The US session was informed most by the University of Michigan consumer sentiment preliminary data which showed a sharp decline in the sentiment index to 67.4 from 76.0 . The expectations also fell sharply to 66.5 from 75.0 and current conditions also tumbled to 68.8 versus 79.0. To make the data even worse when you inflation expectations rose to 3.5% from 3.2% last month which was the highest level since November 2023. The five year inflation also rose to 3.1% from 3.0% last month.

Although somewhat shocking, there were reports that this month marked the first month that the survey was done electronically versus through phone calls (people pick up phones and answer questions on the economy….hmmmm). The commentary was that statistically people are more pessimistic about inflation when surveyed online. I wonder if generally there also pessimistic about the economy in general.

Nevertheless, the news sent yields higher, and erased gains in the NASDAQ index in particular which was up +91.13 points at session highs before rotating to the downside to as much as -52.74 points lower on the day ast session lows. The index ended up closing near unchanged. The S&P was up 0.17% in the Dow Industrial Average average rose for the 8th consecutive day with a gain of 0.32%.

For the trading week, the Dow closed higher for the 4th consecutive week. Both the Nasdaq and the S&P closed up for the 3rd straight week:

- Dow Industrial Average average rose 2.16%

- S&P index rose 1.85%

- NASDAQ index rose 1.14%

In the US debt market, the yield closed higher across the curve with the shorter end up the most:

- 2- year yield 4.871%, +6.5 basis points

- 5-year yield 4.516%, +5.6 basis points

- 10 year yield 4.500%, +5.1 basis points

- 30-year yield 4.642%, +4.2 basis points

For the trading week, the yields were mixed with the shorter end rising and the longer end falling:

- 2-year was up 5.2 basis points

- 5-year was up 2.8 basis points

- 10-year was down -1.2 basis points

- 30-year was down -2.6 basis points

There was more Fedspeak today with Fed’s Kashkari, Chicago Fed Pres. Goolsbee and Dallas Fed Pres. Lorie Logan all speaking.

Neel Kashkari from the Federal Reserve discussed economic issues and monetary policy, highlighting persistent U.S. housing supply challenges and the impact of higher interest rates on reducing this supply in the short term. Kashkari emphasized the necessity of controlling inflation and noted that low interest rates alone wouldn’t resolve housing issues. He expressed caution about the restrictiveness of current monetary policies, pointing out that the business community doesn’t view financial conditions as tight. Currently in a “wait and see” mode, Kashkari is open to the possibility of future rate hikes but notes that any decision to increase rates would require significant justification. He remains uncertain about the neutral rate’s current level, suggesting a period of steady rates ahead unless conditions change markedly.

Meanwhile, Chicago Fed Pres. Goolsbee was also talking a lot today discussed the managing inflation, particularly emphasizing the 2% target as an anchor for expectations. He acknowledged the current high short-term inflation expectations but cautioned against overreacting to these. Goolsbee highlighted that although inflation has not shown signs of settling at 3%, the real Fed funds rate is the highest it has been in decades, suggesting a restrictive monetary policy stance. He mentioned the complexity of interpreting recent data due to positive supply developments, including a significant boost from increased immigration which adds approximately 80,000 jobs monthly. Housing inflation remains a critical concern, with rates contributing to supply issues but not fully explaining the persistent high inflation in housing. Despite various economic indicators and the challenges of housing inflation, Goolsbee remains cautiously optimistic about reaching the 2% inflation target, provided housing inflation decreases. He also noted the ongoing recovery of supply chains and potential lasting benefits from labor supply increases into 2024, maintaining a stance that nothing is off the table in terms of policy adjustments to control inflation.

Finally, Dallas Fed Pres. Lorie Logan was probably the most hawkish of the three. Logan highlighted that the Federal Reserve has made substantial progress on combating inflation, noting that the economy and labor market are currently strong. However, she expressed concerns, stating that the fight against inflation is not over as the first quarter inflation data was disappointing. Logan pointed out the presence of significant upside risks to inflation and uncertainties around whether the current policy is sufficiently restrictive. She emphasized that it is too early to consider lowering interest rates and stressed the importance of maintaining flexibility in monetary policy. Additionally, Logan suggested that the neutral interest rate level, which balances the economy without stimulating or restraining growth, may have risen, indicating a possible shift in the economic environment that could affect future policy decisions.

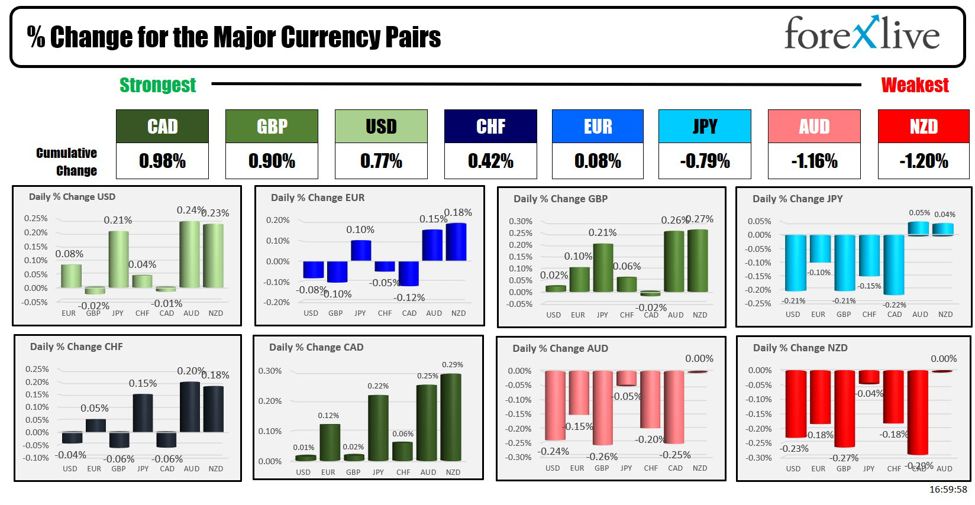

In the forex market, the major indices are ending the day fairly scrunched together in up and down trading. The CAD was the strongest of the major currencies, while the NZD was the weakest.

The strongest to the weakest of the major currencies

For the trading week, the greenback is ending mixed and little changed vs the major currencies. Below are the % changes of the greenback vs the major currencies:

- EUR, -0.08%

- JPY, +1.849%

- GBP, +0.20%

- CHF, +0.16%

- CAD, -0.11%

- AUD, +0.12%

- NZD, -0.9%

Thank you for your support this week and wish you all a wonderful weekend.