As US session kicks off, Dollar is trading mildly higher, with traders eagerly anticipating Fed Chair Jerome Powell’s two-day semiannual testimony before Congress. The key questions looming over the markets are whether the Fed will initiate interest rate cuts in September and if there will be a total of one or two cuts this year. Currently, fed fund futures indicate about a 75% chance of a rate cut in September and a 73% chance of two cuts within the year.

If Powell sticks to the messaging from last Friday’s Monetary Policy Report, he may acknowledge some modest progress in disinflation but could stress the need for more significant confidence before considering policy easing. He might also highlight that while labor supply has eased, it remains relatively tight, though not excessively so. That would leave market participants guessing about the Fed’s next steps.

Also, it should be emphasized that the US is set to release June CPI report on Thursday. This report could either reinforce or counteract the market moves following Powell’s testimony. As such, traders may want to consider securing profits early or at least tightening stops when trades are in their favor, given the potential for heightened volatility.

Overall, in the currency markets, Dollar is the strongest performer so far today, followed by Swiss Franc and British Pound. Conversely, Yen is the weakest, followed by Aussie and Kiwi. Euro and Loonie are positioned in the middle of the pack.

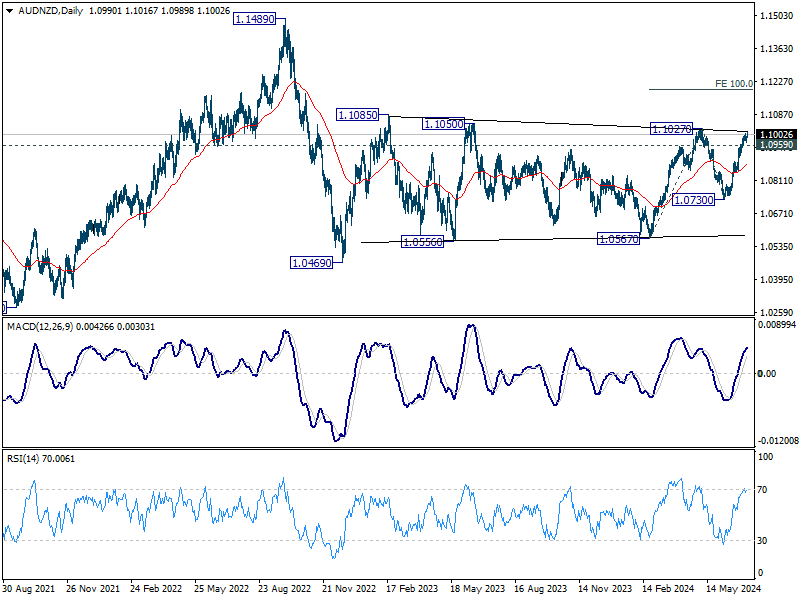

Looking ahead to Asian session, AUD/NZD pair is worth monitoring closely, as RBNZ will announce its rate decision. The OCR is expected to remain unchanged at 5.50%. The key question is whether RBNZ will hint at earlier-than-expected rate cuts, which is unlikely. Nevertheless, dovish remarks from RBNZ could boost AUD/NZD.

Technically, firm break of 1.1027 resistance in AUD/NZD would argue that whole rebound from 1.0469 is resuming through 1.1085. Next target would be 100% projection of 1.0567 to 1.1027 from 1.0730 at 1.1187. Nevertheless, break of 1.0959 will be the firm sign of rejection by 1.1027 and bring deeper pullback.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -1.03%. CAC is down -1.29%. UK 10-year yield is up 0.0403 at 4.158. Germany 10-year yield is up 0.027 at 2.569. Earlier in Asia, Nikkei surged 1.96%. Hong Kong HSI fell -0.00%. China Shanghai SSE rose 1.26%. Singapore Strait Times rose 0.64%. Japan 10-year JGB yield fell -0.0152 to 1.076.

ECB’s Panetta backs gradual rate cuts amid stabilizing inflation

ECB Governing Council member Fabio Panetta indicated today the “reduction of official rates could proceed gradually”, in line with the return of inflation towards the ECB’s target. Speaking to bankers in Rome, Panetta emphasized that as long as macroeconomic trends remain consistent with ECB’s expectations, this gradual approach will be maintained.

Panetta downplayed concerns over persistently high service sector prices, explaining that it is typical for service prices to decline more slowly compared to goods prices. He also noted that wage growth is expected to moderate in the near future.

“Past interest rate hikes are still dampening demand, output, and inflation and will continue to do so in the months to come,” Panetta remarked.

Australia Westpac consumer sentiment falls -1.1% mom, intensifying interest rate concerns

Australia’s Westpac Consumer Sentiment index dropped by -1.1% mom to 82.7 in July, reflecting increased concerns about persistent inflation and fears of interest rate hikes.

The Mortgage Rate Expectations Index, which measures consumer expectations for variable mortgage rates over the next 12 months, surged by 12.8% in July, marking the steepest monthly rise since early 2022. Over the past three months, the index has climbed by 30%, from a below-average 122.8 in April to 159.2 in July, well above historical average of 143.8. This marked increase is the sharpest observed in the past seven years, with detailed responses indicating that nearly 60% of consumers expect mortgage rates to rise over the next year.

RBA will meet on August 5–6. Westpac expects the RBA to hold interest rates steady, contingent on inflation continuing to decline as anticipated. The upcoming Q2 CPI and labor market data will be critical.

Australia’s NAB business confidence rebounds to 4, highest since early 2023

Australia’s NAB Business Confidence rose from -2 to 4 in June, marking its highest level since early 2023 and returning to positive territory. However, Business Conditions fell from 6 to 4, indicating some ongoing challenges. Trading conditions decreased slightly from 11 to 10, profitability conditions dropped from 3 to 2, and employment conditions fell sharply from 5 to 0.

Labor cost growth slowed to 1.8% on a quarterly basis, down from 2.3% in May, while purchase cost growth eased to 1.3% from 1.7%. Overall product price growth decreased to 0.7%, down from 1.1%. Retail price growth, however, held steady at 1.5%, and recreation and personal services prices declined to 0.7% from 1.1%.

Gareth Spence, NAB Head of Australian Economics, noted, the survey signals “another soft quarter” in Q2. Capacity utilisation remains “high with demand and supply yet to fully normalise”.

“Price pressures continue to ease in a trend sense though the data certainly remains bumpy,” Spence added.

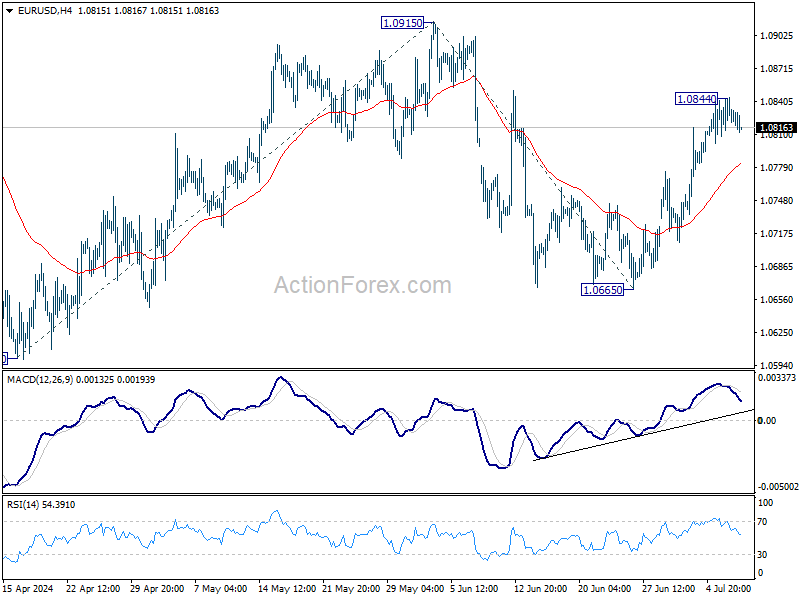

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0824; (R1) 1.0845; More….

Intraday bias in EUR/USD remains neutral for consolidations below 1.0844 temporary top. Further rally is in favor as long as 55 4H EMA (now at 1.0783) holds. On the upside, above 1.0844 will resume the rebound from 1.0665 to retest 1.0915 resistance. Firm break there will target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. However, sustained break of 55 4H EMA will bring deeper fall back to 1.0665 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that’s still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | 1.50% | 2.00% | 1.90% | |

| 00:30 | AUD | Westpac Consumer Confidence Jul | 1.50% | 1.70% | ||

| 01:30 | AUD | NAB Business Conditions Jun | 4 | 6 | ||

| 01:30 | AUD | NAB Business Confidence Jun | 4 | -3 | -2 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jun P | 9.70% | 4.20% | ||

| 10:00 | USD | NFIB Business Optimism Index Jun | 91.5 | 89.5 | 90.5 |