Risk-on sentiment returned to global markets again in early US trading, driven by lower-than-expected inflation data. While annual PCE core inflation edged up to 2.7%, the monthly increase was a modest 0.1%. This tamer monthly inflation growth suggests that underlying price pressures would, at least, not obstruct Fed’s to another aggressive rate cut at its next meeting. However, upcoming non-farm payrolls and CPI data will still play a decisive role in Fed’s final decision.

In Japan, Yen staged a sharp turnaround after Shigeru Ishiba unexpectedly secured leadership of the ruling Liberal Democratic Party, setting him on the path to become the next Prime Minister. Known for his hawkish monetary stance, Ishiba’s ascent has intensified speculation that BoJ may implement another rate hike in December. However, the political landscape remains uncertain. There is a possibility that Ishiba may call for a snap general election to secure a stronger mandate from voters, and that could delay any BoJ action until 2025.

For the week, Kiwi and Aussie remain the top performers, with the Swiss Franc catching up as the third strongest due to today’s rebound. Dollar has become the weakest currency as Yen recovers. Euro and Sterling are also underperforming, while Yen and Loonie are positioned in the middle of the currency spectrum.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 1.20%. CAC is up 0.59% UK 10-year yield is down -0.0528 at 3.964. Germany 10-year yield is down -0.054 at 2.130. Earlier in Asia, Nikkei rose 2.32%. Hong Kong HSI rose 3.55%. China Shanghai SSE rose 2.88%. Singapore Strait Times fell -0.25%. Japan 10-year JGB yield fell -0.0239 to 0.807.

US PCE inflation falls to 2.2% in Aug, core PCE ticks up to 2.7%

US personal income rose USD 50.5B or 0.2% mom in August, below expectation of 0.4% mom. Personal spending rose USD 47.2B or 0.2% mom, below expectation of 0.3% mom.

PCE price index rose 0.1% mom, matched expectations while core PCE (excluding food and energy)price index rose 0.1% mom,m below expectation of 0.2% mom. Good prices fell -0.2% mom while services prices rose 0.2% mom. Food prices rose 0.1% mom and energy prices fell -0.8% mom.

From the same month a year ago, PCE price growth slowed from 2.5% yoy to 2.2% yoy, below expectation of 2.3% yoy. Core PCE price growth accelerated fro 2.6% yoy to 2.7% yoy, matched expectations. Prices for goods decreased -0.9% yoy and prices for services increased 3.7% yoy. Food prices increased 1.1% yoy and energy prices -decreased 5.0% yoy.

Canada’s GDP grows 0.2% mom in Jul essentially unchanged in Aug

Canada’s GDP grew 0.2% mom in July, above expectation of 0.1% mom. Services-producing industries grew 0.2% mom while goods- producing industries rose 0.1% mom. Overall, 13 of 20 sectors expanded in July.

Advance information indicates that real GDP was essentially unchanged in August. Increases in oil and gas extraction and the public sector were offset by decreases in manufacturing and transportation and warehousing.

Eurozone economic sentiment dips slightly to 96.2

Eurozone Economic Sentiment Indicator fell slightly from 96.5 to 96.2 in September. Employment Expectations Indicator ticked up from 99.4 to 99.5. Economic Uncertainty Indicator rose from 17.5 to 17.8. Industry confidence fell from -9.9 to -10.9. Services confidence rose from 6.4 to 6.7. Consumer confidence rose from -13.4 to -129. Retail trade confidence fell from -7.9 to -8.5. Construction confidence rose from -6.3 to -5.8.

EU Economic Sentiment Indicator was unchanged at 96.7. For the largest EU economies, the ESI worsened markedly in France (-1.4) and Germany (-1.2), while it improved significantly in Poland (+2.0), Spain (+1.9), Italy (+1.2) and, more moderately, in the Netherlands (+0.5).

Japan’s Tokyo core inflation slows to 2%, supporting BoJ’s cautious approach

Japan’s Tokyo CPI core (excluding fresh food) slowed from 2.4% yoy to 2.0% yoy in September, aligning with expectations and marking its lowest level since May. Headline CPI dropped to 2.2% yoy from 2.6% yoy , while CPI core-core (excluding food and energy) remained stable at 1.6% yoy.

The primary driver of the deceleration in inflation was reduction in electricity and gas prices, influenced by government energy subsidies reintroduced by outgoing Prime Minister Fumio Kishida. These subsidies helped alleviate the impact of a particularly hot summer, shaving 0.5 percentage points off overall inflation.

This data, especially the stable core-core inflation, supports BoJ’s cautious stance regarding more tightening. BoJ Governor Kazuo Ueda recently noted that inflationary risks have diminished, particularly with Yen’s recent gains. BoJ is likely to remain on hold during its upcoming policy meeting on October 31.

PBoC cuts RRR and repo rate

In a follow-up to Governor Pan Gongsheng’s earlier remarks this week, the People’s Bank of China announced today a 50bps cut in the reserve requirement ratio and a 20bps reduction in the seven-day reverse repurchase rate.

This move is intended to release approximately CNY 1T in long-term liquidity, enabling banks to lend more and increase purchases of government bonds aimed at funding infrastructure projects. With the cut, the weighted average RRR will drop to around 6.6%. The central bank also lowered the seven-day reverse repo rate from 1.7% to 1.5%.

Further fiscal measures are anticipated before China’s National Day holiday on October 1, as the Politburo has signaled a heightened focus on addressing economic pressures.

Reports indicate that the government will raise CNY 1T via special bonds, which will fund consumer goods subsidies, upgrades to business equipment, and provide a monthly allowance of CNY 800 yuan per child for households with multiple children. Additionally, another CNY 1T in special sovereign debt could be issued to help local governments manage their mounting debt burdens.

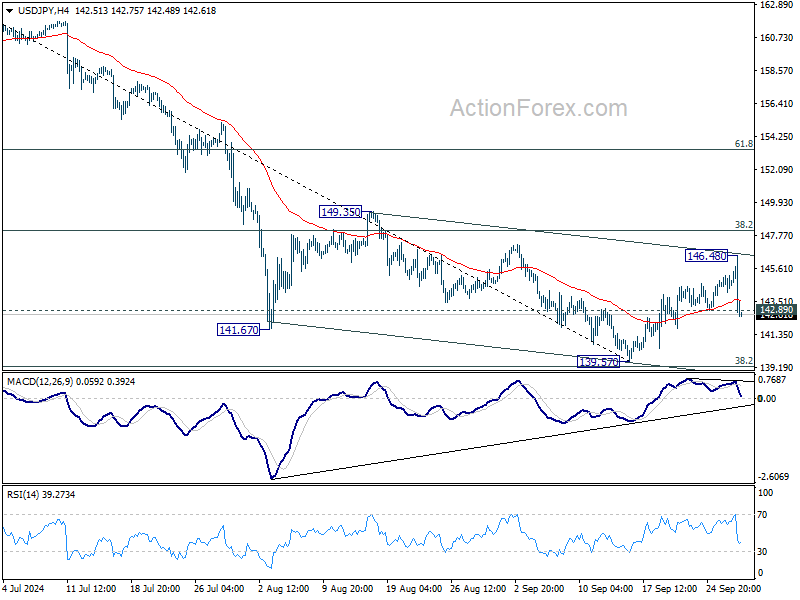

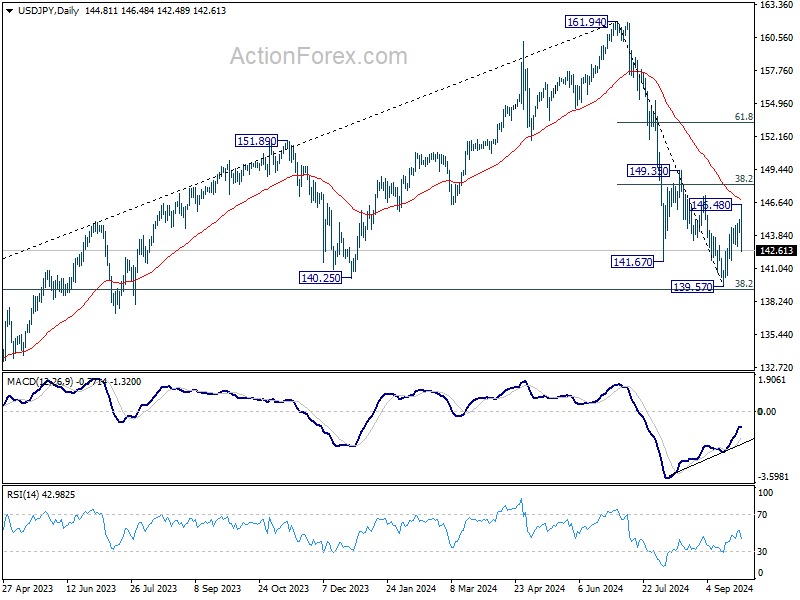

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.21; (P) 144.71; (R1) 145.31; More…

USD/JPY’s break of 142.89 minor support suggests that recovery fro 139.57 has completed at 146.48 already. Intraday bias is back on the downside for 139.57 low. Strong support is still expected from 139.26 to contain downside to bring another rebound. But decisive break there will carry larger bearish implications. On the upside, above 146.48 will resume the rebound to 38.2% retracement of 161.94 to 139.57 at 148.11.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Sep | 2.20% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | 2.00% | 2.00% | 2.40% | |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Sep | 1.60% | 1.60% | ||

| 06:45 | EUR | France Consumer Spending M/M Aug | 0.20% | -0.10% | 0.30% | 0.20% |

| 07:55 | EUR | Germany Unemployment Rate Sep | 6.00% | 6.00% | 6.00% | |

| 07:55 | EUR | Germany Unemployment Change Sep | 17K | 9K | 2K | |

| 09:00 | EUR | Eurozone Economic Sentiment Sep | 96.2 | 96.5 | 96.6 | 96.5 |

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -10.9 | -9.8 | -9.7 | -9.9 |

| 09:00 | EUR | Eurozone Services Sentiment Sep | 6.7 | 5.6 | 6.3 | 6.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -12.9 | -12.9 | -12.9 | |

| 12:30 | CAD | GDP M/M Jul | 0.20% | 0.10% | 0.00% | |

| 12:30 | USD | Personal Income M/M Aug | 0.20% | 0.40% | 0.30% | |

| 12:30 | USD | Personal Spending Aug | 0.20% | 0.30% | 0.50% | |

| 12:30 | USD | PCE Price Index M/M Aug | 0.10% | 0.10% | 0.20% | |

| 12:30 | USD | PCE Price Index Y/Y Aug | 2.20% | 2.30% | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 2.70% | 2.70% | 2.60% | |

| 12:30 | USD | Goods Trade Balance (USD) Aug P | -94.3B | -100.6B | -102.7B | |

| 12:30 | USD | Wholesale Inventories Aug P | 0.20% | 0.20% | 0.20% | |

| 14:00 | USD | Michigan Consumer Sentiment Sep F | 69 | 69 |