Trading in the forex markets remains muted as investors hold their positions ahead of Fed Chair Jerome Powell’s highly anticipated speech at Jackson Hole. Market participants are keenly focused on any signals regarding the Fed’s plans for monetary policy easing, beyond the expected rate cut in September.

Currently, Fed fund futures indicate a 26.5% probability of a 50bps cut in September, with a 73.5% likelihood of a more modest 25bps reduction. By the end of the year, there is a 65% chance that the federal funds rate will be reduced by a total of 100 basis points, bringing it to a range of 4.25-4.50%. Powell’s speech could cause significant market movements depending on whether he affirms or challenges these expectations.

The next move in the currency markets will likely be influenced by shifts in risk sentiment. NASDAQ has been clearly losing upside momentum as seen in H MACD. Firm break of 55 H EMA (now at 17615.51) should confirm short term topping at 18017.68. Deeper fall should be seen to 38.2% retracement of 15708.53 to 18017.68 at 17135.59 in rather quick manner, even as a corrective move. If realized, that would give Dollar a near term boost, in particular against commodity currencies.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.54%. CAC is up 0.39%. UK 10-year yield is down -0.010 at 3.952. Germany 10-year yield is down -0.0061 at 2.243. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI fell -0.16%. China Shanghai SSE rose 0.20%. Singapore Strait Times rose 0.43. Japan 10-year JGB yield rose 0.0161 to 0.896.

Canada’s retail sales falls -0.3% mom in Jun, to bounce back 0.6% mom in Jul

Canada’s retail sales value fell -0.3% mom to CAD 65.7B in June, matched expectations. Sales were down in four of nine subsectors and were led by decreases at motor vehicle and parts dealers. In volume terms, retail sales increased 0.1% mom.

Excluding gasoline stations and fuel vendors and motor vehicle and parts dealers, sales value were up 0.4% mom.

Retail sales volume were down 0.5% in the second quarter. In volume terms, quarterly sales declined -0.3%.

Advance estimate suggests that retail sales value rose 0.6% mom in July.

BoJ’s Ueda ready to scale back easing despite market instability

In a special parliamentary session today, BoJ Governor Kazuo Ueda reiterated the central bank’s stance to its current monetary policy, even amidst recent market volatility. He emphasized that there is “no change to our basic stance to adjust the degree of monetary easing” should economic and price trends align with its forecasts.

Addressing concerns over the market turbulence observed in early August, Ueda attributed the instability to rising fears of a US recession, driven by weaker-than-expected economic data. He also noted that BoJ’s interest rate hike in July had triggered a sharp reversal in the “one-sided Yen falls”.

He stressed that BoJ would continue to monitor market movements closely, recognizing their potential impact on the central bank’s growth and price forecasts.

“Markets at home and abroad remain unstable, so we will be highly vigilant to market developments for the time being,” Ueda remarked.

Japan’s CPI core ticks up to 2.7% in Jul, but core-core falls to 1.9%

Japan’s CPI Core, which excludes food, rose slightly from 2.6% yoy to 2.7% yoy in July, aligning with expectations and marking the 28th consecutive month that core inflation has been at or above the BoJ 2% target.

However, CPI core-core, which excludes both food and energy, fell from 2.2% yoy to 1.9% yoy, dipping below the critical 2% threshold for the first time since September 2022.

Headline CPI remained steady at 2.8% yoy. Notably, electricity prices surged by 22% following the suspension of utility subsidies, which contributed to the overall inflation rate. In contrast, services inflation softened, dropping from 1.7% yoy to 1.4% yoy.

The uptick in core CPI largely reflects the phase-out of government subsidies aimed at reducing household utility costs. Excluding this factor, the broader inflation trend appears to be on a slowing path.

New Zealand retail sales volume falls -1.2% qoq in Q2

New Zealand’s retail sales volume fell -1.2% qoq in Q2, , well below the expected -0.1% drop. Retail sales value also decreased by -1.3% qoq. Notably, 11 out of 15 retail industries reported lower sales volumes compared to the previous quarter.

Total volume of retail sales per person fell by -1.5%, marking the tenth consecutive quarter of decline after adjustments for seasonal effects and price inflation.

Ricky Ho, Business Financial Statistics Manager, highlighted the severity of this trend, noting, “Retail sale volumes per person have been falling for the last two-and-a-half years. The last time we saw several quarters of consistent falls was between 2007 and 2009, which coincided with the global financial crisis.”

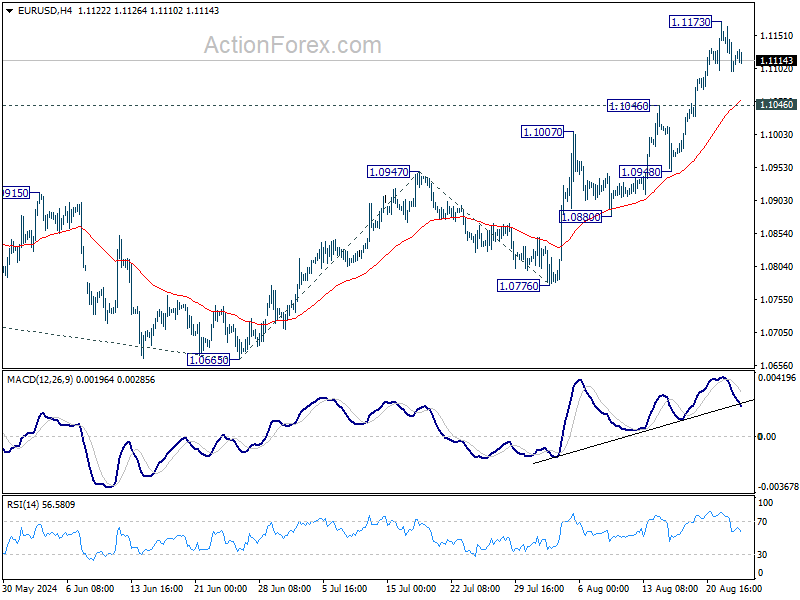

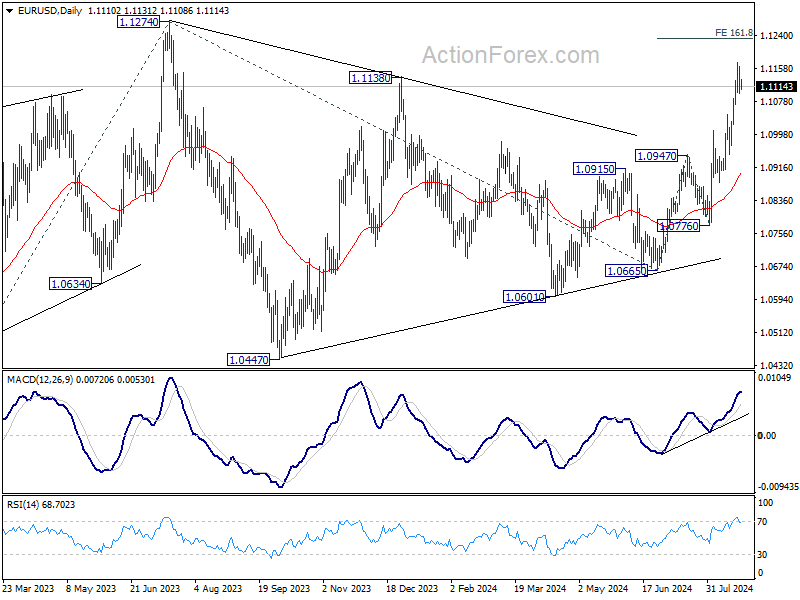

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1085; (P) 1.1125; (R1) 1.1152; More….

EUR/USD is staying in consolidation below 1.1173 and intraday bias remains neutral for the moment. Further rally is expected as long as 1.1046 resistance turned support holds. Above 1.1173 will target 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232. However, break of 1.1046 will indicate short term topping and bring deeper pullback towards 1.0947.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that’s could still extend. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). Next target is 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. However, break of 1.0974 resistance turned support will extend the correction with another falling leg back towards 1.0447 support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -1.20% | -1.00% | 0.50% | 0.40% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -1.00% | -0.80% | 0.40% | 0.30% |

| 23:01 | GBP | GfK Consumer Confidence Aug | -13 | -11 | -13 | |

| 23:30 | JPY | National CPI Y/Y Jul | 2.80% | 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jul | 2.70% | 2.70% | 2.60% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jul | 1.90% | 2.20% | ||

| 12:30 | CAD | Retail Sales M/M Jun | -0.30% | -0.30% | -0.80% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | 0.30% | -0.40% | -1.30% | |

| 14:00 | USD | New Home Sales Jul | 630K | 617K |

#shorts #crypto #forex #trading #patterns

#shorts #crypto #forex #trading #patterns