Dollar’s rally continues broadly today, though most of its strength remains concentrated against European majors. While the greenback holds firm, it remains capped below last week’s highs against commodity-linked currencies and Yen. A clear move upwards could only unfold if 10-year Treasury yield breaks past the 4.4% threshold, though the true direction may hinge on tomorrow’s US CPI release, which could determine near-term policy expectations.

Among European currencies, Euro is under particular pressure. Disappointing German ZEW economic sentiment report has added to concerns that Germany’s fragile recovery could face further challenges amid anticipated US trade policy shifts. Sterling is also feeling the weight of higher UK unemployment rate, which signals some labor market loosening. However, with wage growth still elevated, BoE appears far from pursuing an aggressive policy easing path. The softening job market, though, does provide a slight cushion against inflation.

This week so far, Yen leads losses, followed by Euro and Sterling, while Dollar leads gains, trailed by Canadian and Australian Dollars. Kiwi and Swiss Franc sit in middle positions.

Technically, with today’s strong rally, 10-year yield looks set to take on key resistance level at 61.8% retracement of 4.997 to 3.603 at 4.464 within the course of the week. Decisive break there would strengthen the case that whole correction from 4.997 has completed with three waves down to 3.603. Stronger rise should then be seen to 4.737 resistance next, and this should take Dollar higher too. However, another rejection by 4.465, followed by 4.223 support bring deeper pullback to 55 D EMA (now at 4.102) and possibly below.

In Europe, at the time writing, FTSE is down -0.80%. DAX is down -0.93%. CAC is down -1.26%. UK 10-year yield is up 0.046 at 4.473. Germany10-year yield is up 0.020 at 2.348. Earlier in Asia, Nikkei fell -0.40%. Hong Kong HSI fell -2.84%. China Shanghai SSE fell -1.39%. Singapore Strait Times fell -0.75%. Japan 10-year JGB yield rose 0.0078 at 1.009.

German ZEW slumps to 7.4, domestic political uncertainty and US election outcome

German ZEW Economic Sentiment index took a significant hit in November, plunging from 13.1 to a mere 7.4, sharply missing expectations of 13.2. Current Situation Index also declined, falling from -86.9 to -91.4, below the anticipated -86.0.

The broader Eurozone felt the impact as well, with its ZEW Economic Sentiment index dropping from 20.1 to 12.5, and the Current Situation Index slipping by 3.0 points to 43.8.

ZEW President Achim Wambach highlighted that the drop in German economic expectations was heavily influenced by two recent developments: Donald Trump’s election victory and the collapse of Germany’s government coalition.

According to Wambach, “Economic sentiment has declined – and the outcome of the US presidential election is likely to be the main reason for this.” The survey data reflect rising optimism toward the US, while sentiment for China and Eurozone continues to deteriorate, reinforcing concerns of broader instability.

ECB’s Rehn: May exit restrictive policy as soon as late winter

Speaking at a conference today, Finnish ECB Governing Council member Olli Rehn reiterated that the direction of monetary easing is “clear”. However, he emphasized that the “speed and scope ” of these cuts will be determined by a trio of factors evaluated at each ECB meeting: the inflation outlook, underlying inflation trends, and the efficacy of monetary policy transmission.

Rehn pointed to the possibility of reducing the ECB’s deposit rate, currently at 3.25%, to a neutral level. Such adjustments could occur by late winter or early spring if the data supports it.

“Current market data and simple maths seem to imply that we would leave restrictive territory sometime in the spring/winter next year 2025,” Rehn said. “But that is just an observation from my side, not a commitment.”

BoE’s Pill cites persistent pay growth and underlying inflationary pressures

At a conference today, BoE Chief Economist Huw Pill referred to today’s UK labor market data, noted that wage growth remains “quite sticky at elevated levels,” which he characterized as “hard to reconcile” with the inflation target, given current productivity growth expectations.

While acknowledging the significant disinflation seen in recent months, which has allowed for a reduction in monetary policy restrictions, Pill cautioned that “does not mean it is job done”.

He emphasized that despite some easing in headline inflation, “some underlying inflationary pressures” persist in the UK economy.

Mixed UK labor data as unemployment rate and earnings growth climbs

In October, UK employment data indicated slight weakening in the labor market, with payrolled employees decreasing by -5k or -0.0% mom to a total of 30.4m. Comparing to the same month a year ago, payrolled employment rose 95k or 0.3% yoy. However, the claimant count for job-related benefits rose by 26.7k to reach 1.806mn, smaller than expectations of a 30.5k increase.

In the three months to September, unemployment rate climbed from 4.0% to 4.3%, higher than the anticipated 4.1%. On the earnings front, total average earnings, including bonuses, rose by 4.8% yoy, outpacing both the previous 3.9% growth and market forecasts. Excluding bonuses, average earnings grew by 4.8% yoy, marginally down from 4.9% yoy in the prior period but still above the projected 4.7% yoy.

Australian Westpac consumer sentiment jumps 5.3%, but US election casts shadow on outlook

Australian consumer sentiment saw a solid rebound in November, with Westpac Consumer Sentiment Index climbing by 5.3% mom to reach 94.6. This marks a 14.4% rise from its mid-year low, leaving it just 5.4 points shy of the neutral 100 mark.

The improvement was led by increased optimism about the short-term economic outlook. The “economic outlook, next 12 months” sub-index jumped 8.7% to 100.9, the first optimistic reading (above 100) since post-COVID recovery. Confidence around personal finances also strengthened, with the “family finances, next 12 months” sub-index up 4.4% to 104.1. Meanwhile, Unemployment Expectations Index dropped by -7.2% to 120.5, indicating the highest level of labor market confidence since April 2023.

Westpac noted three important observations in November’s sentiment trends. First, confidence reached 99.7 in the early survey period, prior to RBA’s rate decision, reflecting marked optimism. Secondly, consumer sentiment remained unaffected by RBA’s decision to hold rates steady. Lastly, sentiment dropped sharply after US election result, averaging 91.1 in the survey’s latter half. This indicates an unusually wide range of ±5% for November’s final read, suggesting a degree of uncertainty not typically seen.

Australian NAB business confidence surges to 5, easing cost pressures but persistent retail inflation

Australia’s NABs Business Confidence Index jumped from -2 to 5, marking a notable improvement after a prolonged period of below-average sentiment. Business conditions remained stable at 7, while trading conditions saw a slight increase from 12 to 13. Profitability held steady at 5, and employment conditions edged lower from 5 to 3.

Gareth Spence, NAB’s Head of Australian Economics, highlighted the jump in confidence as an encouraging development, noting that it is “just one month” but shows “tentative improvement” in forward orders, suggesting possible momentum.

Input cost pressures continued to ease, with labor cost growth decelerating from 1.9% to 1.4% on a quarterly basis from 1.9%, and purchase cost growth slowing from 1.3% to 0.9%. Retail price growth, however, saw a rebound, rising from 0.6% to 1.1%.

Spence noted, “The survey, like other price indicators, continues to suggest an ongoing gradual easing in inflation pressure, but also that there is still some way to go in in the inflation moderation when we look at the consumer facing components”.

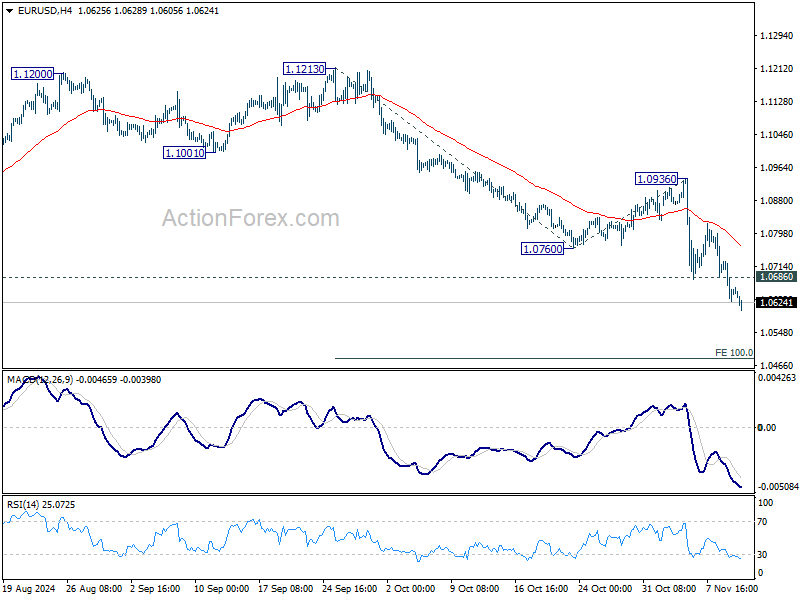

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0614; (P) 1.0671; (R1) 1.0713; More…

EUR/USD’s fall from 1.1213 is in progress and intraday bias stays on the downside. Next target is100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483. On the upside, above 1.0686 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0760 support turned resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.