Risk aversion continues to support Dollar in relatively quiet trading today. Both Sterling and Canadian Dollar weakened mildly after worse-than-expected retail sales data. Euro shrugged off dovish comments from some ECB officials. Meanwhile, Yen softened slightly following lower-than-expected CPI core reading.

However, overall movements in the currency markets remain limited as traders hold their bets, awaiting further developments to determine if yesterday’s steep selloff in US stocks will continue or if risk sentiment will improve as the week comes to a close.

For the week, Swiss Franc remains the strongest, followed by Yen and then Dollar. The greenback, however, has the potential to overtake both of their positions. Kiwi remains the worst performer, followed by Aussie and Loonie, which is typical in risk-off markets. Euro and Sterling are stuck in the middle, with the common currency having a slight upper hand.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.54%. CAC is down -0.44%. UK 10-year yield is up 0.0467 at 3.252. Germany 10-year yield is up 0.0463 at 2.473. Earlier in Asia, Nikkei fell -0.16%. Hong Kong HSI fell -2.03%. China Shanghai SSE rose 0.17%. Singapore Strait Times fell -0.68%. Japan 10-year JGB yield closed flat at 1.047.

Canada retail sales falls -0.8% mom in May, down further -0.3% mom in Jun

Canada’s retail sales fell -0.8% mom to CAD 66.1B in May, worse than expectation of -0.5% mom. Sales were down in eight of nine subsectors, led by decreases at food and beverage retailers. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -1.4% mom in May.

Advance estimate indicates that sales decreased further by -0.3% mom in June.

ECB’s Villeroy: Market rate cut expectations “rather reasonable”

ECB Governing Council member Francois Villeroy de Galhau spoke on French radio BFM Business today, expressing that current market expectations for interest rate cuts seem “rather reasonable.”

Markets are currently pricing in nearly two ECB rate cuts for the remainder of the year, likely occurring in September and December, with around five cuts anticipated by the end of next year.

Villeroy de Galhau affirmed ECB’s stance on inflation, stating, “Overall, we are ‘on track’ with our inflation target and forecast of 2% next year.” He further emphasized the commitment to this target, noting, “Barring any shocks, this is more than a forecast, it’s a commitment.”

ECB’s Simkus: Interest rates are getting lower, quite significantly

ECB Governing Council member Gediminas Simkus shared his views with reporters today, indicating that his outlook aligns with current market expectations, which anticipate two rate cuts this year.

Simkus commented, “Interest rates are getting lower and, I think, will keep getting lower, and quite significantly.”

UK retail sales falls -1.2% mom in Jun, down -0.2% yoy in Q2

UK retail sales volume fell -1.2% mom in June, worse than expectation of -0.6% mom. Sales volumes fell across most sectors, with department stores and clothing retailers broadly returning to their Q1 levels. It’s -1.3% below their pre-pandemic levels in February 2020.

Looking at the quarter, sales volumes fell by -0.1% qoq and -0.2% yoy in Q2.

Japan’s CPI core rises to 2.6%, above target for 27th month

Japan’s core CPI, which excludes food prices, rose from 2.5% yoy to 2.6% yoy in June, slightly missing expectations of 2.7% yoy. This nonetheless marks the 27th consecutive month that inflation has been at or above BoJ’s 2% target. Core-core CPI, which excludes both food and energy, increased from 2.1% yoy to 2.2% yoy, while headline CPI as unchanged at 2.8% yoy.

Services inflation saw a modest increase from 1.6% yoy to 1.7% yoy. A reduction in government subsidies aimed at curbing utility bills resulted in a 7.7% yoy rise in energy costs, up from 7.2% increase seen in May.

Attention is now shifting to BoJ’s upcoming meeting on July 30-31. There is divided opinion on whether BoJ will decide to hike the policy rate from the current 0.00-0.10% range to 0.15-0.25%. The central bank is also expected to unveil a roadmap for reducing its bond purchases and release its economic outlook report, which will publish new economic forecasts.

Japan downgrades fiscal 2024 growth forecast amid consumption struggles

Japan’s government has downgraded its growth forecast for the current fiscal year 2024 from 1.3% to 0.9%.

This adjustment comes as inflation continues to impact private consumption, which accounts for over half of the economy. Private consumption growth is now expected to be just 0.5%, a significant drop from the January forecast of 1.2%.

Various one-off factors, including safety test scandals in the auto industry, have also contributed to this downgrade.

However, the economy is expected to rebound in fiscal 2025 with a growth rate of 1.2%.

Consumer prices are now forecast to rise by 2.8% in fiscal 2024, an increase from the earlier expectation of 2.5%.

The government has also adjusted its assumption for Yen, now expecting it to remain around 158.8 per Dollar for the current fiscal year, weaker than the previous estimate of 149.8 Yen.

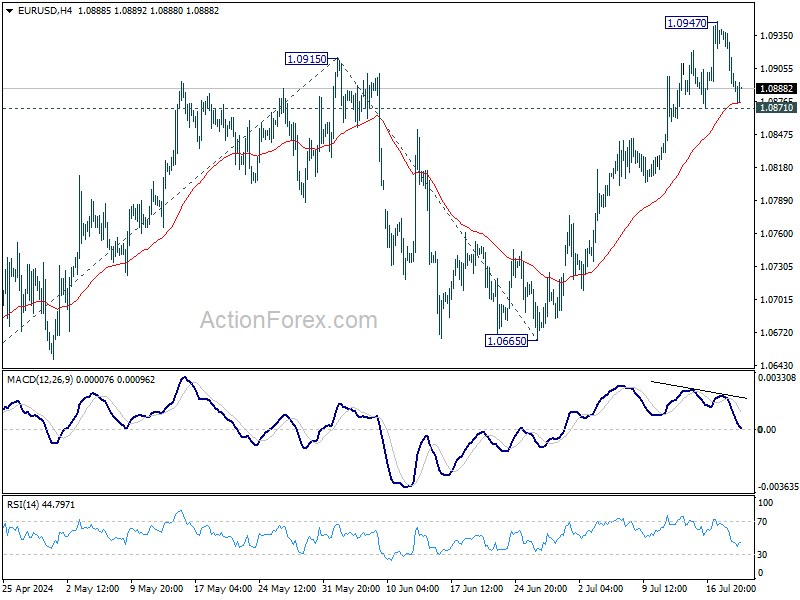

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0879; (P) 1.0911; (R1) 1.0928; More….

EUR/USD is still holding above 1.0871 support and intraday bias stays neutral. Further remains mildly in favor. Break of 1.0947 will resume the rise from 1.0601 and target target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, considering bearish divergence condition in 4H MACD, firm break of 1.0871 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 1.0804).

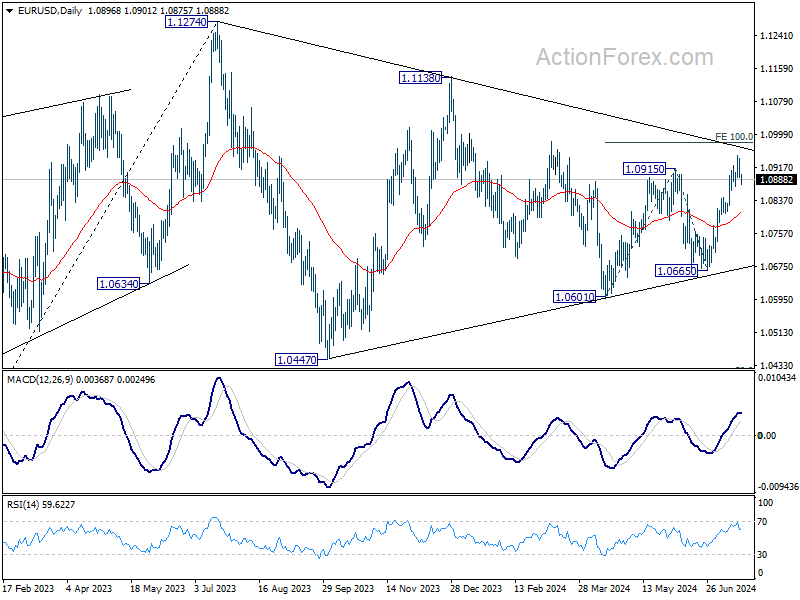

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that’s still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Jul | -13 | -11 | -14 | |

| 23:30 | JPY | National CPI Y/Y Jun | 2.80% | 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.60% | 2.70% | 2.50% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 2.20% | 2.10% | ||

| 06:00 | EUR | Germany PPI M/M Jun | 0.20% | 0.10% | 0.00% | |

| 06:00 | EUR | Germany PPI Y/Y Jun | -1.60% | -1.60% | -2.20% | |

| 06:00 | GBP | Retail Sales M/M Jun | -1.20% | -0.60% | 2.90% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 13.6B | 12.0B | 14.1B | 15.6B |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 37B | 34.6B | 38.6B | |

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.00% | 0.20% | 0.00% | 0.20% |

| 12:30 | CAD | Raw Material Price Index Jun | -1.40% | -0.70% | -1.00% | -1.50% |

| 12:30 | CAD | Retail Sales M/M May | -0.80% | -0.50% | 0.70% | 0.60% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | -1.30% | -0.50% | 1.80% | 1.70% |