Dollar dipped as weaker-than-expected ADP job data hit the market entering US session. However, the movement has been limited with traders bracing for FOMC rate decision. Fed is widely expected to keep its policy rate unchanged at 5.25-5.50% today. The main focus is whether Fed will signal enough “confidence” to start cutting interest rates in September, a move that markets have fully priced in. Nonetheless, there is a risk that Chair Jerome Powell might sound non-committal, emphasizing that future decisions will remain data-dependent. Recent economic data, including Q2 GDP, suggest that economic activities are just normalizing without a sharp slowdown, suggesting that Fed is not in a hurry for policy loosening.

Euro saw a slight bounce following stronger-than-expected headline and core inflation readings. The headline CPI has reaccelerated slightly, and core CPI did not slow for the third straight month. There remains one more inflation report before ECB meets on September 11-12, making it premature to conclude that ECB won’t consider another rate cut. However, today’s data complicate the decision.

Meanwhile, Yen remains the strongest performer of the day. Yen surged after BoJ raised interest rates for the second time this year, extending gains after Governor Kazuo Ueda’s press conference. Ueda emphasized that 0.50% interest rate won’t be the ceiling, as the central bank will continue to hike if the economy and prices align with its projections. He did not rule out further tightening this year, stating it would depend on incoming data, such as services inflation, inflation expectations, and overall demand and output gap. Ueda also noted that while Yen’s depreciation hasn’t altered economic forecasts, there is a “significant risk” of a weak yen leading to an overshoot of inflation.

Australian Dollar is the worst performer today following Q2 inflation data, which showed slowdown in the core measure. This data should be welcomed by RBA, reducing the pressure to hike interest rates again. Indeed, markets are now pricing in a 65% chance of a rate cut by year-end, compared to 30% chance of a hike next week before the data.

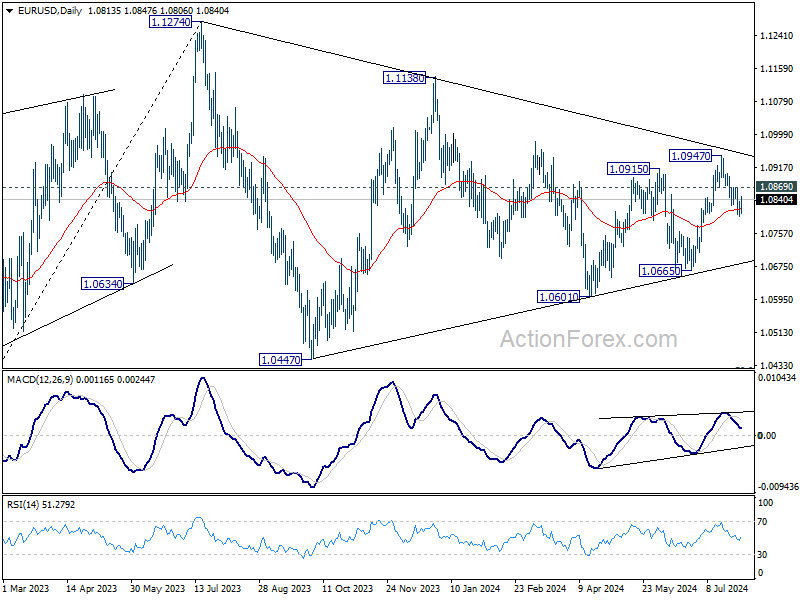

Technically, a key level to watch today for the rest of the US session is 1.0869 minor resistance in EUR/USD. Firm break there will argue that fall from 1.0947 has completed as a corrective move, after drawing support from 55 D EMA. In this case, rise from 1.0601 would be ready to resume through 1.0947 towards 1.1138 resistance. Nevertheless, rejection by 1.0869 will set the stage for deeper fall back to 1.0665 support next.

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 0.56%. CAC is up 1.09%. UK 10-year yield is down -0.052 at 3.998, below 4% handle. Germany 10-year yield is down -0.033 at 2.311. Earlier in Asia, Nikkei rose 1.49%. Hong Kong HSI rose 2.01%. China Shanghai SSE rose 2.06%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.0644 to 1.061.

Canadian GDP grows by 0.2% mom in May, exceeds expectations

Canada’s GDP grew by 0.2% mom in May, surpassing the expected 0.1% mom growth. The primary driver of this growth was the goods-producing industries, which saw a 0.4% increase with four out of five sectors expanding. The services-producing industries also contributed, albeit modestly, with a 0.1% rise. Overall, 15 out of 20 sectors experienced growth.

Advance information suggests that real GDP increased by 0.1% mom in June. Gains in construction, real estate and rental and leasing, and finance and insurance were partially offset by declines in manufacturing and wholesale trade.

US ADP employment grows only 122k, wages growth slows further

In July, US ADP private employment grew by 122k, significantly below the expected 166k. Breaking it down by sector, goods-producing jobs increased by 37k, while service-providing jobs rose by 85k. By establishment size, small companies lost -7,000k, medium-sized companies added 70k jobs, and large companies added 62k jobs.

Annual pay gains for job-stayers slowed to 4.8% yoy, the lowest rate in three years. Annual pay growth for job-changers also dropped significantly from 7.7% yoy to 5.2% yoy.

Nela Richardson, chief economist at ADP, commented, “With wage growth abating, the labor market is playing along with the Federal Reserve’s effort to slow inflation. If inflation goes back up, it won’t be because of labor.”

Eurozone CPI rises to 2.6% yoy in Jul, core CPI unchanged at 2.9% yoy

Eurozone CPI rose from 2.5% yoy to 2.6% yoy in July, above expectation of 2.4% yoy. Core CPI (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in July (4.0%, compared with 4.1% in June), followed by food, alcohol & tobacco (2.3%, compared with 2.4% in June), energy (1.3%, compared with 0.2% in June) and non-energy industrial goods (0.8%, compared with 0.7% in June).

BoJ hikes to 0.25%, signals more increases if outlook realizes

BoJ raised the uncollateralized overnight call rate from 0-0.10% to around 0.25% today. The decision was made by a 7-2 vote, with dissenting votes from Toyoaki Nakamura and Asahi Noguchi, who preferred to gather more information and conduct a careful assessment before adjusting the interest rate.

Regarding JGB purchases, there was a unanimous decision to reduce the amount of monthly outright purchases to about JPY 3T by Q1 2026. The amount will be cut by JPY 400B each calendar quarter.

BoJ stated that economic activity and prices have been “developing generally in line with the Bank’s outlook.” Moves to raise wages have been spreading, and the annual rate of import price growth has “turned positive again,” with upside risks to prices requiring attention.

It also noted if the outlook presented in the July Outlook Report is realized, BoJ will continue to raise the policy interest rate and adjust the degree of monetary accommodation accordingly.

In the new economic projections, the BoJ made several adjustments:

- Fiscal 2024 growth forecast was lowered from 0.8% to 0.6%.

- Fiscal 2025 growth forecast remains unchanged at 1.0%.

- Fiscal 2026 growth forecast remains unchanged at 1.0%.

For inflation projections:

- Fiscal 2024 CPI core forecast was lowered from 2.8% to 2.5%.

- Fiscal 2025 CPI core forecast was raised from 1.9% to 2.1%.

- Fiscal 2026 CPI core forecast remains unchanged at 1.9%.

- Fiscal 2024 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2025 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2026 CPI core-core forecast remains unchanged at 2.1%.

Australia’s trimmed mean CPI drops to 3.9%, continuing six-quarter downtrend

In Q2, Australia’s CPI rose by 1.0% qoq, matching both expectations and the pace set in Q1. Annual rate increased from 3.6% to 3.8% , also in line with forecasts.

More notably, the core inflation measure marked its sixth consecutive quarter of cooling. Trimmed mean CPI, which is a key indicator of underlying inflation, rose by 0.8% qoq. This represents a slowdown from the prior quarter’s 1.0% qoq increase and falls below the expected 0.9% qoq. Annually, trimmed mean CPI slowed from 4.0% yoy to 3.9% yoy, below the expected 4.0% and continuing its downward trend from the peak of 6.8% in the December 2022 quarter.

Additionally, the monthly CPI for June slowed from 4.0% yoy to 3.8% yoy, again matching expectations.

NZ ANZ business confidence jumps to 27.1, inflation expectations fall further

In July, New Zealand’s ANZ Business Confidence saw a notable increase, jumping from 6.1 to 27.1. Own Activity Outlook also improved, rising from 12.2 to 16.3. Meanwhile, cost expectations fell slightly from 69.2 to 68.2, and wage expectations edged up from 73.5 to 74.6. Pricing intentions saw an increase from 35.3 to 37.6. Importantly, inflation expectations continued their steady decline, falling from 3.46% to 3.20%.

ANZ commented that the economic climate remains one where “bad news is good news” for RBNZ. With mounting evidence that monetary policy has been effective, perhaps overly so, there is now a broad expectation that RBNZ will start easing the Official Cash Rate this year.

ANZ noted that “evidence is mounting that the inflation dragon is on its last legs,” which positions the New Zealand economy for a more robust recovery compared to a scenario where inflation control efforts were only partially successful.

China’s NBS PMI manufacturing falls to 49.4 in amid weak demand and extreme weather

China’s official NBS PMI Manufacturing index fell slightly from 49.5 to 49.4 in July, just above the expected 49.3. This index has remained below the 50-mark, which separates growth from contraction, for all but three months since April 2023.

NBS analyst Zhao Qinghe attributed the decline in manufacturing activity to the typical off-season for production in July, insufficient market demand, and extreme weather conditions such as high temperatures and floods in some areas.

PMI Non-Manufacturing index also fell, dropping from 50.5 to 50.2, in line with expectations, but still indicating expansion for the 19th consecutive month. Within this category, construction subindex decreased from 52.3 to 51.2, while services subindex slipped from 50.2 to 50e.

Overall, the official PMI Composite, which combines both manufacturing and non-manufacturing sectors, declined from 50.5 to 50.2.

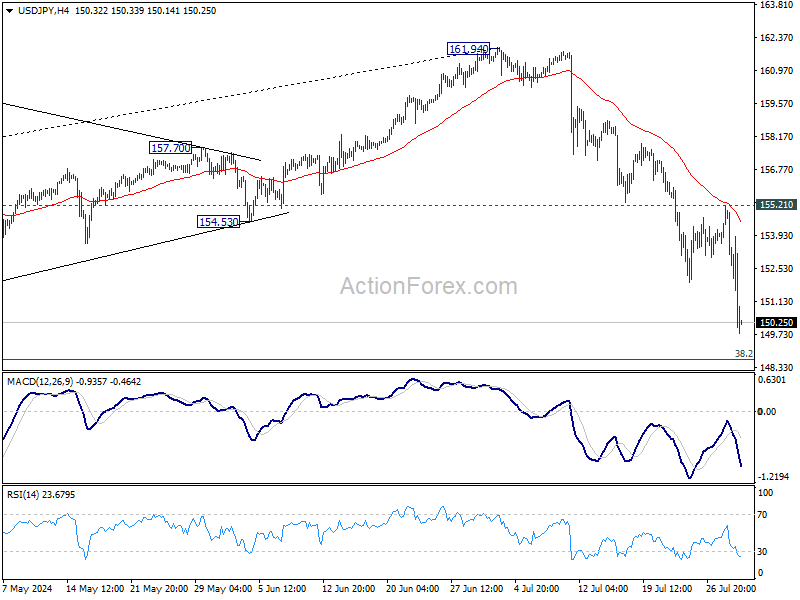

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.86; (P) 153.54; (R1) 154.43; More…

USD/JPY’s fall from 161.94 accelerates lower again to as low as 149.77 so far. Intraday bias stays on the downside for 148.66 fibonacci level, which is close to medium term channel support (now at 148.22). Strong support could be seen there to bring rebound. But break of 155.21 resistance is needed to confirm short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Next target is 38.2% retracement of 127.20 to 161.94 at 148.66. Decisive break there will pave the way to 140.25 support next. Risk will now stay on the downside as long as 55 D EMA (now at 156.90) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -13.80% | -1.70% | -1.90% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -3.60% | -4.20% | 3.60% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | 3.70% | 3.30% | 2.80% | |

| 01:00 | NZD | ANZ Business Confidence Jul | 27.1 | 6.1 | ||

| 01:30 | AUD | Monthly CPI Y/Y Jun | 3.80% | 3.80% | 4.00% | |

| 01:30 | AUD | CPI Q/Q Q2 | 1.00% | 1.00% | 1.00% | |

| 01:30 | AUD | CPI Y/Y Q2 | 3.80% | 3.80% | 3.60% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 0.80% | 0.90% | 1.00% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 3.90% | 4.00% | 4.00% | |

| 01:30 | AUD | Retail Sales M/M Jun | 0.50% | 0.30% | 0.60% | |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.60% | 0.40% | ||

| 01:30 | CNY | NBS Manufacturing PMI Jul | 49.4 | 49.3 | 49.5 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | 50.2 | 50.2 | 50.5 | |

| 03:57 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -6.70% | -2.00% | -5.30% | |

| 05:00 | JPY | Consumer Confidence Jul | 36.7 | 36.5 | 36.4 | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | 0.40% | 0.10% | 0.00% | |

| 07:55 | EUR | Germany Unemployment Change Jul | 18K | 16K | 19K | |

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.00% | 6.00% | 6.00% | |

| 08:00 | CHF | UBS Economic Expectations Jul | 9.4 | 17.5 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 2.60% | 2.40% | 2.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 2.90% | 2.80% | 2.90% | |

| 12:15 | USD | ADP Employment Change Jul | 122K | 166K | 150K | 155K |

| 12:30 | USD | Employment Cost Index Q2 | 0.90% | 1.00% | 1.20% | |

| 12:30 | CAD | GDP M/M May | 0.20% | 0.10% | 0.30% | |

| 13:45 | USD | Chicago PMI Jul | 44.1 | 47.4 | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 1.60% | -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.6M | -3.7M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |