Yen, Swiss Franc, and to a lesser extent, Dollar are trailing at the bottom of the weekly currency performance chart. Strong risk-on sentiment has swept through the US markets, and the positive momentum continued in Asia. This shift in sentiment was ignited by better-than-expected US retail sales data overnight, which has significantly reduced fears of a US recession, lowering the likelihood that Fed will feel compelled to deliver an aggressive rate cut at its upcoming September meeting.

In contrast, British Pound has emerged as the strongest performer of the week. Recent economic data has reinforced BoE’s cautious stance, suggesting that a rate cut at the next meeting is far from certain. Australian Dollar is following closely behind, supported by RBA’s consistent messaging that a near-term rate cut is premature. Euro also shows strength, ranking as the third strongest currency this week, while Canadian Dollar and New Zealand Dollar hold the middle ground.

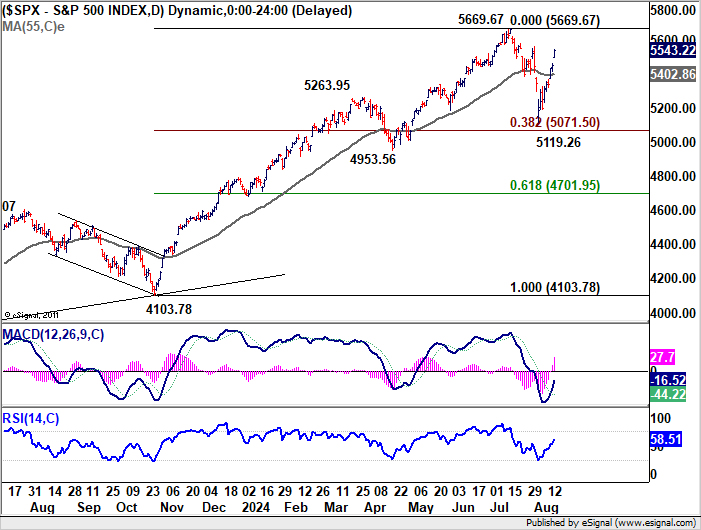

Technically, S&P 500’s strong rally this week confirms that pull back from 5669.67 has completed at 5119.26 already. But beware that there might be strong resistance from 5669.67 ahead to limit upside. Consolidation from there could still extend with one more down leg, and through 55 D EMA. But in this bearish case, strong support should be seen from 38.2% retracement of 41.03.78 to 5669.67 at 5071.50 to contain downside to complete the corrective pattern.

In Asia, at the time of writing, Nikkei is up 3.00%. Hong Kong HSI is up 1.77%. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 1.07%. Japan 10-year JGB yield is up 0.0482 at 0.886. Overnight, DOW rose 1.39%. S&P 500 rose 1.61%. NASDAQ rose 2.34%. 10-year yield rose 0.0106 to 3.926.

RBA’s Bullock dismisses near-term rate cut expectations

In her remarks to the House of Representatives’ economics committee, RBA Governor Michele Bullock emphasized the careful balancing act in managing inflation while minimizing harm to the labor market. Bullock reiterated that the Board believes current monetary policy is “sufficiently restrictive” to bring inflation down over a reasonable timeframe without causing undue damage to employment.

Despite financial markets anticipating a rate cut by the end of the year, Bullock was clear in her message that it is “premature to be thinking about rate cuts” at this stage. She pointed out that inflation remains too high and, in underlying terms, is not expected to fall back within the target range until the end of next year.

While acknowledging that economic circumstances could change, Bullock firmly stated that, based on the current outlook, the Board “does not expect that it will be in a position to cut rates in the near term.”

RBNZ confident in inflation outlook, emphasizes measured approach to further rate cuts

In a speech today, RBNZ Governor Adrian Orr expressed a “very strong level of confidence” that forward indicators are pointing to a return to low and stable inflation, within the target range of 1% to 3%. Orr emphasized the importance of keeping inflation expectations and pricing intentions “anchored” as the central bank continues to monitor economic conditions.

Assistant Governor Karen Silk, speaking in a separate interview, noted that RBNZ is observing a continued decline in price and wage-setting behaviors. Silk mentioned that if this adjustment occurs more rapidly than anticipated, it could open the door for the central bank to consider a different, potentially faster path for rate cuts.

Earlier this week, RBNZ lowered the OCR by 25 bps to 5.25% and projected that it would fall below 4% by the end of 2025. Silk reiterated that RBNZ is taking a “measured approach” to policy loosening and remains committed to a data-dependent strategy.

New Zealand BNZ manufacturing rises to 44, 17th month of contraction

New Zealand’s manufacturing sector showed a slight improvement in July, with the BusinessNZ Performance of Manufacturing Index rising from 41.2 to 44.0. Despite this rebound, the sector remains deeply entrenched in contraction, marking its 17th consecutive month below the expansion threshold. The current level is still significantly below the long-term average of 52.6.

Breaking down the data, production saw an uptick, increasing from 35.7 to 43.4, while new orders also rose, moving from 39.0 to 42.5. However, employment in the sector continued to decline, slipping from 44.0 to 43.1. Finished stocks decreased from 47.7 to 46.5, and deliveries fell slightly from 44.8 to 44.3.

Despite the relative improvement in activity, the proportion of negative comments from respondents remained high, though it eased slightly to 71.1% in July from 76.3% in June. Businesses cited ongoing issues such as a lack of orders, customers, and sales, which have been persistent concerns in recent months.

BNZ’s Senior Economist Doug Steel commented that “manufacturing activity will turn when the broader economy turns.” He added that easing monetary conditions, including a lower OCR, could help stimulate a general pick-up in sales, but emphasized that this recovery would take time.

Looking ahead

UK retail sales and Eurozone trade balance are the main features in European session. Later in the day, Canada will release manufacturing sales. US will publish building permits and housing starts, and U of Michigan consumer sentiment.

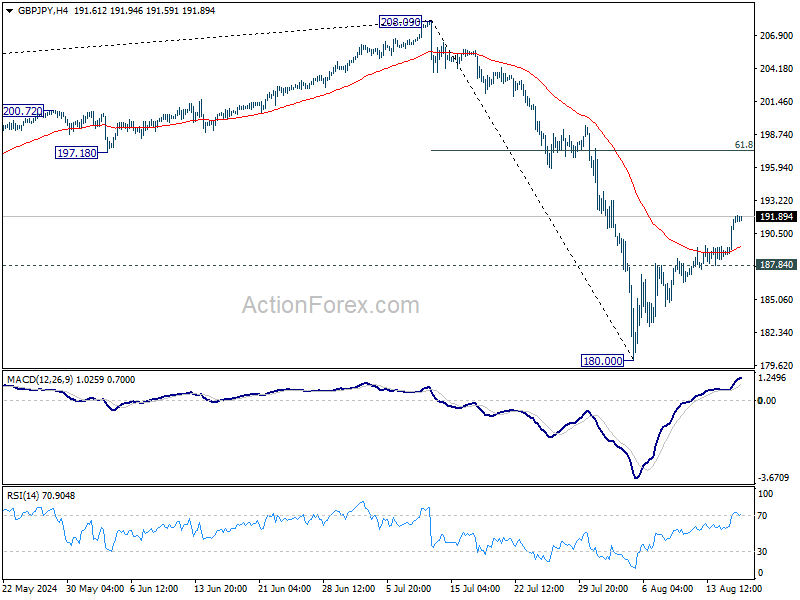

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.77; (P) 190.89; (R1) 193.02; More…

Intraday bias in GBP/JPY remains on the upside at this point. Fall from 208.09 should have completed at 180.00 already. Rebound from there is seen as the second leg of the corrective pattern from 208.09. Further rally should be seen to 61.8% retracement of 208.09 to 180.00 at 197.35, and possibly above. On the downside, however, break of 187.84 minor support will turn bias back to the downside for retesting 180.00 instead.

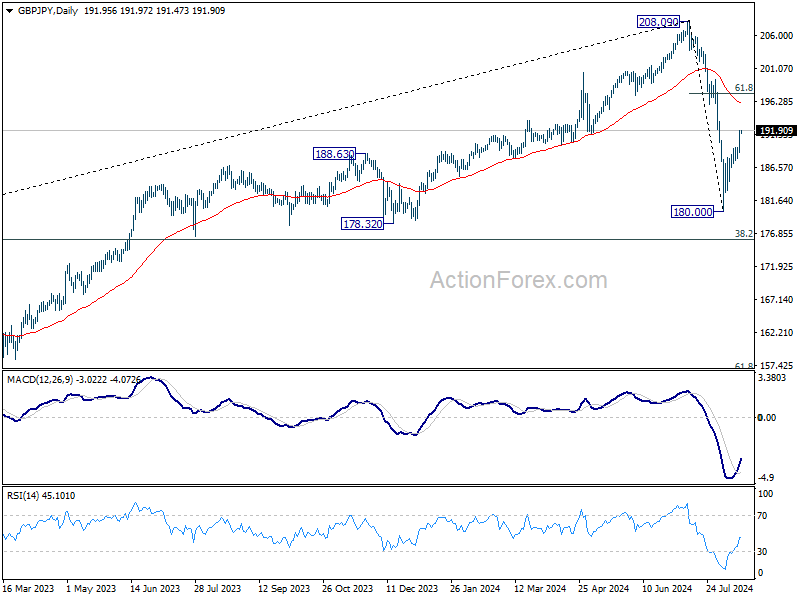

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 44 | 41.1 | 41.2 | |

| 22:45 | NZD | PPI Input Q/Q Q2 | 1.40% | 0.50% | 0.70% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 1.10% | 0.60% | 0.90% | 0.80% |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -1.30% | 0.30% | -0.40% | 0.60% |

| 06:00 | GBP | Retail Sales M/M Jul | 0.80% | -1.20% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 14.5B | 12.3B | ||

| 12:15 | CAD | Housing Starts Jul | 245K | 242K | ||

| 12:30 | CAD | Manufacturing Sales M/M Jun | -2.50% | 0.40% | ||

| 12:30 | USD | Building Permits M/M Jul | 1.44M | 1.45M | ||

| 12:30 | USD | Housing Starts M/M Jul | 1.34M | 1.35M | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 67.3 | 66.4 |