Global markets were buoyed by pervasive risk-on sentiment last week, with both FTSE and DAX setting new records and major US indices posting substantial gains. Even Hong Kong HSI extended its rally from January’s lows by 25%, underscoring a broad uptick in investor confidence. In Europe, enthusiasm was particularly pronounced following the ECB’s reaffirmation of its conditional guidance for a rate cut in June. BoE likewise moved closer to monetary easing, further lifting spirits in the financial markets.

Currency movements, however, presented a more subdued picture, with most major pairs and crosses finishing within the previous week’s range. Japanese Yen underperformed, giving back some of its recent gains, which were fueled by rumored market interventions the week prior. Sterling and Swiss Franc were the next worst, with the Pound reacting to BoE’s dovish shift.

Conversely, New Zealand Dollar emerged as the week’s strongest performer, buoyed by its recovery against Australian Dollar, which faced pressure from less hawkish than anticipated stance from RBA. Canadian Dollar stood out as the second best, driven by robust job data that dampened expectations for an imminent rate cut by BoC. Euro ranked as the third strongest currency while Dollar and Aussie ended the week in the middle of the pack.

UK Economic Recovery and BoE Rate Cut Hopes Propel FTSE to New Record

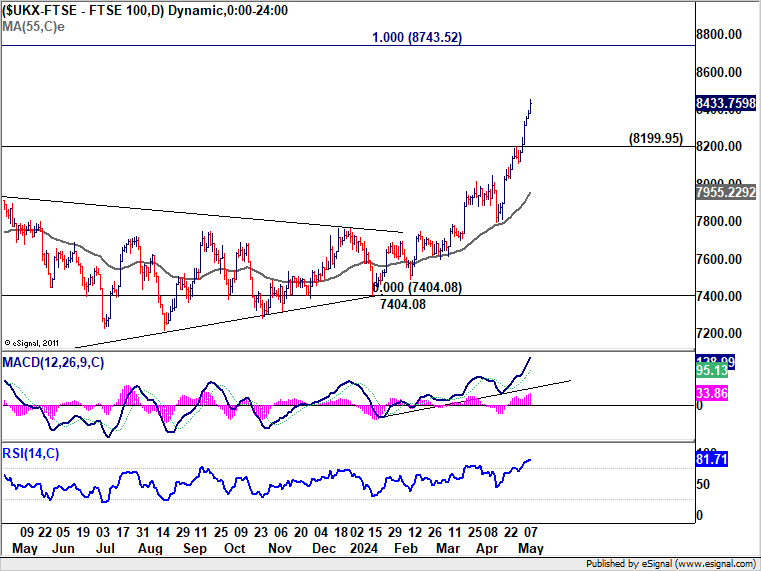

FTSE index soared to new record high following UK GDP figures release, which confirmed that the British economy has officially emerged from recession. The data revealed a robust first-quarter growth of 0.6% qoq, the largest expansion seen since 2021. Additionally, growth rate for March alone stood at 0.4% mom, signaling that the economic recovery is not only underway but also gaining momentum

Concurrently, BoE appears to be inching closer to reducing interest rates. Despite holding the bank rate steady at 5.25%, the tone of the meeting was decidedly dovish. Notably, Deputy Governor Dave Ramsden and Swati Dhingra, a known dovish member, both advocated for a rate cut, resulting in a 7-2 vote. This move, coupled with Governor Andrew Bailey’s remarks that a June rate cut is “neither ruled out nor a fait accompli,” points to a possible easing in monetary policy in the near term.

Nevertheless, Chief Economist Huw Pill added a note of caution to the conversation, advising that excessive focus on June might be “probably a little bit ill-advised.” Despite this caution, the markets are currently pricing in around 50% chance of a rate reduction in June. A rate cut in August is fully priced in, with another reduction anticipated in November.

Technically, FTSE is in upside acceleration phase as seen in D MACD as well as D RSI. Near term outlook will remain bullish as long as 8199.95 support holds. Next target is 100% projection of 6707.62 to 8047.06 from 7404.08 at 8743.52.

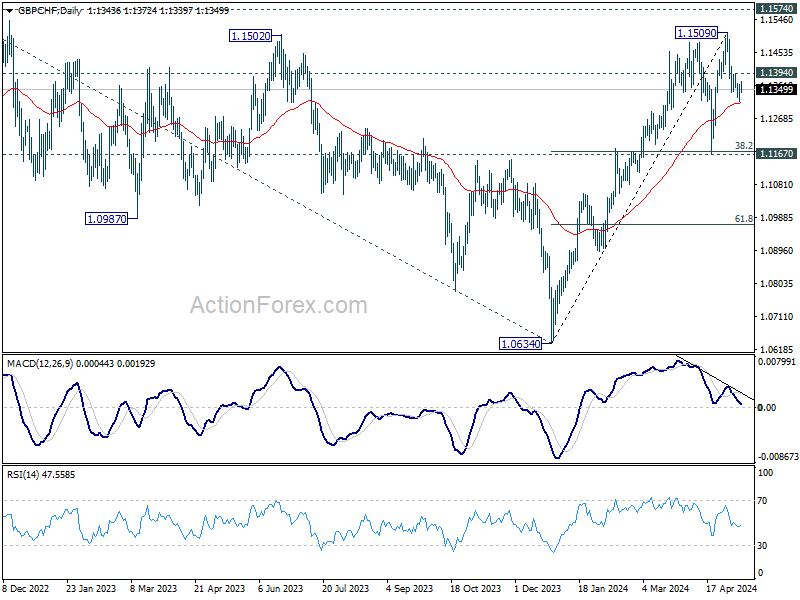

As for Sterling, it has been struggling against Euro and Swiss Franc recently on BoE rate cut expectations too. Considering bearish divergence condition in D MACD, a short term top should be formed at 1.1509, ahead of 1.1574 key resistance. Firm break of 55 D EMA (now at 1.1312) should confirm that GBP/CHF is in correction to whole rise from 1.0634. Deeper fall should then be seen to 1.1167 cluster support (38.2% retracement of 1.0634 to 1.1509 at 1.1175). Strong support is expected there to bring rebound and set the range for sideway consolidations.

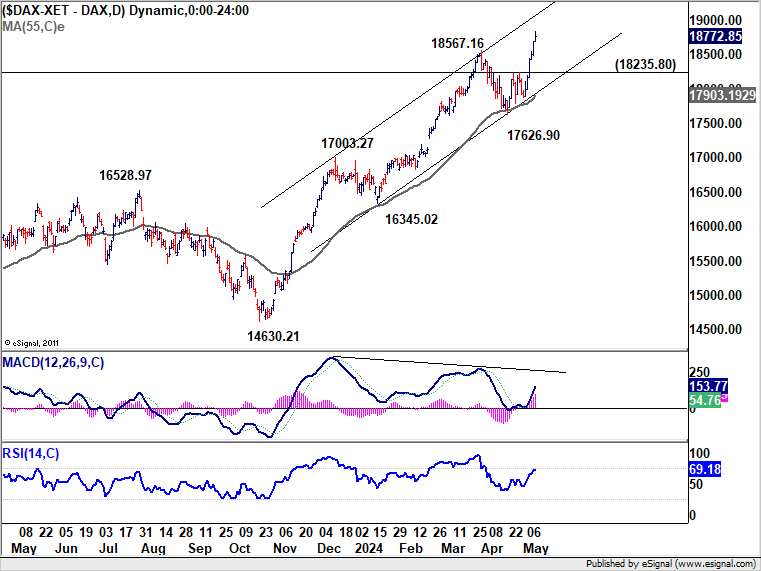

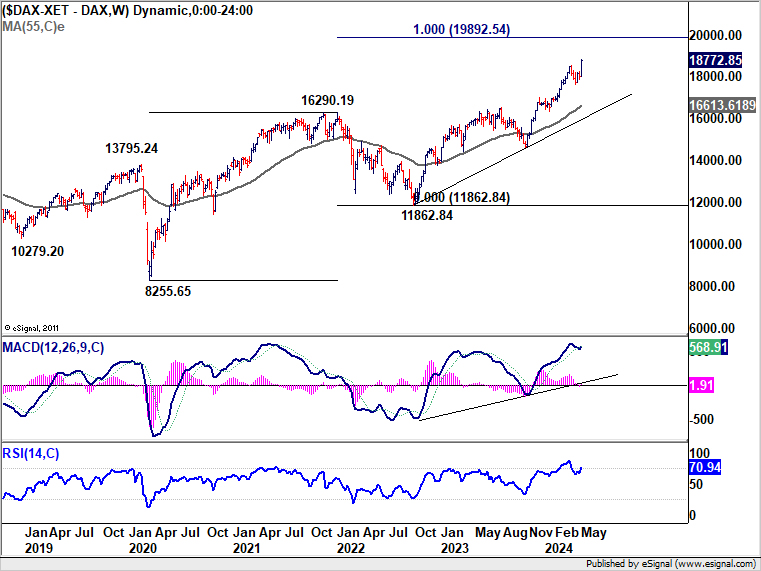

DAX also hits record, ECB on track for June cut

DAX also surged to new record high, buoyed by broad risk-on sentiment and expectations that ECB will soon ease monetary policy. According to the minutes from ECB’s April meeting, while a “very large majority” preferred to hold rates steady for another session, a few members were “sufficiently confident” to support a rate cut at that time. The meeting accounts suggested that it is “plausible that the Governing Council would be in a position to start easing monetary policy restriction at the June meeting.”

Near term outlook in DAX will stay bullish as long as 18235.90 support holds. Next target is 100% projection of 8255.65 to 19892.54 from 11862.84 at 19892.54. However, considering bearish divergence condition in D MACD, upside could be limited there to bring consolidations.

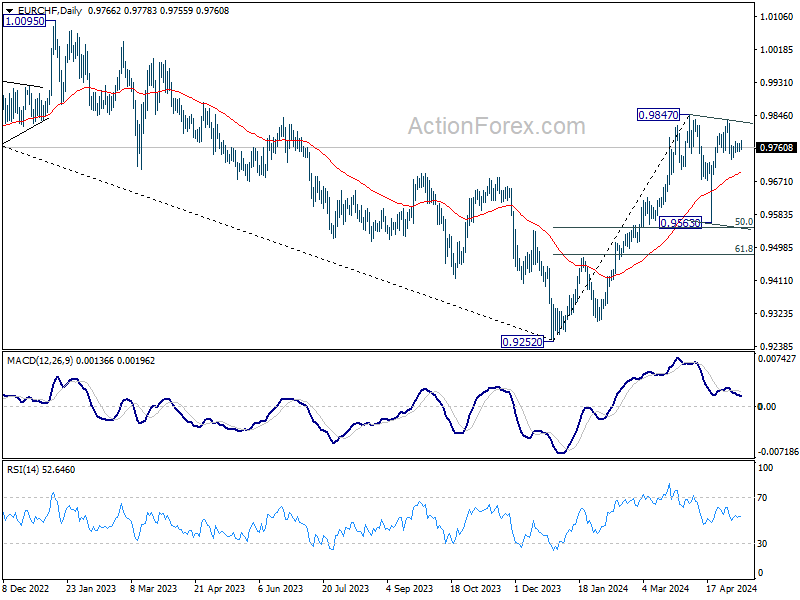

Euro has also seen some weakness against Swiss Franc recently, mainly due to ECB’s easing expectations juxtaposed against SNB more advanced rate-cutting cycle. SNB has already begun cutting rates as of March. However, SNB’s policy rate now at just 1.50%, Comparing to ECB’s deposit rate of 4.00% and BoE’s rate of 5.25%, there is more room for the latter two on rate reductions. Both EUR/CHF and GBP/CHF could stay soft in the near term, until there are more ideas on where the terminal rates for these three central banks would be.

As for EUR/CHF, corrective pattern from 0.9847 is seen as in its third leg already. Deeper decline is expected to 55 D EMA (now at 0.9691). Firm break there will pave the way to 0.9563. But strong support is expected from 50% retracement of 0.9252 to 0.9847 at 0.9550 to complete the pattern.

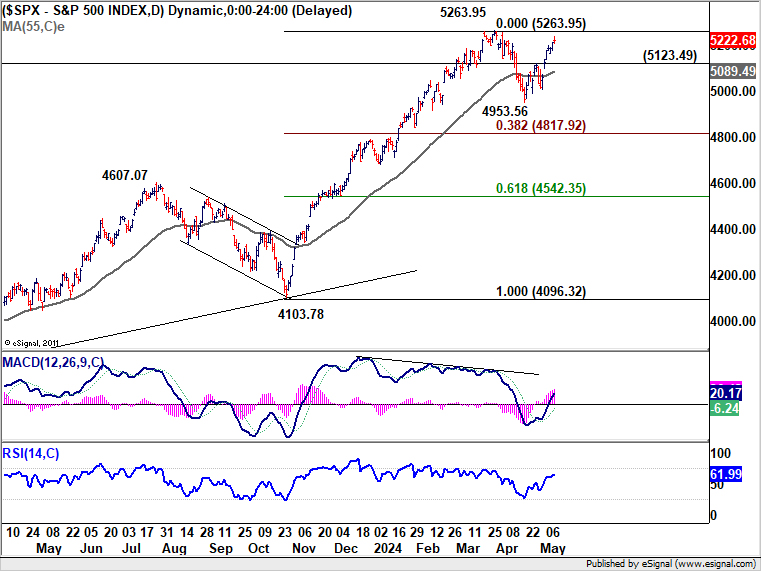

US Equities Extend Gains, Dollar Index continues Consolidation

In the US, the stock markets continued their impressive rebound but Dollar and Treasury Yields have shown little movement. The optimism in equity markets stems from Fed’s recent indications that an interest rate hike is not on the table. However, the overarching challenge remains as Fed has signaled that high interest rates will persist longer than initially anticipated to address stubborn inflationary pressures.

Meanwhile, Investor enthusiasm received a check from the latest University of Michigan consumer survey, which indicated further rise in both short-term and medium-term inflation expectations. According to the survey, one-year inflation expectation increased from 3.2% to 3.5% in May, while five-year expectations edged up from 3.0% to 3.1% . These figures remind the markets that consumer anxiety about inflation is not abating. Traders will likely turn cautious until the upcoming US CPI data provide further guidance.

Technically, S&P 500’s rebound from 4953.45 is seen as the second leg of the corrective pattern from 5263.95. Strong resistance should be seen from 5263.95 to cap upside. Break of 5123.49 support will indicate that the third leg has started. In the case, deeper call would be seen to 4953.56, and possibly below to 38.2% retracement of 4096.32 to 5263.96 at 4817.92. However, decisive break of 5263.96 will invalidate this view and confirm larger up trend resumption.

Dollar Index recovered after drawing support from 55 D EMA, but there is no clear upside momentum yet. Corrective fall from 106.51 could still resume to lower channel support (now at 104.00). Strong support from there would retain near term bullishness for resuming the rise fro 100.61 through 106.51 at a later stage. However, sustained break of the channel will argue that rebound from 100.61 has completed as a three-wave corrective move. Deeper fall would then be seen through 102.35 support in this bearish case.

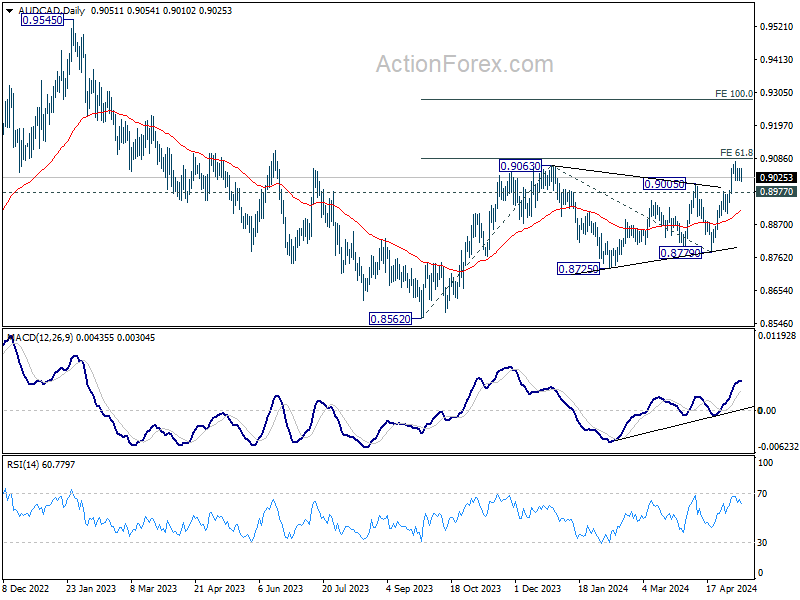

AUD/CAD Rally Hits Pause as Markets Reassess RBA and BoC

Australian Dollar ended the week on a mixed note as market speculations for further RBA rate hikes cooled significantly. In her post-meeting press conference, RBA Governor Michele Bullock provided a clear signal, stating, “we don’t think we necessarily have to tighten again.” This stance suggests that RBA plans to maintain the current interest rate for an extended period to continue addressing inflation pressures effectively. Following this announcement, the Cash Rate Implied Yield Curve adjusted, showing a flattening trend with projections not exceeding the current cash rate of 4.35%. Meanwhile, markets have only fully priced in the first rate cut for June of the following year.

Conversely, Canadian market pared back its expectations for an imminent rate cut by BoC following exceptionally strong job data. The economy added 90k jobs, marking the most substantial increase since January 2023. Although annual wage growth slowed slightly from 5.1% to 4.8%, it remains elevated. The likelihood of a June rate cut has been reduced to 48% from 54%. A cut is now priced in for September, a delay from July anticipated before the job report. Nevertheless, the upcoming inflation report on May 21 will be even more crucial in shaping the outcome of June BoC meeting.

These developments capped AUD/CAD upward momentum, as it stalled below 61.8% projection of 0.8562 to 0.9063 from 0.8779 at 0.9098. Nevertheless, near term outlook will stay bullish as long as 0.8977 support holds. Firm break of 0.9098 could prompt upside acceleration to 100% projection at 0.9280.

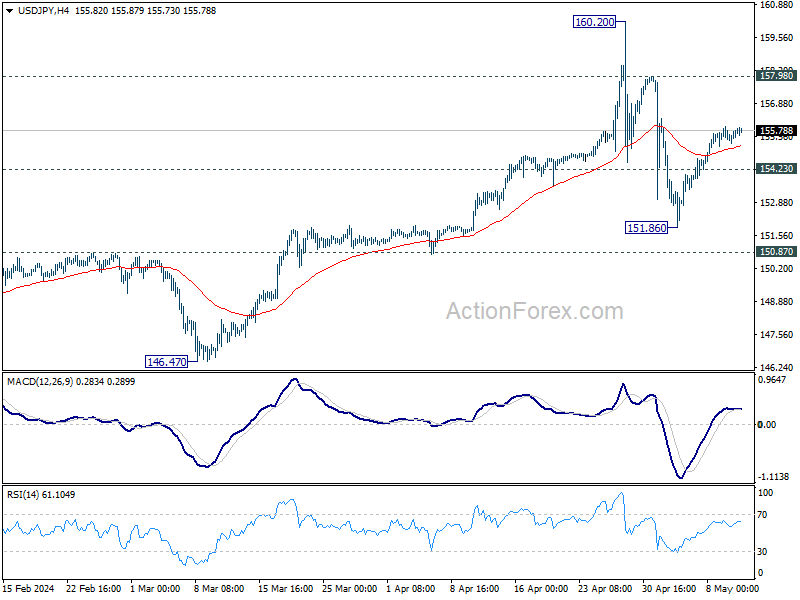

USD/JPY Weekly Outlook

USD/JPY’s rebound last week suggests that pullback from 160.20 has completed at 151.86 already. It’s now in the second leg of the corrective pattern from 160.20. Further rise could be seen towards 157.98 resistance. On the downside, break of 154.23 will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

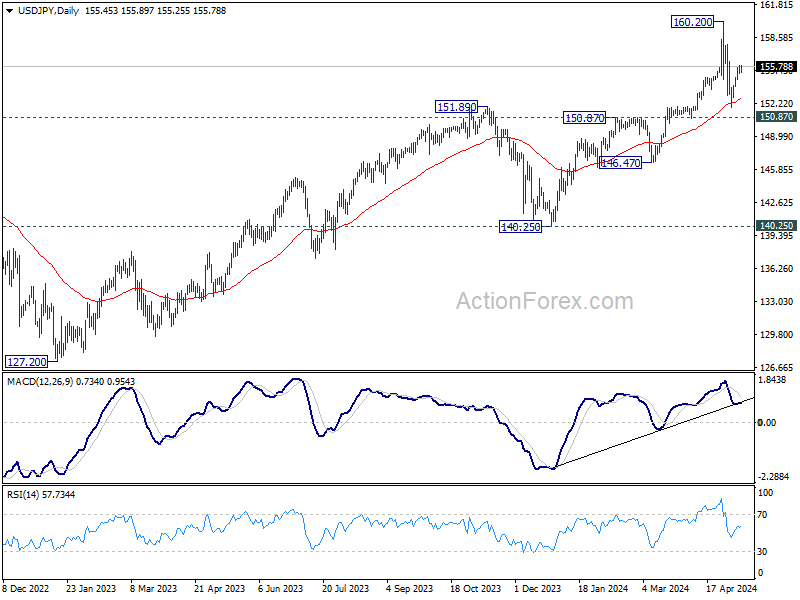

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

In the long term picture, as long as 140.25 support holds, up trend from 75.56 (2011 low) is still in progress. Next target is 138.2% projection of 75.56 (2011 low) to 125.85 (2015 high) from 102.58 at 172.08.