Japanese Yen’s accelerated decline captured significant attention in Asian session, while the broader currency markets remained generally stable. Market participants interpret the apparent lack of urgency from Japanese officials to address Yen’s fall as a tacit approval for its continued depreciation. This perspective gains significance following the recent trilateral meeting between Japan, South Korea, and the US, where the sharp decline of Yen was a subject of “serious concerns.” Speculation is rife that Japan might tolerate Yen’s fall to 160 mark against Dollar before taking any corrective actions.

Concurrently, Dollar is also soft as traders anticipate US Q1 GDP advance report. The US economy is expected to show 2.1% annualized growth in Q1, slowed from Q4’s 3.4%. GDP price index is expected to jump from 1.6% to 3.0%. If these projections hold, they would suggest that the economy is continuing to expand at a healthy rate with little risk of recession. This scenario is likely to support Fed’s cautious stance on interest rate cuts. A detailed breakdown showing robust consumer spending could even delay Fed’s first rate cuts further.

In terms of weekly performance, Yen is currently the weakest among major currencies, followed by Dollar and Swiss Franc. In contrast, Australian Dollar leads as the strongest, followed by Kiwi and Euro, while Sterling and Canadian Dollar hold middle positions. This configuration aligns with the prevailing risk-on sentiment, evidenced by strong rebound in US stock indices and new record high in FTSE.

Technically, a focus today is whether AUD/USD, in reaction to broader risk sentiment, could break through 55 D EMA (now at 0.6526) decisively. In this case, fall from 0.6870 could have completed with three waves down to 0.6361 already. Stronger rally would be seen to 0.6643 resistance first. However, rejection by 55 D EMA, followed by break of 0.6440 minor support will retain near term bearishness, and resume the decline through 0.6361 instead.

In Asia, at the time of writing, Nikkei is down -1.98%. Hong Kong HSI is up 0.25%. China Shanghai SSE is up 0.13%. Singapore Strait Times is down -0.40%. Japan 10-year JGB yield is up 0.0019 at 0.893. Overnight, DOW fell -0.11%. S&P 500 rose 0.02%. NASDAQ rose 0.10%. 10-year yield rose 0.054 to 4.6552.

Yen’s selloff intensifies as BoJ meeting commences

Yen’s selloff is intensifying and breaking through 155 mark against Dollar as BoJ commences its two-day policy meeting. While no changes in policy are anticipated at this gathering, the continued decline of Yen could provoke hawkish remarks from Governor Kazuo Ueda. He has clearly indicated that a policy adjustment would be considered if weakening Yen’s impact on inflation becomes too significant to overlook.

Attention is also turning towards BoJ’s new economic projections. Inflation forecasts for fiscal years 2024 and 2025 are expected to be upgraded from current predictions of 2.4% and 1.8%, respectively. For fiscal 2026, forecasts could suggest that core inflation will align closely with BoJ’s target of 2%.

Governmental response to Yen’s decline has so far been constrained. Finance Minister Shunichi Suzuki reiterated today that there has been no alteration in the government’s approach towards Yen’s valuation, emphasizing that actions will be taken as appropriate. He added that the government is “carefully monitoring” currency market movements, but declined from further comments.

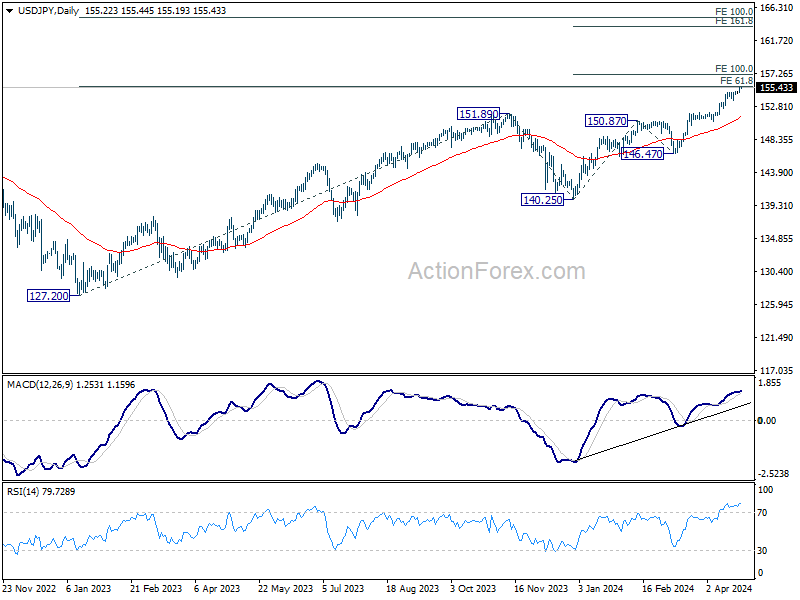

Technically, strong resistance could be seen from 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20 to limit USD/JPY’s rally on the first attempt. However, firm break of this level will put 100% projection of 140.25 to 150.87 from 146.47 at 157.09 as next near term target.

BoC members divided on rate cut timing, united on gradual easing approach

BoC’s April meeting summary revealed a “diversity of views” among its members concerning the timing of the first interest rate cut. Despite differing opinions, there was a unanimous agreement that any adjustment to monetary policy would “probably be gradual” once initiated.

Key concerns highlighted by some board members included the need for “more reassurance” regarding the diminishing risks associated with stalling of progress on slowing core inflation. These members observed that the Canadian economy is “performing well”, mitigating the risk that the current restrictive monetary policy could excessively decelerate economic activity. However, they cautioned that stronger domestic demand, alongside robust economic growth in the US, “keep core inflation from slowing further” or might even cause it to “pick up again in the event of new surprises”.

Conversely, other members argued that there is a tangible risk of maintaining a monetary policy that is “more restrictive than needed.” This group emphasized the significant progress already achieved in reducing inflation, noting that the rates of inflation across most goods and services had “come down significantly,” and the distribution of inflation rates among the CPI components had begun to “approach normal.”

Despite these differing perspectives, the consensus was clear that any forthcoming policy easing would be implemented cautiously. “While there was a diversity of views about when conditions would likely warrant cutting the policy rate, they agreed that monetary policy easing would probably be gradual, given risks to the outlook and the slow path for returning inflation to target,” the summary stated.

Looking ahead

German Gfk consumer climate and ECB monthly bulletin will be released in Euroepan session. Later in the day, US Q1 GDP advance is the main focus. Jobless claims, trade balance, and pending home sales will also be released.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.67; (P) 165.95; (R1) 166.50; More…

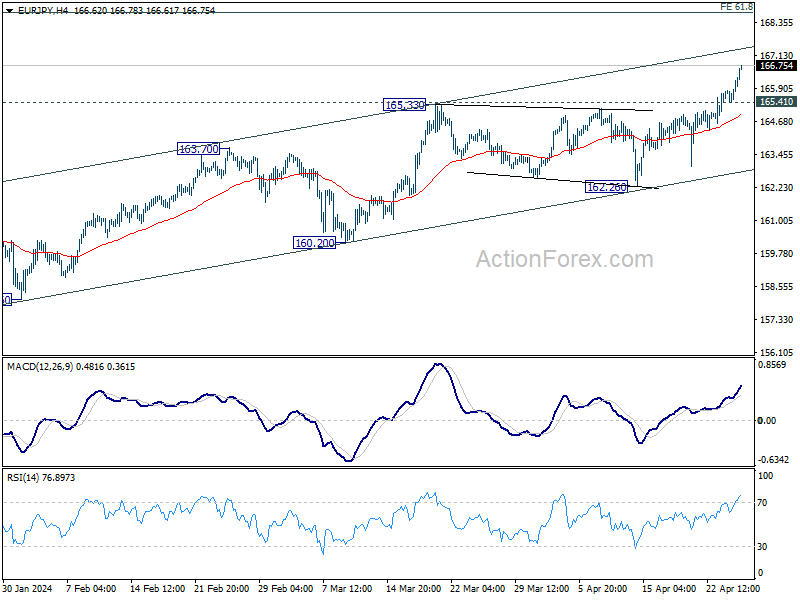

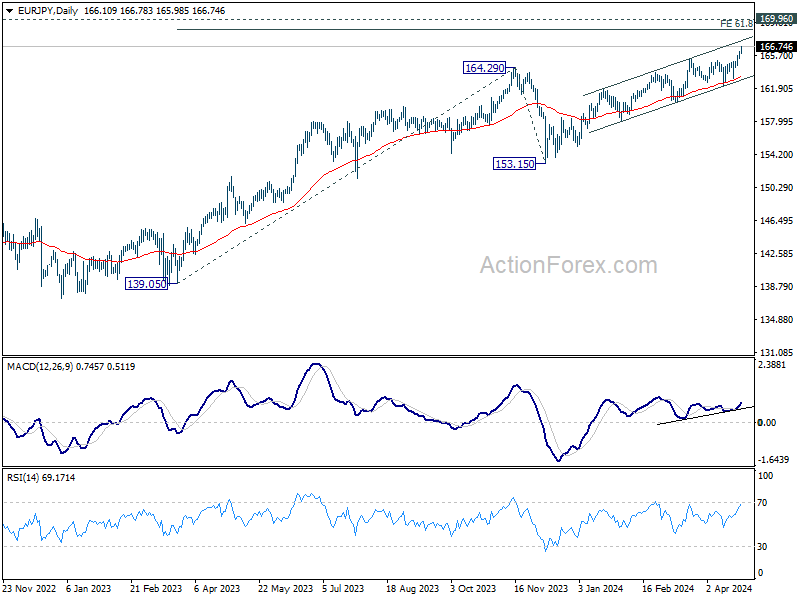

EUR/JPY’s up trend continues to as high as 166.78 so far. Intraday bias stays on the upside for 168.72 projection level next. On the downside, below 165.41 minor support will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 61.8% projection of 139.05 to 164.29 from 153.15 at 168.72, or even further to 169.96 (2008 high). Break of 162.26 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Confidence May | -25.5 | -27.4 | ||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 19) | 210K | 212K | ||

| 12:30 | USD | GDP Annualized Q1 P | 2.10% | 3.40% | ||

| 12:30 | USD | GDP Price Index Q1 P | 3.00% | 1.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -91.2B | -90.3B | ||

| 12:30 | USD | Wholesale Inventories Mar P | 0.20% | 0.50% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | 0.90% | 1.60% | ||

| 14:30 | USD | Natural Gas Storage | 50B |