Dollar rebounded broadly overnight following steep 500+ point selloff in DOW. Some analysts cited rotation away from big tech as the cause, but the decline was broad-based. Profit-taking could be a more likely factor after recent record runs, as traders and Fed policymakers await more data to determine the number of rate cuts needed this year.

Yen is struggling to extend near-term gains after slightly lower-than-expected core CPI data. Although inflation has accelerated, it is not strong enough to warrant a rate hike by BoJ later this month. The government’s new forecasts suggest that Yen will average around 158.8 against Dollar. This argues that USD/JPY could be allowed to fluctuate around 159 without triggering intervention from Japanese authorities.

For the week, Swiss Franc remains the strongest performer, followed by Yen and then Dollar. New Zealand Dollar is staying as the weakest, followed by Australian Dollar and then Canadian Dollar. Euro and the pound continue to struggle in the middle.

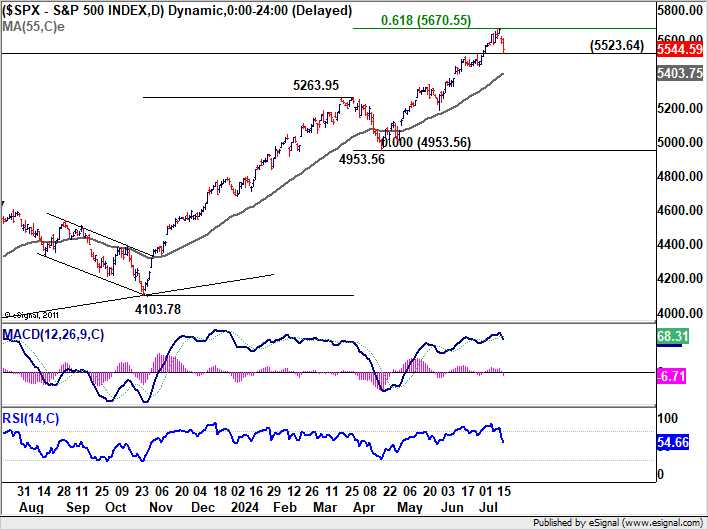

Technically, S&P 500 is now pressing 5523.64 support with the steep decline in the past two days. Firm break there would confirm short term topping after just missing 61.8% projection of 4103.78 to 5263.95 from 4953.56 at 5670.55. Deeper pullback could then be seen back to 55 D EMA now at 5403.75. IN this bearish case, risk aversion could provide Dollar with some support.

In Asia, at the time of writing, Nikkei is down -0.22%. Hong Kong HSI is up 0.22%. China Shanghai SSE is down -0.08%. Singapore Strait Times is down -0.81%. Japan 10-year JGB yield is up 0.0102 at 1.042. Overnight, DOW fell sharply by -1.29%. S&P 500 fell -0.78%. NASDAQ fell -0.70%. 10-year yield rose 0.043 to 4.189.

Japan’s CPI core rises to 2.6%, above target for 27th month

Japan’s core CPI, which excludes food prices, rose from 2.5% yoy to 2.6% yoy in June, slightly missing expectations of 2.7% yoy. This nonetheless marks the 27th consecutive month that inflation has been at or above BoJ’s 2% target. Core-core CPI, which excludes both food and energy, increased from 2.1% yoy to 2.2% yoy, while headline CPI as unchanged at 2.8% yoy.

Services inflation saw a modest increase from 1.6% yoy to 1.7% yoy. A reduction in government subsidies aimed at curbing utility bills resulted in a 7.7% yoy rise in energy costs, up from 7.2% increase seen in May.

Attention is now shifting to BoJ’s upcoming meeting on July 30-31. There is divided opinion on whether BoJ will decide to hike the policy rate from the current 0.00-0.10% range to 0.15-0.25%. The central bank is also expected to unveil a roadmap for reducing its bond purchases and release its economic outlook report, which will publish new economic forecasts.

Japan downgrades fiscal 2024 growth forecast amid consumption struggles

Japan’s government has downgraded its growth forecast for the current fiscal year 2024 from 1.3% to 0.9%.

This adjustment comes as inflation continues to impact private consumption, which accounts for over half of the economy. Private consumption growth is now expected to be just 0.5%, a significant drop from the January forecast of 1.2%.

Various one-off factors, including safety test scandals in the auto industry, have also contributed to this downgrade.

However, the economy is expected to rebound in fiscal 2025 with a growth rate of 1.2%.

Consumer prices are now forecast to rise by 2.8% in fiscal 2024, an increase from the earlier expectation of 2.5%.

The government has also adjusted its assumption for Yen, now expecting it to remain around 158.8 per Dollar for the current fiscal year, weaker than the previous estimate of 149.8 Yen.

Fed’s Daly advocates for patience as “we’re not there yet”

San Francisco Fed President Mary Daly commented at an event overnight, emphasizing that the US has not yet achieved price stability. While acknowledging recent positive inflation data, Daly noted, “We’re not there yet.”

Daly highlighted the delicate balancing act facing monetary policy. She called for patience, urging policymakers to “balance the costs of acting fast and being wrong.”

“It’s a risk to act too soon to normalize interest rates and then have inflation stuck below or above our target, and it’s a risk to hold on too long and make the labor market falter,” Daly elaborated.

Looking ahead

UK retail sales and publis sector net borrowing, an Eurozone current account will be released in European session. Later in the day, Canada will publish retail sales, IPPI and RMPI.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3678; (P) 1.3698; (R1) 1.3727; More…

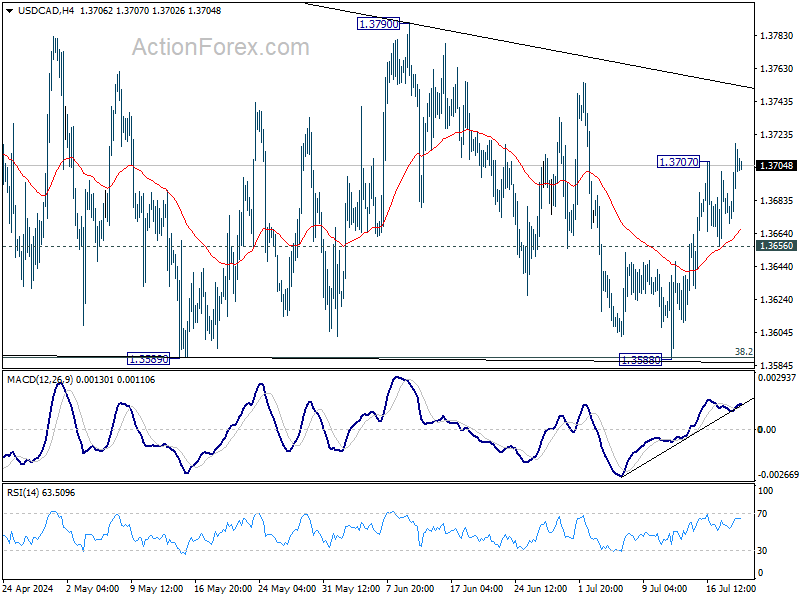

USD/CAD’s rebound from 1.3588 resumed by breaking 1.3707 temporary top and intraday bias back on the upside. Outlook is unchanged that corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Further rise is expected to 1.3790 resistance first. Break there will larger rise from 1.3716 is ready to resume through 1.3845.

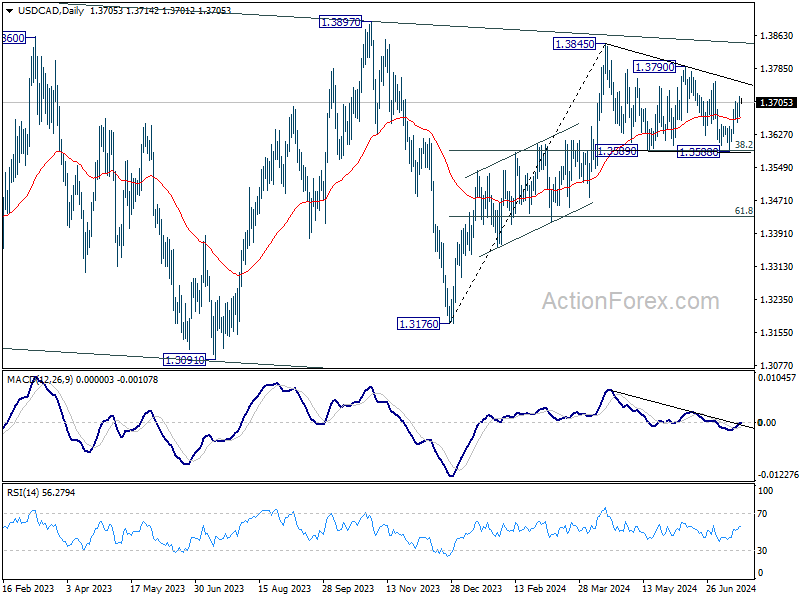

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Jul | -13 | -11 | -14 | |

| 23:30 | JPY | National CPI Y/Y Jun | 2.80% | 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.60% | 2.70% | 2.50% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 2.20% | 2.10% | ||

| 06:00 | GBP | Retail Sales M/M Jun | -0.60% | 2.90% | ||

| 06:00 | EUR | Germany PPI M/M Jun | 0.10% | 0.00% | ||

| 06:00 | EUR | Germany PPI Y/Y Jun | -1.60% | -2.20% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 12.0B | 14.1B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) May | 34.6B | 38.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.20% | 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Jun | -0.70% | -1.00% | ||

| 12:30 | CAD | Retail Sales M/M May | -0.20% | 0.70% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.20% | 1.80% |