Trading in the forex markets continued to be relatively subdued, as the initial buzz surrounding a Fed rate cut in September is quickly dissipating. Although there is still some speculation about the possibility of a more aggressive 50bps cut to kick off the easing cycle, the repeated reassurances from Fed officials about a preference for a gradual approach have dampened expectations. It seems increasingly likely that only a significantly disappointing non-farm payroll report on September 6 could prompt a more forceful move from Fed. However, such negative news could also dampen investor confidence, leading to broader market concerns.

So far this week, Canadian Dollar and Swiss Franc are the stronger performers, largely driven by heightened geopolitical tensions that have also contributed to a spike in oil prices. The risk for a broader conflict in the Middle East appeared to ease after Israel and Lebanon’s Hezbollah exchanged fire without further escalation. However, fresh concerns have surfaced with reports of Russia launching missile and drone attacks overnight, targeting Kyiv and other regions.

On the weaker side, Kiwi, Yen, and Aussie are trailing, while Dollar, Euro, and Sterling are showing mixed performance.

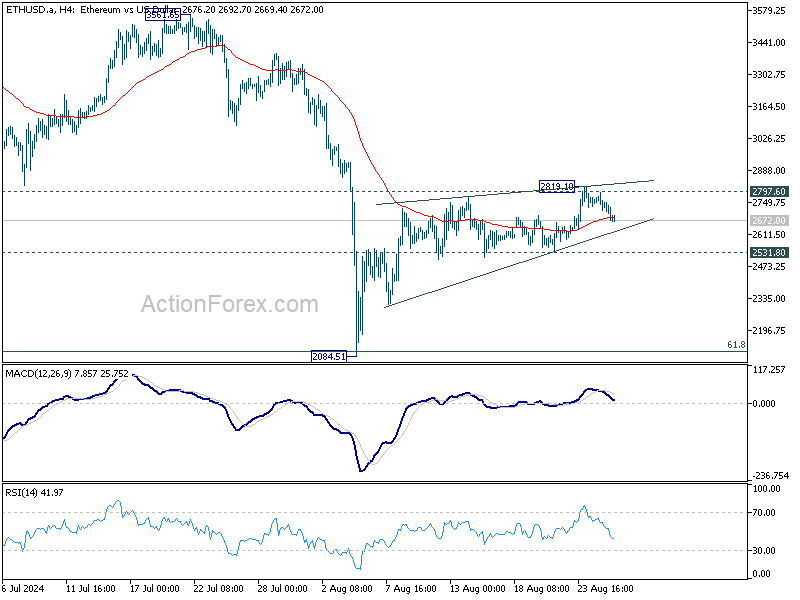

Technically, Ethereum’s rebound from 2084.51 is failing strong resistance from 2797.60 support turned resistance and 2800 psychological level. Break of 2531.80 support should confirm rejection by this 2800 resistance zone, and argue that the rebound has already completed. In this case, deeper decline would be seen back to retest 2084.51 low.

In Asia, at the time of writing, Nikkei is down -0.14%. Hong Kong HSI is down -0.21%. China Shanghai SSE is down -0.24%. Singapore Strait Times is down -0.36%. Japan 10-year JGB yield is up 0.0055 at 0.890. Overnight, DOW rose 0.16%. S&P 500 fell -0.32%. NASDAQ fell -0.85%. 10-year yield rose 0.011 to 3.818.

Fed’s Daly sees regular, normal cadence as path for rate cuts

San Francisco Fed President Mary Daly said in a Bloomberg TV interview that “the time is upon us” to cut interest rates, strongly suggesting that a rate reduction in September is highly likely.

Daly expressed concerns about maintaining “highly restrictive into a slowing economy”, and stated that it is “hard to imagine” not easing rates soon.

Daly outlined her most probable outlook, which involves inflation gradually slowing and the labor market continuing to add jobs at a “steady, sustainable” pace. If this scenario holds, she noted, adjusting policy at a “regular, normal cadence” would be reasonable.

However, Daly also indicated that if the labor market shows any signs of deterioration or weakness, “being more aggressive” in policy adjustments would be appropriate to avoid further economic strain.

DOW hits new record, but Nvidia’s earnings could be the decider

DOW managed to break into new intraday record overnight before pulling back slightly, but it was enough to secure a fresh record close. The excitement around the index’s performance is palpable, yet the overall market sentiment might hinge on Nvidia’s upcoming earnings report on Wednesday. Investors are keen to see the second-quarter results to assess the ongoing strength of the AI trade, which has been a significant driver of market gains.

Technically, doubts persist regarding the Dow’s ability to sustain its record-breaking momentum. Firm break below 40584.47 support would indicate that a short term top was formed, and set up deeper pull back to 55 D EMA (now at 39893.83), or around 40k psychological level, before DOW decides on its next move.

Looking ahead

Germany Gfk consumer sentiment and Q2 GDP final will be released in European session. Later in the day, US will release house price index and consumer confidence.

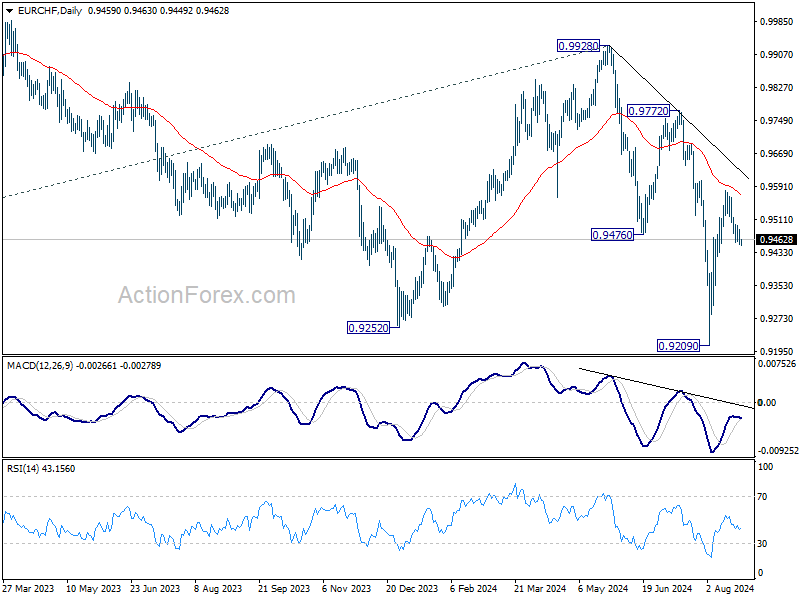

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9467; (R1) 0.9482; More….

Intraday bias in EUR/CHF stays neutral and outlook is unchanged. On the upside, sustained break of 55 D EMA (now at 0.9569) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 2.80% | 2.90% | 3.00% | 3.10% |

| 06:00 | EUR | Germany GDP Q/Q Q2 F | -0.10% | -0.10% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jun | 7.10% | 6.80% | ||

| 13:00 | USD | Housing Price Index M/M Jun | 0.20% | 0.00% | ||

| 14:00 | USD | Consumer Confidence Aug | 100.2 | 100.3 |