Sterling climbed broadly today, fueled by unexpectedly strong UK retail sales data that more than compensated for the lackluster consumer confidence report. Despite ongoing high interest rates and persistent inflation, British consumers appear to be resilient, continuing to spend. This bolsters the position of hawkish members within the BoE’s MPC, who may push harder for a measured, gradual approach to reducing interest rates.

Looking at the broader market, Australian Dollar has maintained its position as the top performer for the week, driven by post-FOMC risk-on sentiment. However, with risk appetite fading as the weekend approaches, Sterling, currently in second place, has a real chance of overtaking the Aussie. Meanwhile, New Zealand Dollar follows closely as the third strongest currency this week.

On the downside, Japanese Yen remains the weakest performer, extending its selloff after BoJ’s decision to hold rates steady earlier today. The rise in US and European bond yields has further weighed on the Yen, as the growing yield differential makes it less attractive. Dollar and Swiss Franc are also under pressure, lacking the safe-haven appeal in the current risk-on environment. Euro and Canadian Dollar remain relatively mixed in the middle.

In Europe, at the time of writing, FTSE is down -0.85%. DAX is down -0.74%. CAC is down -0.77%. UK 10-year yield is up 0.0041 at 3.897. Germany 10-year yield is up 0.005 at 2.207. Earlier in Asia, Nikkei rose 1.53%. Hong Kong HSI rose 1.36%. China Shanghai SSE rose 0.03%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.0106 to 0.864.

Canada’s retail sales rises 0.9% mom, 7 of 9 subsectors grow

Canada’s retail sales rose 0.9% mom to CAD 66.4B in July, well above expectation of 0.5% mom. Sales were up in seven of nine subsectors, led by increases at motor vehicle and parts dealers. In volume terms, sales were also up 1.0% mom.

Advance estimate suggests that sales increased 0.5% mom in August.

ECB’s de Guindos keeps all option open data will drive future rate cuts

In an interview with Expresso, ECB Vice President Luis de Guindos reaffirmed the central bank’s cautious approach regarding rate cuts in the upcoming meetings. He stressed that ECB remains “fully committed” to a data-dependent strategy, making decisions on a “meeting-by-meeting” basis.

While he acknowledged the possibility of cuts in both October and December, De Guindos highlighted that December would provide a clearer picture. “We will have more information and a new round of projections,” he noted.

Nevertheless, he emphasized ECB plans to keep “all options open” to retain flexibility, with future moves hinging entirely on evolving economic data.

BoE’s Mann favors extended tight policy before swift, aggressive cuts

In a speech today, BoE MPC member Catherine Mann emphasized the importance of a cautious approach to easing monetary policy, stating that it’s preferable to remain restrictive longer amid inflation uncertainties.

She argued that “a risk management assessment implies it is better, under inflation uncertainty, to remain restrictive for longer, until right tail risks to the inflation process dissipate, and then to cut more aggressively.”

This “more activist strategy”, according to her, would allow for a sustainable inflation outcome with less impact on the economy, as she mentioned it helps achieve the target “at a lower sacrifice ratio.”

Despite agreeing with the majority of the MPC members on holding rates steady in the latest meeting, Mann has expressed a “guarded view” on starting the cutting cycle. Having voted against the 25bps rate cut in August, Mann again voted to hold yesterday.

UK retail sales grows 1% mom in Aug, annual growth highest since Feb 2022

UK retail sales volumes surged 1.0% mom in August, significantly outpacing the expected 0.3% mom growth. This marked the highest sales index level since July 2022. Over the broader three-month period ending in August, sales volumes increased by 1.2% compared to the previous three months.

On an annual basis, sales volumes jumped 2.5% yoy, marking the largest annual rise since February 2022. However, despite these strong gains, retail sales volumes remain -0.4% below their pre-pandemic levels from February 2020.

UK Gfk consumer confidence plummets to -20 ahead of expected painful budget

UK GfK Consumer Confidence dropped sharply in September, falling from -13 to -20, marking the biggest decline since April 2022. The seven-point drop reflects growing concerns about the economic outlook and personal finances, with households bracing for a difficult budget next month.

Key forward-looking indicators worsened significantly. Expectations for the general economy over the next 12 months dropped by -12 points to -27, while personal finance expectations fell by -9 points to -3. The major purchase index, which gauges consumers’ willingness to buy big-ticket items, also dropped -10 points to -23.

GfK noted, “Despite stable inflation and the prospect of further rate cuts, this is not encouraging news for the UK’s new government.” Neil Bellamy, Consumer Insights Director at GfK, linked the drop to concerns over Prime Minister Keir Starmer’s warnings of a “painful” budget. Bellamy said, “Consumers are nervously awaiting the Budget decisions on Oct. 30 after the withdrawal of winter fuel payments and warnings of further difficult measures.”

BoJ stands pat at 0.25%, sees gradual inflation rise and economic growth

BoJ left its uncollateralized overnight call rate unchanged at around 0.25% during today’s meeting, as widely anticipated and decided by unanimously.

In the accompanying statement, BoJ maintained a positive outlook for the Japanese economy, projecting continued growth at a rate above its potential. The central bank expects “overseas economies will continue to grow moderately,” further supporting Japan’s economic expansion. Domestically, the “virtuous cycle from income to spending” will gradually intensify, aided by accommodating financial conditions.

On the inflation front, core CPI is forecast to rise through fiscal 2025. BoJ also noted that underlying inflation will “increase gradually” as output gap narrows and medium- to long-term inflation expectations firm up.

However, the central bank also outlined several risks to its outlook, including global economic developments, commodity prices, and the pace at which firms adjust wage and price setting.

Japan’s CPI core rises to 2.8% in Aug, core-core up to 2.0%

Japan’s core CPI, excluding fresh food, rose to 2.8% yoy in August, matching expectations and marking the fourth consecutive month of acceleration. This increase is up from 2.7% yoy in July and continues the upward trend from 2.2% yoy in April, keeping inflation above BoJ’s 2% target since April 2022.

Core-core CPI, which strips out both fresh food and energy, also rose from 1.9% yoy to 2.0% yoy, highlighting broader inflationary pressures in Japan. Headline CPI, which includes all categories, increased from 2.8% yoy to 3.0% yoy.

Energy prices surged 12.0% yoy, while food prices increased by 2.9% yoy, and household durable goods saw a significant rise of 7.7% yoy. These numbers indicate persistent inflationary pressures across a wide range of goods and services.

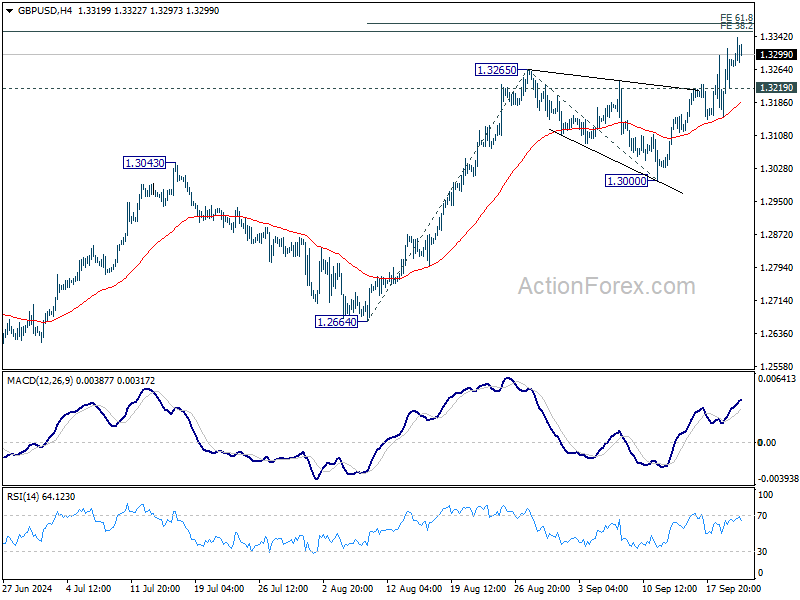

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3188; (P) 1.3251; (R1) 1.3349; More…

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, below 1.3219 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3000 support holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Sep | -20 | -13 | -13 | |

| 23:30 | JPY | CPI Y/Y Aug | 3.00% | 2.80% | ||

| 23:30 | JPY | CPI Core Y/Y Aug | 2.80% | 2.80% | 2.70% | |

| 23:30 | JPY | CPI Core-Core Y/Y Aug | 2.00% | 1.90% | ||

| 01:00 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.35% | 3.35% | |

| 01:00 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.85% | 3.85% | |

| 02:52 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 06:00 | EUR | GermanyPPI M/M Aug | 0.20% | 0.00% | 0.20% | |

| 06:00 | EUR | GermanyPPI Y/Y Aug | -0.80% | -1.00% | -0.80% | |

| 06:00 | GBP | Retail Sales M/M Aug | 1.00% | 0.30% | 0.50% | 0.70% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 13.7B | 12.3B | 2.2B | 3.1B |

| 12:30 | CAD | Retail Sales M/M Jul | 0.90% | 0.50% | -0.30% | -0.20% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 0.40% | 0.20% | 0.30% | |

| 12:30 | CAD | Industrial Product Price M/M Aug | -0.80% | -0.30% | 0.00% | -0.10% |

| 12:30 | CAD | Raw Material Price Index Aug | -3.10% | -2.00% | 0.70% | |

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -13 | -13 |

for beginner #shorts #crypto #forex #patterns #trading

for beginner #shorts #crypto #forex #patterns #trading