UPCOMING

EVENTS:

- Monday: US NAHB Housing Market Index.

- Tuesday: RBA Meeting Minutes, Canada CPI, US Housing

Starts and Building Permits. - Wednesday: PBoC LPR, UK CPI, Eurozone Wage Growth.

- Thursday: Canada PPI, US Jobless Claims.

- Friday: Australia/Japan/EU/UK/US Flash PMIs, Japan CPI,

UK Retail Sales, Canada Retail Sales.

Tuesday

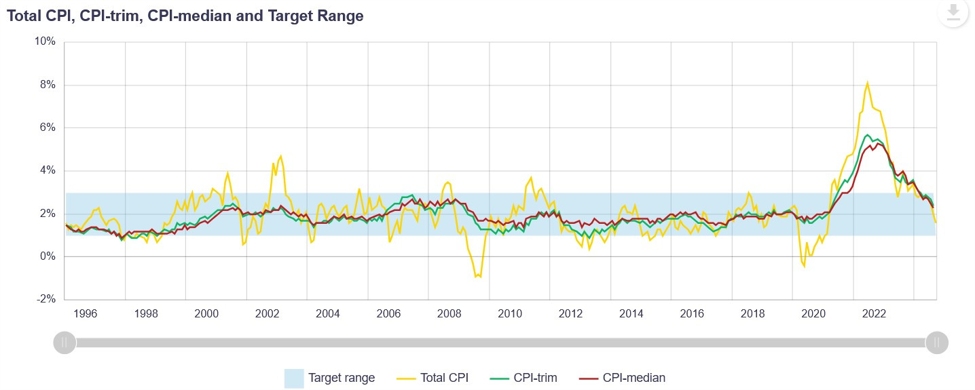

The Canadia CPI

Y/Y is expected at 1.9% vs. 1.6% prior, while the M/M figure is seen at 0.3%

vs. -0.4% prior. The focus will be on the underlying inflation measures with

the Trimmed Mean CPI Y/Y expected at 2.4% vs. 2.4% prior, while the Median CPI

Y/Y is seen at 2.4% vs. 2.3% prior.

The BoC is now focused

on growth as inflation has been inside the target band for several months while

economic activity slowed down. The market is pricing a 35% chance of another 50

bps cut in December, so lower than expected inflation readings will likely

raise those probabilities.

Canada Inflation Measures

Wednesday

The PBoC is

expected to keep the LPR rates unchanged at 3.1% for the 1 year and 3.6% for

the 5 year. Deflationary forces remain in place and the market continues to

signal that they need to do more.

The PBoC pledged

more monetary policy support with another cut in the reserve requirement ratio

to accommodate additional government bond issuance likely coming by the end of

the year. The central bank should do much more though as real interest rates

are still too high.

PBoC

The UK CPI Y/Y is

expected at 2.2% vs. 1.7% prior, while the M/M figure is seen at 0.5% vs. 0.0%

prior. The Core CPI Y/Y is expected at 3.2% vs. 3.2% prior. Last time, the UK inflation data missed expectations by a big margin with

services inflation dropping to 4.9% from 5.6% in the prior month.

In the meantime,

we’ve also got a soft labour market report and a lower than expected GDP

print. The market is currently pricing just a 22% probability of another 25 bps

cut in December, but that should increase if we were to get another miss in the

CPI data.

UK Core CPI YoY

Thursday

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

after a spike to the cycle highs in the last couple of weeks due to distortions

coming from hurricanes and strikes, are now turning around.

This week Initial

Claims are expected at 223K vs. 217K prior, while there’s no consensus for

Continuing Claims at the time of writing although the prior reading saw a

decrease to 1873K vs. 1884K prior.

US Jobless Claims

Friday

Friday is going to

be the Flash PMIs Day for many major economies. The market is going to focus

majorly on the Eurozone, UK and US PMIs as they are likely to influence the

interest rate expectations:

- Eurozone Manufacturing PMI: 46.0 expected vs. 46.0

prior. - Eurozone Services PMI: 51.5 expected vs. 51.6

prior. - UK Manufacturing PMI: 49.9 expected vs. 49.9

prior. - UK Services PMI: 52.0 expected vs. 52.0 prior.

- US Manufacturing PMI: 48.8 expected vs. 48.5

prior. - US Services PMI: 55.3 expected vs. 55.0 prior.

PMI

The Japanese Core

CPI Y/Y is expected at 2.2% vs. 2.4% prior. Inflation isn’t really an issue for

Japan as the underlying measures are basically at target. Nonetheless, the

probabilities for a rate hike in December increased to 55% recently as the

Japanese Yen continued to depreciate non-stop due to the rally in Treasury

yields. One of the main reasons why the BoJ hiked rates last time was the fast

depreciation of the JPY.

Japan Core CPI YoY