The forex markets are pretty steady in Asian session today, with Euro stabilizing from its previous sharp sell-off. Meanwhile, Dollar and Yen are posting modest gains. In contrast, commodity currencies showed less resilience, and Swiss Franc surrendered some of its recent strong gains. British Pound demonstrated mixed performance. A noticeable characteristic of today’s market is the low activity level, with most major currency pairs and crosses stuck inside last Friday’s trading range.

This subdued activity may continue throughout the rest of Monday. However, the market is expected to become more volatile in the coming days due to several key economic events. Meetings of the RBA, SNB and BoE are scheduled, each with the potential for market-moving surprises. Additionally, BoJ and BoJ will release their meeting minutes. Economic data releases, including inflation figures, retail sales, and PMI data from major economies, will also contribute to the market dynamics.

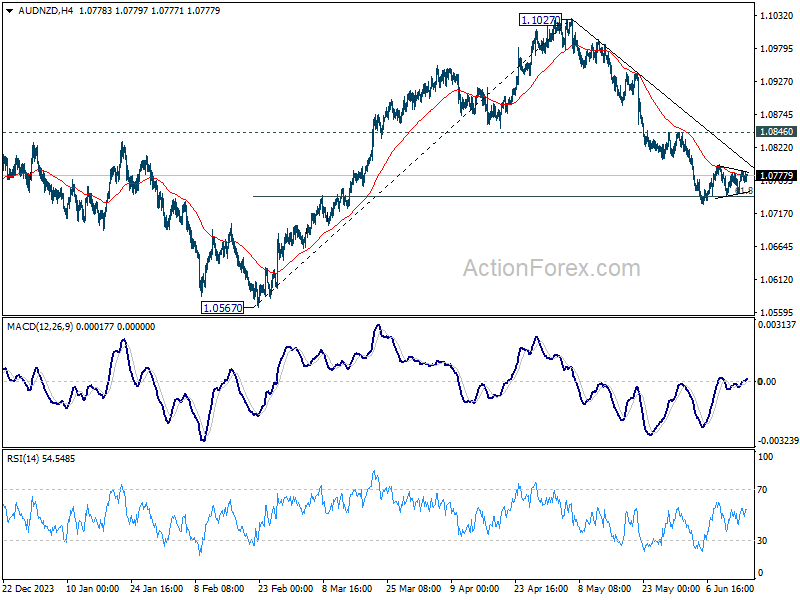

Technically, AUD/NZD continues to draw support from 61.8% retracement of 1.0567 to 1.1027 at 1.0743, but lacks momentum for sustainable rebound yet. While more hawkish than expected RBA could push AUD/NZD higher, outlook will continue to stay bearish as long as 1.0846 resistance holds. Meanwhile, in case of fall resumption on more dovish than expected RBA, sustained trading below 1.0743 will pave the way back to 1.0567 low.

In Asia, at the time of writing, Nikkei is down -2.16%. Hong Kong HSI is up 0.06%. China Shanghai SSE is down -0.55%. Singapore Strait Times is down -0.81%. Japan 10-year JGB yield is down -0.006 at 0.932.

Fed’s Kashkari points to late-year rate cut

Minneapolis Fed President Neel Kashkari indicated in a CBS interview over the weekend that any interest rate cut is likely be towards the end of the year.

Kashkari emphasized the necessity of gathering “more evidence” to ensure inflation is on a downward trend toward Fed’s target of 2%.

“We’re in a very good position right now to take our time, get more inflation data, get more data on the economy, on the labor market, before we have to make any decisions on cutting interest rates,” he added.

If a rate cut is to occur, it would likely be towards the end of the year, aligning with the median forecast.

NZ BNZ services falls to 43, unprecedented contraction

New Zealand’s BusinessNZ Performance of Services Index dropped significantly from 46.6 to 43.0 in May, marking the lowest level of activity for a non-COVID lockdown month since the survey’s inception in 2007.

BusinessNZ Chief Executive Kirk Hope described the May result as “as bad as it can get” for the sector, with contraction levels surpassing those seen during the Global Financial Crisis of 2008/09.

Examining the details, key metrics reveal a stark downturn. Activity/sales fell from 46.0 to 40.9, employment dropped from 47.0 to 46.0, new orders/business decreased from 46.6 to 42.6, stocks/inventories declined from 46.2 to 42.4, and supplier deliveries slid from 47.5 to 46.1.

The proportion of negative comments in May (65.4%) remained similar to April (66.3%), indicating persistent concerns about the economic downturn.

BNZ’s Senior Economist Doug Steel noted, “the speed of decline is as worrisome as its size over the past three months. There is weak and then there is very weak. Overall, this tells of a services sector in reverse, at pace.”

China’s industrial production up 5.6% yoy in May, misses exp 6.0% yoy

China’s industrial production increased by 5.6% yoy in May, falling short of the expected 6.0% yoy and slowing from April’s 6.7% yoy. Despite this overall slowdown, the equipment and high-tech manufacturing sectors showed robust growth, with outputs rising 7.5% yoy and 10% yoy, respectively.

Fixed asset investment grew by 4.0% year-to-date yoy, slightly below the anticipated 4.2%. Within this sector, property development investment notably declined by -10.1%, reflecting ongoing challenges in China’s real estate market.

On a positive note, retail sales rose by 3.7% yoy, surpassing the expected 3.0%. This indicates resurgence in the consumer sector, which could provide a buffer against the broader economic slowdown.

Intense week ahead: RBA, SNB, BoE, CPI, retail sales, PMIs and more

The upcoming week promises to be exceptionally busy for global financial markets, with three central bank meetings, the release of minutes from two others, and a plethora of important economic data across major economies.

RBA is set to hold its policy meeting on Tuesday, with widespread expectations that it will maintain official cash rate at 4.35%. A recent Reuters poll, which surveyed 43 economists, unanimously anticipates RBA to keep rates steady, with a near 90% consensus projecting no change for the next quarter too. However, expectations are leaning towards a 25 bps rate cut in the fourth quarter. Currently,The bar for another rate hike by RBA appears high for now. Given the current economic climate, RBA is likely to maintain its flexible stance of “not ruling anything in or out,” thereby keeping market participants alert and prepared for any shifts, while continuing to address still-elevated inflation levels by holding interest rate at current level for longer.

SNB faces a more complex decision. Earlier this month, SNB President Thomas Jordan highlighted the inflationary risks associated with the depreciation of Swiss Franc, which could be addressed by market intervention. This would typically suggest a cautious approach with unchanged interest rates. However, the Franc’s strong rally last week—spurred by the political crisis in France and ongoing uncertainty in the EU—might provide SNB enough room to consider a second rate cut this year to 1.25%.

Looking towards BoE, while the path towards policy easing is evident, the timing of the first rate cut is not expected this June, especially with the general election looming on July 4. A Reuters poll indicates that most economists foresee the first rate cut occurring in August, with predictions of a total of two 25 bps reductions by the end of 2024, bringing Bank Rate down from 5.25% to 4.75%. A significant number also anticipate a more aggressive cut totaling 75bps. This meeting’s focus will be on whether additional Monetary Policy Committee members will join Dave Ramsden and Swati Dhingra in voting for a rate cut.

In terms of central bank communications, BoJ and BoC will publish their meeting minutes, providing further insight into their respective policy discussions. ECB is also set to release its monthly economic bulletin.

On the data front, the week is loaded with key releases: CPI data from the UK and Japan; retail sales figures from Canada, the UK, and the US; and PMIs from Australia, Japan, the Eurozone, the UK, and the US. Additionally, Germany’s ZEW economic sentiment index and New Zealand’s GDP data will be closely watched too.

Here are some highlights for the week:

- Monday: New Zealand BNZ services index; Japan machine orders; China industrial production, retail sales, fixed asset investment; Swiss SECO economic forecasts; Canada housing start; US Empire state manufacturing index.

- Tuesday: RBA rate decision; Eurozone CPI final; German ZEW economic sentiment; US retail sales, industrial production, business inventories.

- Wednesday: Japan trade balance, BoJ minutes; UK CPI, PPI; Eurozone current account; US NAHB housing index; BoC summary of deliberations.

- Thursday: New Zealand GDP; Swiss trade balance, SNB rate decision; ECB monthly bulletin; BoE rate decision; US jobless claims, Philly Fed survey, housing starts and building permits.

- Friday: Japan CPI, PMIs; UK retail sales, PMIs; Eurozone PMIs; Canada retail sales; US PMIs, existing home sales.

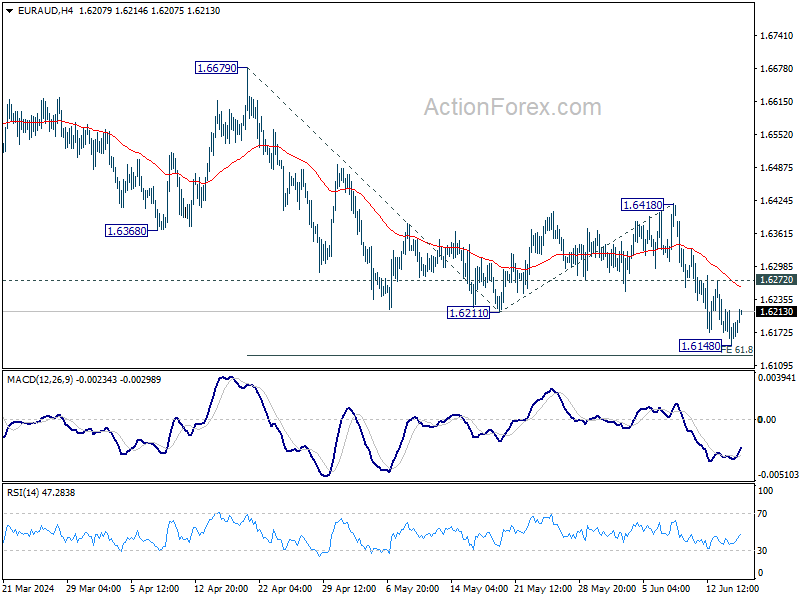

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6143; (P) 1.6181; (R1) 1.6212; More…

Intraday bias in EUR/AUD is turned neutral first with current recovery. Some consolidations could be seen above 1.6148. But outlook will stay bearish as long as 1.6418 resistance holds. Firm break of 61.8% projection of 1.6679 to 1.6211 from 1.6418 at 1.6129 will pave the way to 100% projection at 1.5950.

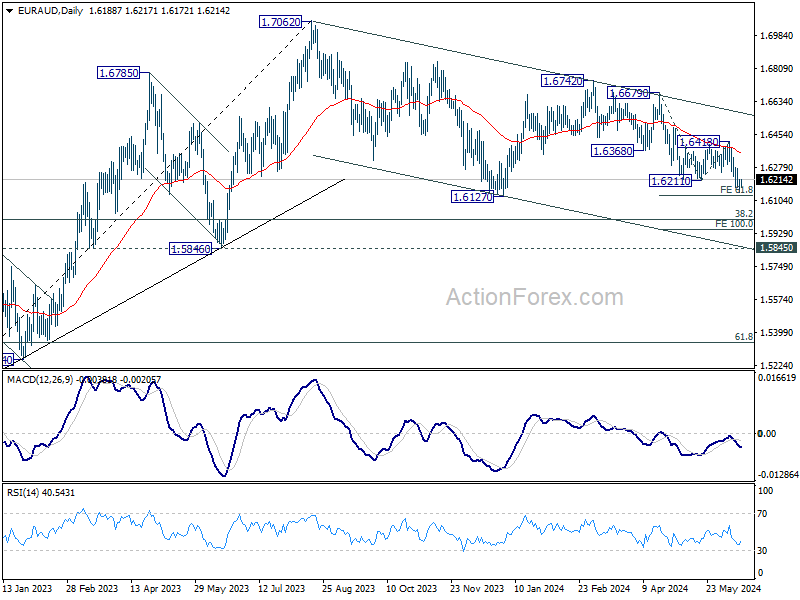

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 43 | 47.1 | 46.6 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jun | 0.00% | 0.80% | ||

| 23:50 | JPY | Machinery Orders M/M Apr | -2.90% | -3.10% | 2.90% | |

| 02:00 | CNY | Industrial Production Y/Y May | 5.60% | 6.00% | 6.70% | |

| 02:00 | CNY | Retail Sales Y/Y May | 3.70% | 3.00% | 2.30% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 4.00% | 4.20% | 4.20% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 12:15 | CAD | Housing Starts Y/Y May | 241K | 240K | ||

| 12:30 | USD | Empire State Manufacturing Index Jun | -13 | -15.6 |