

Here are some highlights for the week:

- Monday: New Zealand BNZ services, PPI; Japan machine orders; Eurozone trade balance; Canada housing starts; US NAHB housing index.

- Tuesday: RBA minutes; Swiss Trade balance; Eurozone current account, CPI final; Canada CPI; US housing starts and building permits.

- Wednesday: Japan trade balance; Germany PPI; UK CPI, PPI.

- Thursday: UK public sector net borrowing; Canada IPPI, RMPI; US jobless claims, Philly Fed survey, existing home sales, leading indicators.

- Friday: Australia PMIs; Japan CPI, PMI manufacturing flash; Germany GDP final; UK retail sales, PMI flash; Eurozone PMI flash; Canada retail sales; US PMI flash.

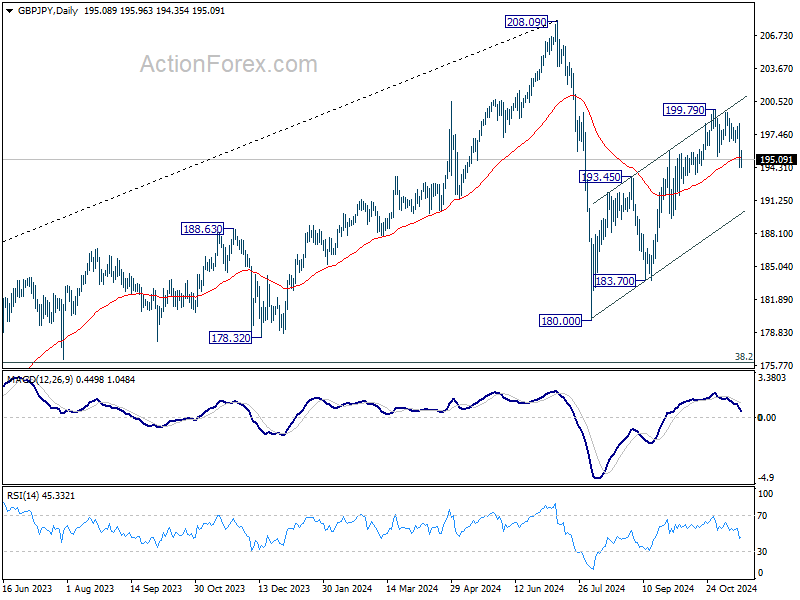

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.21; (P) 195.83; (R1) 197.37; More…

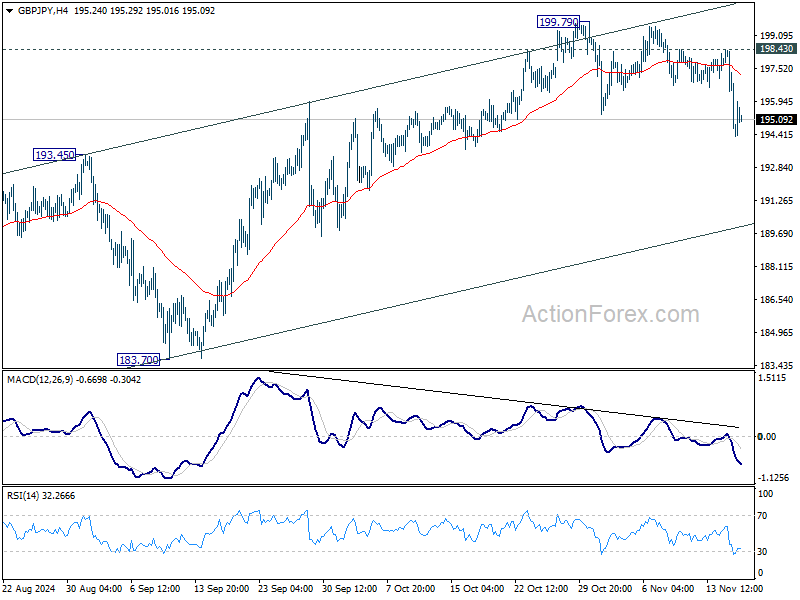

Intraday bias in GBP/JPY stays on the downside despite today’s weak recovery. Prior break of 55 D EMA (now at 195.23) argues that corrective rise from 180.00 has completed with three waves up to 199.79, after hitting rising channel resistance. Further decline would be seen to 193.45 resistance turned support. Decisive break there will target 183.70 next. For now, risk will stay on the downside as long as 198.43 resistance holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.