Significant volatility was seen in Asian session, following the news of Israel’s missile strike in retaliation against Iran. This geopolitical development initially led to steep decline in Asian stocks and concurrent surge in oil prices and safe-haven assets like Swiss Franc, Yen, and Dollar. Nevertheless, fund flows started to reverse partially as the situation seemed to stabilize somewhat, as likelihood of immediate further escalation appeared to diminish.

Iran attempted to downplay the severity as its state media denied any foreign military presence in their airspace. Temporary flight restrictions that had been placed near the Isfahan military base were also lifted quickly. Meanwhile, Israel maintained silence on the issue, neither confirming nor denying involvement in the strikes.

As the day progresses, Swiss Franc, Yen, and Dollar are trading as the strongest currencies, bolstered by their status as traditional safe havens during times of international tension. Conversely, Aussie, Kiwi, and Sterling are underperforming as investors shy away from riskier assets. Euro and Canadian Dollar are situated in the middle of the currency spectrum. But the picture could dramatically alter depending on further developments from the Middle East conflict.

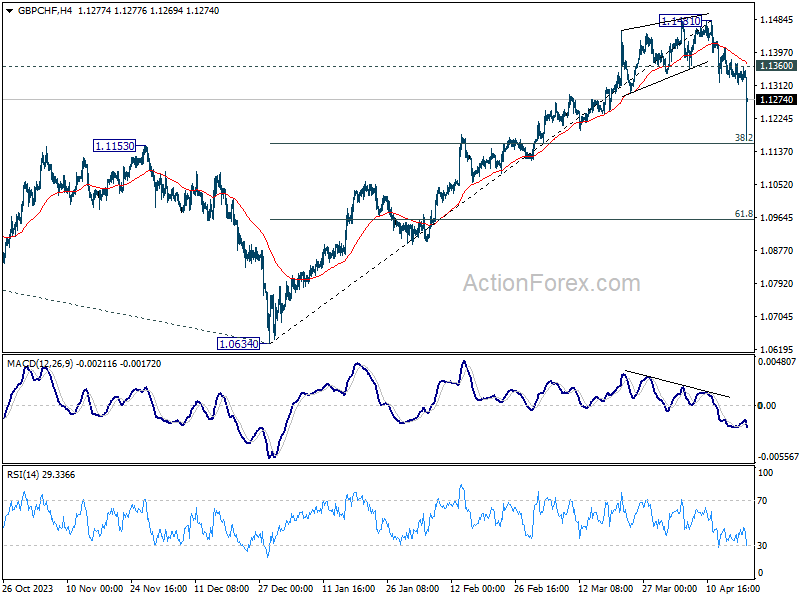

Technically, while GBP/CHF dived sharply today, downside is contained by 38.2% retraceent of 1.0634 to 1.1481 at 1.1157 so far. Price actions from 1.1481 are seen as developing into a consolidation pattern to rally from 1.0634 only, with range set between 1.1157 and 1.1481. Break of 1.1360 will bring further rebound to retest 1.1481 high. However, firm break of 1.1157 will bring deeper fall to 61.8% retracement at 1.0958, even just as a deep correction.

In Asia, at the time of writing, Nikkei is down -2.48%. Hong Kong HSI is down -1.23%. China Shanghai SSE is down -0.40%. Singapore Strait Times is down -0.59%. Japan 10-year JGB yield is down -0.0276 at 0.843. Overnight, DOW rose 0.06%. S&P 500 fell -0.22%. NASDAQ fell -0.52%. 10-year yield rose 0.062 to 4.647.

Oil and safe havens rally amid new Middle East conflict

Oil prices surges sharply in Asian session and there was a significant influx into safe-haven assets such as Gold, Dollar, Swiss Franc, and Japanese Yen.

This market reaction was triggered by escalating tensions in the Middle East, following a report by ABC News on a retaliatory missile strike by Israel against Iran. Meanwhile, Iran’s Fars news agency also reported that explosions were heard near the Isfahan airport,m even though the causes were unknown.

The missile launches are continuation of hostilities following last Saturday when Iran targeted Israel with over 300 drones and missiles, a majority of which were intercepted by Israel and its allies.

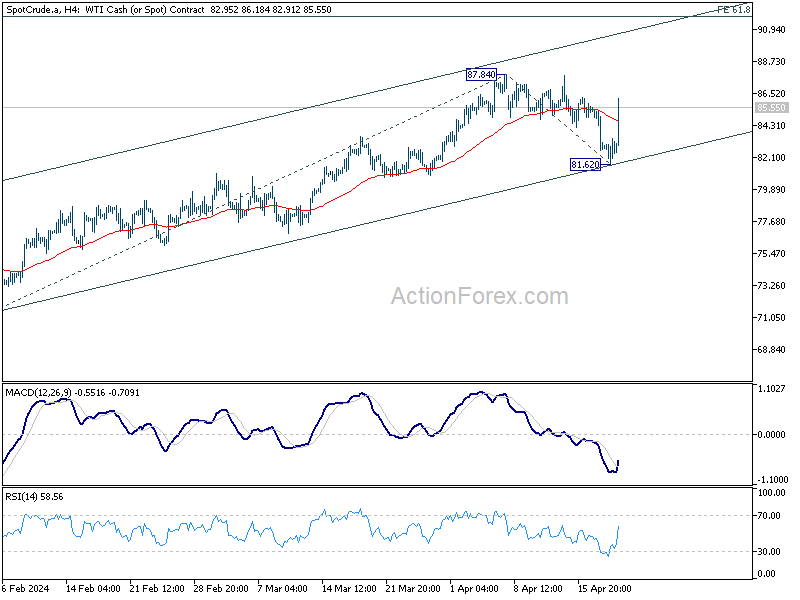

WTI oil’s strong rebound today suggests that corrective pullback from 87.84 has completed at 81.62 already. Further rise would be seen to retest 87.84 resistance first. Decisive break there will resume whole rally from 67.79 and target 61.8% projection of 71.32 to 87.84 from 81.62 at 91.82 next.

Also, note that rise from 67.79 is seen as the third leg of the pattern from 63.67 (2023 low). Hence, break of 95.50 is possible in the medium term, depending on whether WTI could sustain its upside momentum.

BoJ’s Ueda: Impact of weak Yen on inflation could lead to policy shift

During a press conference today, BoJ Governor Kazuo Ueda highlighted the potential economic repercussions of the persistently weak yen, particularly its effect on trend inflation through increased costs of imported goods.

“There’s a possibility the weak yen could push up trend inflation through rises in imported goods prices,” Ueda noted, indicating that such a scenario “might lead to a change in monetary policy.”

At the same occasion, Finance Minister Shunichi Suzuki pointed out that exchange rates are not solely influenced by interest rate differentials. Various other factors, such as each country’s current account balance, market participants’ sentiment, and speculative trade, drive currency moves,” Suzuki explained.

Japan’s CPI core slows to 2.6% in Mar, CPI core-core down to 2.9%

In March, Japan observed a subtle cooling in core inflation, though levels persistently exceed BoJ’s target.

Core CPI, which excludes food prices, slowed from 2.8% yoy to 2.6% yoy, slightly under the expectation of 2.7% yoy, marking a continued stretch above BoJ’s 2% target for two full years.

Further detail is seen in the core-core CPI, excluding both food and energy, which decreased from 3.2% yoy to 2.9% yoy. This marks the seventh consecutive month of deceleration and brings this measure below 3% level for the first time since November 2022.

Meanwhile, headline CPI dipped slightly from 2.8% year-on-year to 2.7%, aligning with analysts’ forecasts.

Fed’s Bostic emphasizes patience on rate cuts, open to rate hikes

Atlanta Fed President Raphael Bostic highlighted his readiness to maintain the current rate levels through the end of the year. “I’m comfortable being patient,” he noted at an event overnight. “I’m of the view that things are going to be slow enough this year that we won’t be in a position to reduce our rates towards … the end of the year.”

He pointed out the importance of continued job creation and wage growth that outpaces inflation as key metrics guiding his decision-making process. “If we can keep those things going, and inflation has the signs that it is moving to that target, I’m happy to just stay where we are,” he explained.

However, Bostic also warned of the potential need to adjust rates upward if inflation trends unfavorably, diverging from the Fed’s 2% target. “If inflation starts moving in the opposite direction away from our target, I don’t think we’ll have any other option but to respond to that,” he stated.

“I’d have to be open to increasing rates,” he added.

Fed’s Kashkari suggests rate cuts may wait until next year

Minneapolis Fed President Neel Kashkari told Fox News Channel that he wants to be “patient” regarding monetary easing. He added that the first rate cut could “potentially” be inappropriate until 2025.

“I’m in the view of, we need to wait and see, be patient as long as it takes, until we get convinced that inflation is on its way back down to 2%,” he said.

Greene: BoE in trade-off territory, rate cuts not near

BoE MPC member Megan Greene said at an event overnight that rate cut is no on the immediate horizon. She characterized that BoE is in a “trade-off territory”, in an environment of persistent high inflation coupled with weak growth in the UK.

“We have to weigh the risk of doing too much against the risk of doing too little,” Greene explained.

She expressed a particular concern that being too cautious could lead to more severe consequences down the line: “In my mind, doing too little is the bigger risk because you end up having to hike rates even higher in the end and could end up generating an even bigger recession,” she noted.

Looking ahead

UK retail sales and Germany PPI are the only economic data releases today.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6406; (P) 0.6432; (R1) 0.6446; More…

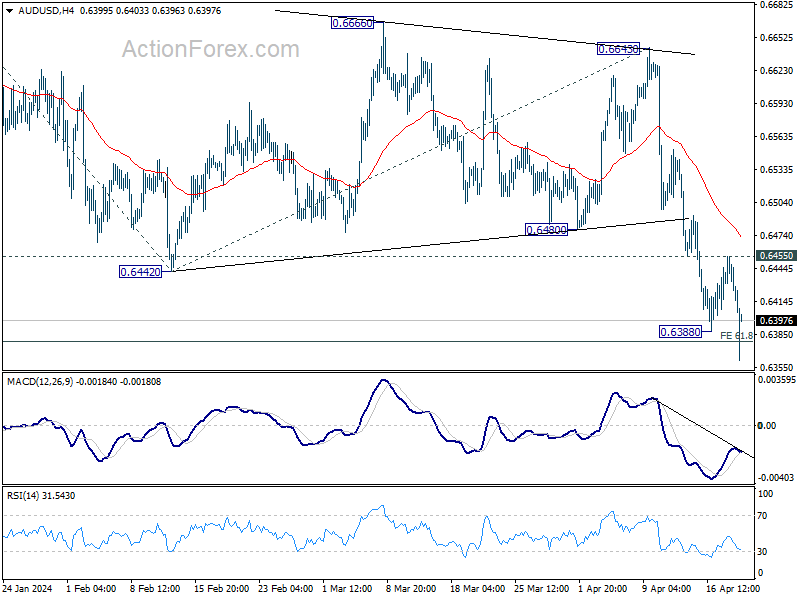

Intraday bias in AUD/USD is back on the downside a recent decline resumes through 0.6388 temporary low. Sustained break of 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378 will extend the fall from 0.6870 to 100% projection at 0.6215. On the upside, break of 0.6455 resistance will turn intraday bias neutral again first.

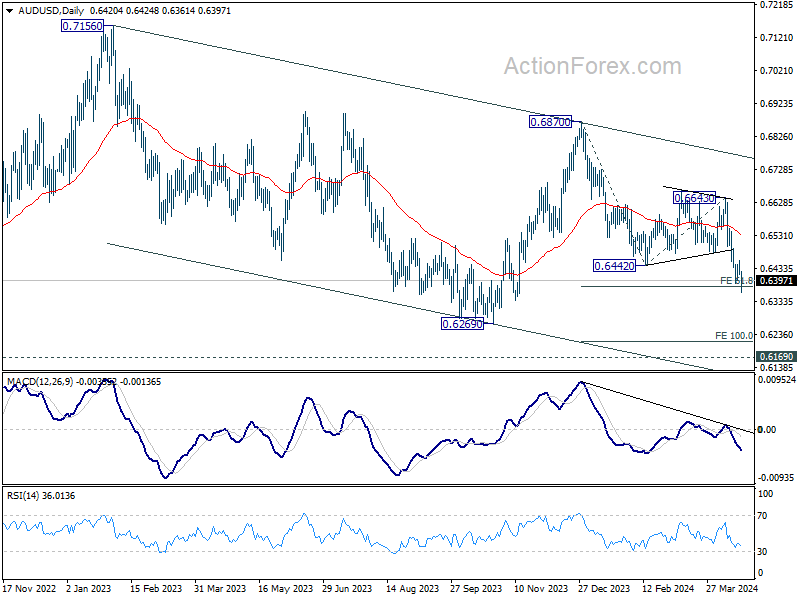

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Mar | 2.70% | 2.70% | 2.80% | |

| 23:30 | JPY | National CPI core Y/Y Mar | 2.60% | 2.70% | 2.80% | |

| 23:30 | JPY | National CPI core-core Y/Y Mar | 2.90% | 3.20% | ||

| 06:00 | GBP | Retail Sales M/M Mar | 0.30% | 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Mar | 0.00% | -0.40% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | -4.10% |