Japanese Yen declines broadly in today’s Asian session, reacting to dovish remarks made by BoJ Deputy Governor. The official’s commentary emphasized a cautious approach to monetary tightening, highlighting that even with exit from negative interest rate policy, the pace of interest rate hikes would remain measured.

This outlook, especially the suggestion that inflation could stabilize around the 2% target without prompting rapid policy adjustments, has contributed to Yen’s downward trajectory, setting the stage for further depreciation against major currencies in the coming days.

Nevertheless, Yen’s performance will still hinge on the movements of benchmark treasury yields in US and Europe.

At the same time, Australian and New Zealand Dollars weakened. This regional currency softness comes at a time when Chinese stock market is set to close for Lunar New Year holidays, pausing trading activities until February 18.

Instead of introducing concrete market supporting measures as rumored, China announced a notable change in leadership at the Securities Regulatory Commission. Yi Huiman, the outgoing chair, will be succeeded by Wu Qing, vice mayor of Shanghai during the stringent 2022 lockdown. Wu is also know for his strict regulation of traders that have earned him the moniker “Broker Butcher.”

Elsewhere in the market, Swiss Franc is making a modest recovery after yesterday’s selloff, while Euro and Sterling maintain their strength, as near term rebound continued. Canadian Dollar is also showing firmness, contrasting with the mixed performance of Dollar.

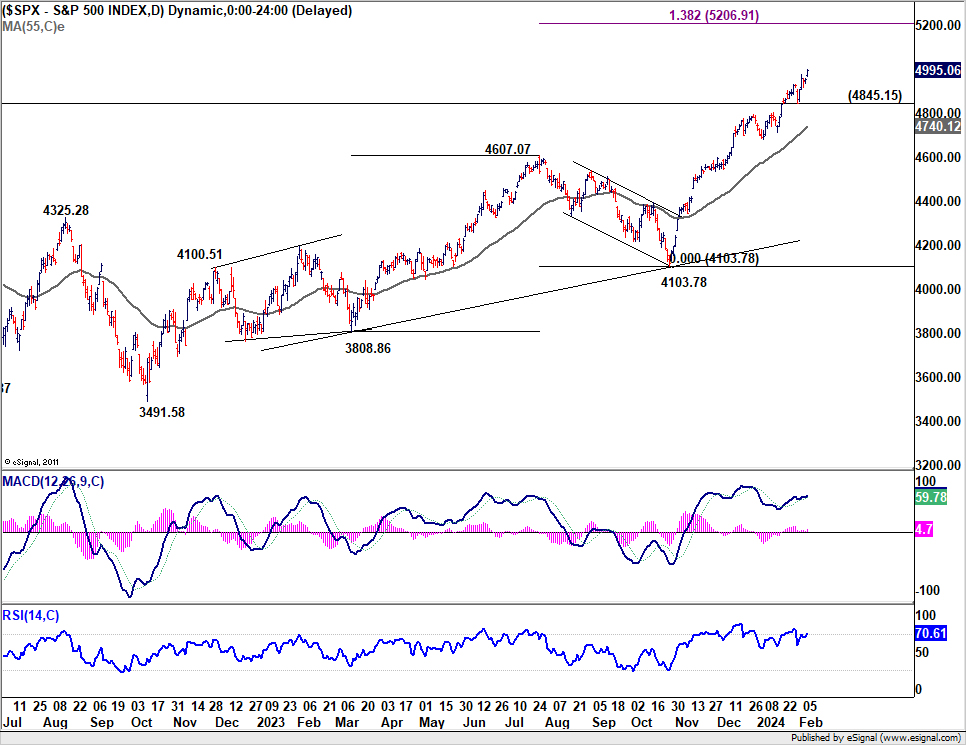

S&P 500 hit another record high overnight despite persistent comments from Fed officials advocating patience regarding rate cuts. Immediate focus will be on 5000 psychological level now. Sustained break there will pave the way to 138.2% projection of 3808.86 to 4607.07 from 4103.78 at 5206.91. In any case, near term outlook will stay bullish as long as 4845.15 support holds.

In Asia, Nikkei rose 2.15. Hong Kong HSI is down -1.16%. China Shanghai SSE is up 1.05%. Singapore Strait Times is down-0.21%. Japan 10-year JGB yield is down -0.0077 at 0.702. Overnight, DOW rose 0.40%. S&P 500 rose 0.82%. NASDAQ rose 0.95%. 10-year yield rose 0.020 to 0.411.

BoJ’s Uchida signals no swift hikes after negative rate ends

In a speech today, BoJ Deputy Governor Shinichi Uchida articulated a scenario where, despite an end to the negative interest rate policy, rapid interest rate hikes remain unlikely.

“Even if the Bank were to terminate the negative interest rate policy, it is hard to imagine a path in which it would then keep raising the interest rate rapidly,” he stated, suggesting a gradual adjustment process, while financial conditions wild remain “accommodative.

Uchida projected gradual increase in underlying inflation toward 2 percent target through fiscal 2025. This forecast anticipates core CPI (all items less fresh food) at 2.8% for fiscal 2023, with a subsequent moderation to 2.4% in fiscal 2024 and 1.8% in fiscal 2025.

Theses projections are based on the outlook that “while the pass-through of cost increases will continue to wane, prices such as of services will rise, accompanied by wage increases.”

To achieve this economic outlook, Uchida emphasized, the virtuous cycle needs to intensify in both directions, from prices to wages and from wages to prices.”

China’s deepening deflation: CPI hits 14-year low in Jan

China’s CPI took a notable dip in January, registering decrease of -0.8% yoy, marking a significant deepening of deflationary pressures from the previous month’s -0.3% and falling short of expectation -0.5% yoy. This downturn represents the fourth consecutive negative reading and the most substantial fall observed since 2009, over fourteen years ago.

The decline was particularly pronounced in food prices, which was down -5.9% yoy. Meanwhile, core CPI, which excludes volatile energy and food prices, rose by a modest 0.4% yoy, slowing from December’s 0.6% yoy increase. Despite the annual downturn, CPI saw a slight month-on-month increase of 0.3%, albeit below the anticipated 0.4% growth.

The NBS attributed January’s inflation figures to the high base effect associated with the Spring Festival, or Lunar New Year, which occurred in January the previous year. This annual holiday, which shifts between January and February depending on the lunar calendar, significantly impacts consumption patterns and inflation metrics due to its influence on consumer spending and business operations.

In parallel, PPI fell by -2.5% yoy in January, showing a modest improvement from the -2.7% yoy observed in the previous month and slightly better than -2.6% forecast. This marks the 16th consecutive month of annual declines for PPI, with factory-gate prices decreasing by -0.2% mom, following -0.3% mom drop in December.

Fed’s Kugler highlights inflation risks stemming from consumer behavior, job market, and global tensions

In a speech overnight, Fed Governor Adriana Kugler said she’s satisfied with the disinflationary progress, and expects it to “continue”. However, she was quick to temper this optimism with a note of caution, emphasizing that Fed’s work in combating inflation is far from over. The unpredictability of consumer behavior stands as a reminder of unforeseen developments to “slow progress on inflation.”

Kugler also pointed to the recent employment report, which showed unexpected strength. While a strong labor market is generally a positive sign, in the context of Fed’s efforts to cool inflation, such robustness could complicate the path to achieving a balanced demand-supply equation in both product and labor markets.

Fed Governor underscored the importance of monitoring geopolitical risks, particularly highlighting how the ongoing conflict in Ukraine and tensions in the Middle East could exacerbate inflationary pressures through “higher commodity prices” and global trade “disruptions”, “in turn pushing up goods inflation in the US”.

“At some point, the continued cooling of inflation and labor markets may make it appropriate to reduce the target range for the federal funds rate,” she noted. Conversely, “if progress on disinflation stalls, it may be appropriate to hold the target range steady at its current level for longer to ensure continued progress on our dual mandate.”

Fed’s Collins: Sustained, broadening inflation progress needed before methodical policy relaxation

Boston Fed President Susan Collins emphasized the need for “sustained, broadening signs of progress” in inflation reduction before contemplating any “methodical” adjustments to interest rate policy.

“As we gain more confidence in the economy achieving the Committee’s goals… I believe it will likely become appropriate to begin easing policy restraint later this year,” she stated in a speech overnight.

She advocates for a gradual approach to interest rate adjustments, allowing for “flexibility to manage risks, while promoting stable prices and maximum employment.”

Collins also highlighted the resilience of the US economy, as evidenced by recent GDP and labor market data, suggesting that the anticipated slowdown in economic activity “may take some time”.

“The path the economy takes toward the Fed’s mandated goals may continue to be bumpy and uneven, and we should not overreact to individual data points,” she advised.

A critical factor in Collins’s assessment is wage dynamics, with a specific interest in wage trends that align with long-term price stability. While acknowledging that not all economic indicators might perfectly converge, “seeing sustained, broadening signs of progress should provide the necessary confidence I would need to begin a methodical adjustment to our policy stance.”

Fed’s Barkin endorses patience regarding rate cuts

Richmond Fed President Thomas Barkin has voiced a call for patience concerning interest rate cuts, in the face of prevailing economic uncertainties.

“I am very supportive of being patient to get to where we need to get,” Barkin articulated during an event overnight.

Barkin highlighted the ongoing efforts to combat inflation, acknowledging that while progress has been made towards balancing the trade-offs between economic growth and inflation control, “a reasonable amount of uncertainty” remains.

He pointed out that the inflationary challenges are not confined to goods alone but extend to services and rental sectors.

“Declaring victory is very enticing, but you’re never going to hear me do that,” Barkin asserted.

BoC cites difficulty in predicting appropriate timing of rate cuts

BoC’s deliberations from the January meeting saw the governing council expressing that it was “difficult to foresee when it would be appropriate to begin cutting interest rates.”

The possibility of additional rate hikes was not dismissed, with members indicating that such measures could be warranted should new inflationary surprises emerge. However, the focus of future policy discussions would likely “shift to how much longer to maintain the policy rate at 5% to sustain the disinflationary process.”

Inflation’s persistent high levels and broad impact have prompted the council to emphasize their ongoing concerns regarding “persistence of underlying inflation” in their communications.

The members collectively agreed on the necessity for “further evidence of progress toward price stability,” seeking definitive signs of a downturn in core inflation rates.

To gauge the effectiveness of their monetary policy and the evolving economic landscape, the Governing Council plans to closely monitor core inflation alongside several critical indicators. These include the equilibrium between supply and demand within the economy, corporate pricing strategies, inflation expectations, and the ratio of wage growth to productivity.

Looking ahead

ECB monthly bulletin is the only feature in the European economic calendar. Later today, US will release jobless claims.

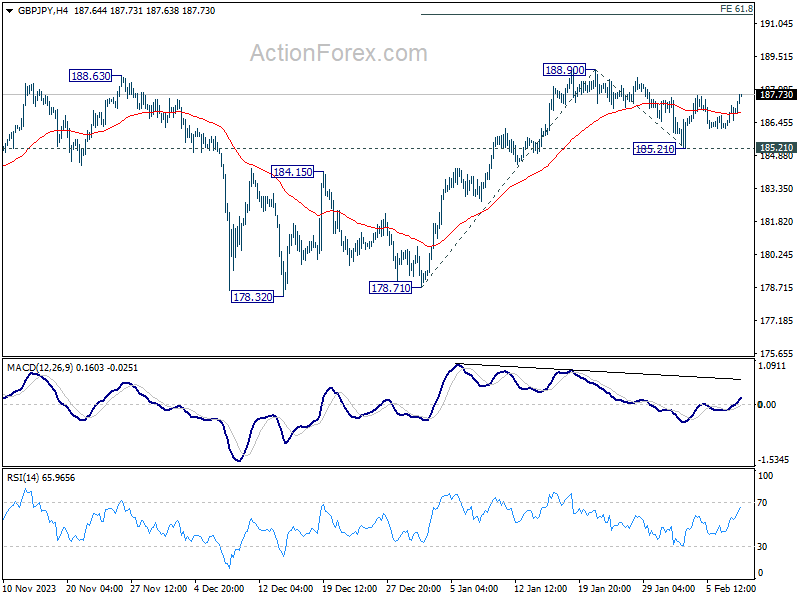

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.45; (P) 186.86; (R1) 187.53; More…

Intraday bias in GBP/JPY is back on the upside as rebound from 185.21 resumes. Further rise is expected to retest 188.90 resistance first. Firm break there will resume larger up trend. Next near term target will be 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50. For now, near term outlook will stay bullish as long as 185.21 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jan | 3.10% | 3.20% | 3.10% | 3.00% |

| 00:01 | GBP | RICS Housing Price Balance Jan | -18% | -28% | -30% | |

| 01:30 | CNY | CPI Y/Y Jan | -0.80% | -0.50% | -0.30% | |

| 01:30 | CNY | PPI Y/Y Jan | -2.50% | -2.60% | -2.70% | |

| 05:00 | JPY | Eco Watchers Survey: Current Jan | 50.2 | 50.3 | 50.7 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 13:30 | USD | Initial Jobless Claims (Feb 2) | 220K | 224K | ||

| 15:00 | USD | Wholesale Inventories Dec F | 0.40% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -73B | -197B |