Range trading continues in most major pairs and crosses for the week so far. Dollar’s selloff was relatively short-lived overnight, as US stocks retreated rather deeply after initial rally. There is sign of profit-taking in equities, which could curb any selling pressure in the greenback in the near term. However, Dollar’s next move remains contingent on the upcoming US GDP release today and PCE inflation tomorrow.

Today’s ECB rate decision and Germany’s Ifo Business Climate index are key focal points for Euro. While it’s improbable that the ECB will provide any concrete indications regarding the timing of rate adjustments, President Christine Lagarde’s commentary on Eurozone economy could be a game-changer. Any expressions of deep concern might spark renewed speculation about an imminent rate cut, potentially exerting further pressure on Euro, especially considering its relative weakness against Sterling and Swiss Franc.

Turning our gaze to Asia-Pacific, the ongoing rebound in Chinese and Hong Kong stock markets has yet to make a substantial impact on the currency markets. Australian Dollar is notably struggling to maintain momentum in its rebound, while New Zealand Dollar also appears to be under some strain. Following BoC decision to maintain its interest rate stance, Canadian Dollar is experiencing some bearish pressure. On the other hand, Japanese Yen stands out as one of the stronger performers this week. However, it’s important to note that Yen’s strength is more reflective of a consolidation phase in the aftermath of its recent downward trend, rather than a fundamental bullish shift.

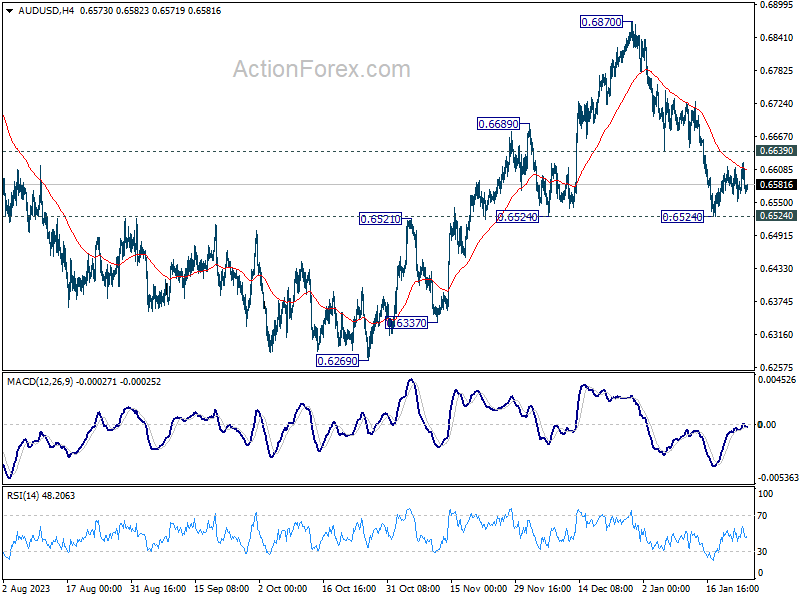

Technically, AUD/USD is worth a watch today after initial rejection by 55 4H EMA. Near term outlook stays bearish with 0.6639 minor resistance intact. Firm break of 0.6524 will resume the decline from 0.6870. That could also prompt downside acceleration back towards 0.6269 low. The next move in AUD/USD could depend on whether US stocks are turning into a corrective phase after recent record run.

In Asia, Nikkei closed up 0.03%. Hong Kong HSI is up 1.94%. China Shanghai SSE is up 2.76%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is up 0.0229 at 0.745. Overnight, DOW fell -0.26%. S&P 500 rose 0.08%. NASDAQ rose 0.36%. 10-year yield rose 0.036 to 4.178.

ECB to stand pat, await Lagarde’s take on rate cut and economic outlook

ECB is widely expected to keep monetary policy unchanged today. Main refinancing rate will be held at 4.50%, and deposit rate at 4.00%. Given the lack of significant new data since the December meeting, it’s improbable that ECB will offer fresh policy directions. Instead, it’s expected that the market will have to await March meeting, which will include new economic projections, for any substantial updates.

President Christine Lagarde is likely to continue her stance against the speculation of imminent rate cuts. It is anticipated that she will emphasize the persistence of underlying price pressures, especially in the services sector, and highlight the various risks still in play. These risks range from impending wage negotiations to geopolitical tensions, such as the ongoing Red Sea blockade.

However, the tone adopted by Lagarde regarding the Eurozone’s economic condition will be scrutinized closely. Recent economic data, including this week’s PMIs suggests that Eurozone might be already in a recession in the last quarter and is witnessing a sluggish start to the new year. Should President Lagarde express heightened concern over the economic situation, it could potentially trigger market participants to increase their bets on an earlier rate cut.

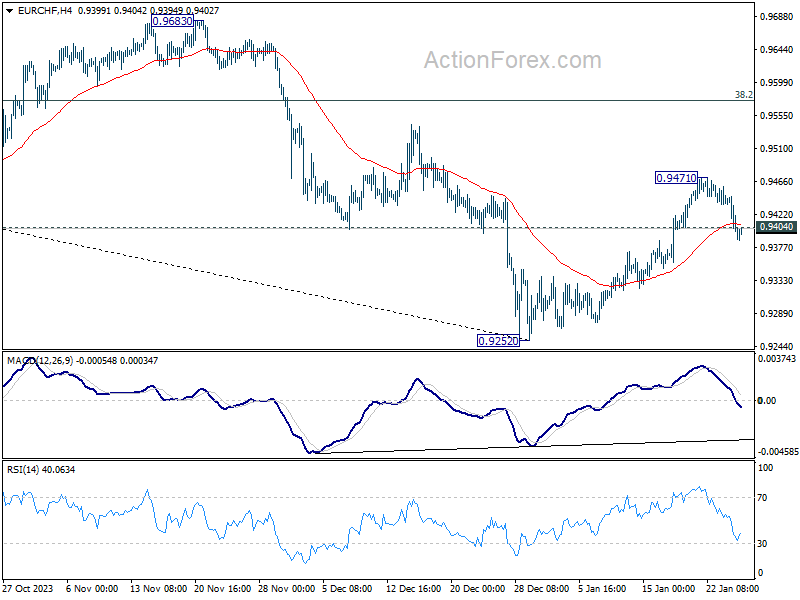

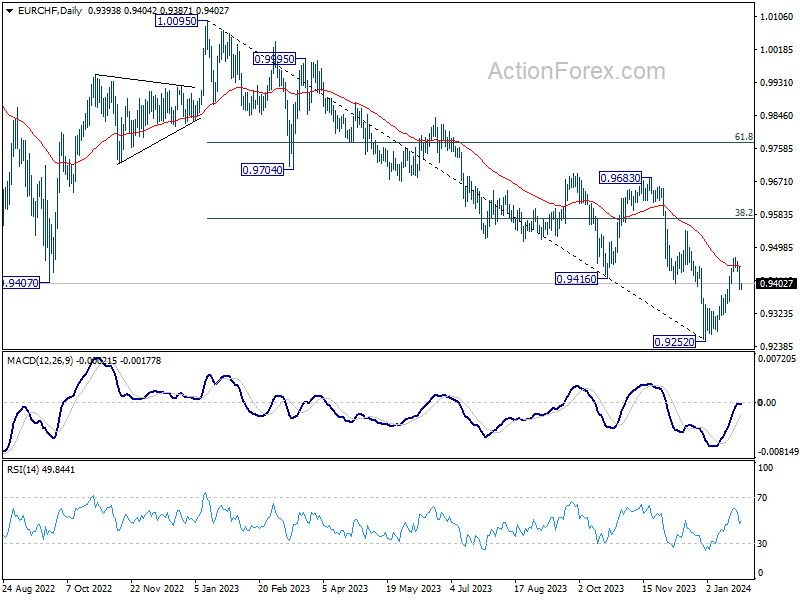

EUR/CHF’s deep retreat this week suggests initial rejection by 55 D EMA (now at 0.9447). Deeper pull back is now mildly in favor as long as 0.9471 holds, towards 0.9252 low. But a break there is not envisaged at this point. Meanwhile, break of 0.9471 will resume the rebound, as a correction to whole down trend from 1.0095, to 38.2% retracement of 1.0095 to 0.9252 at 0.9574.

US Q4 GDP in spotlight: A test for S&P 500 amid profit taking

Financial markets are also keenly focused on US GDP data today. Analysts expect GDP to grow at an annualized rate of 2.0% in Q4, marking a slowdown from the previous quarter’s 4.9%, and reaching the lowest rate since Q2 of 2022. This anticipated reading would align with the notion that the US economy, while experiencing a rapid cooling, remains resilient. A key component under scrutiny is the performance of consumption growth, which has been a significant support for the economy. Also to be featured from the US, durable goods orders, trade balance, jobless claims, and new home sales will be released.

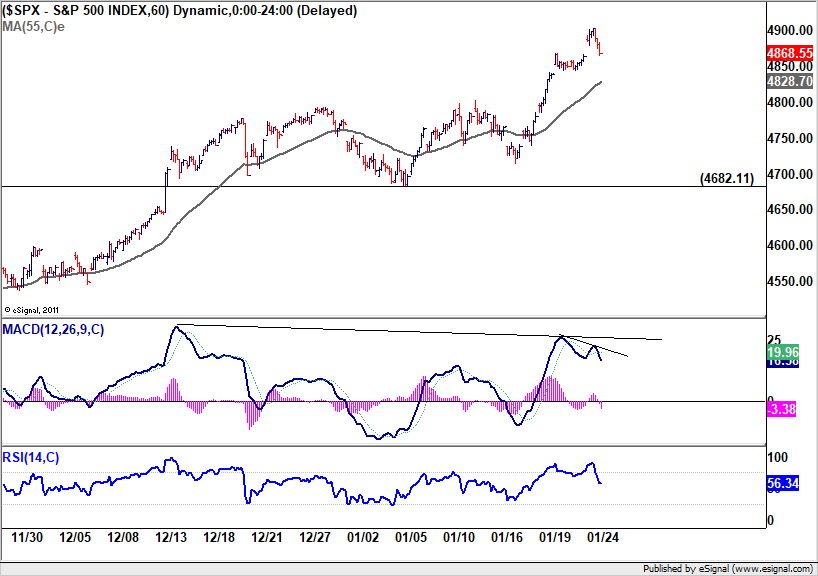

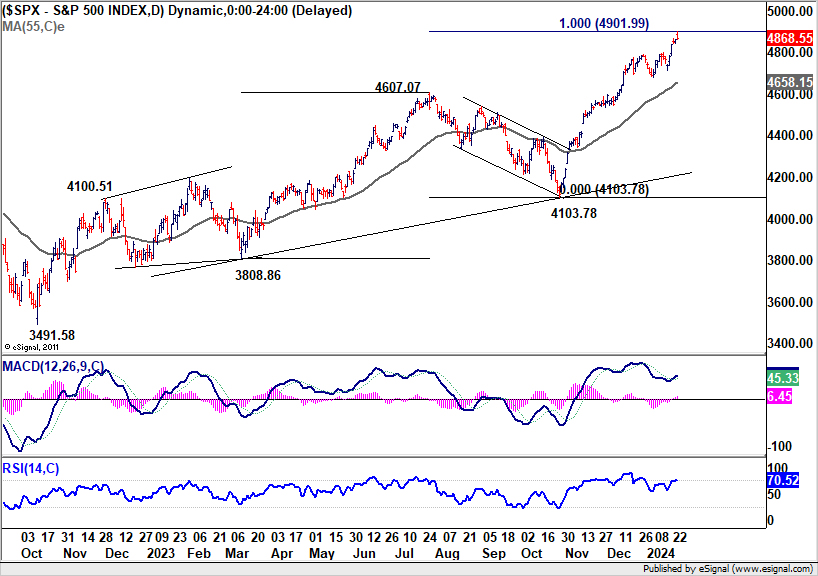

Notable profit taking was seen in the US stock markets after initial rally overnight. S&P 500 closed up just 0.08% at 4868.55, after climbing to 4903.68. Technically, there is prospect of a prolonged near-term consolidation given that SPX has just met 100% projection of 3808.86 to 4607.07 from 4103.78 at 4901.99.

Break of 55 H EMA (now at 4828.70) could trigger deeper correction towards 4682.11 support, which is slightly above 55 D EMA (now at 4658.15), and set the range for sideway consolidations.

Nevertheless, another rally, as supported by strong GDP data today, and sustained trading above 4901.99 would set the stage for a take on 5000 psychological level quickly.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3459; (P) 1.3494; (R1) 1.3558; More…

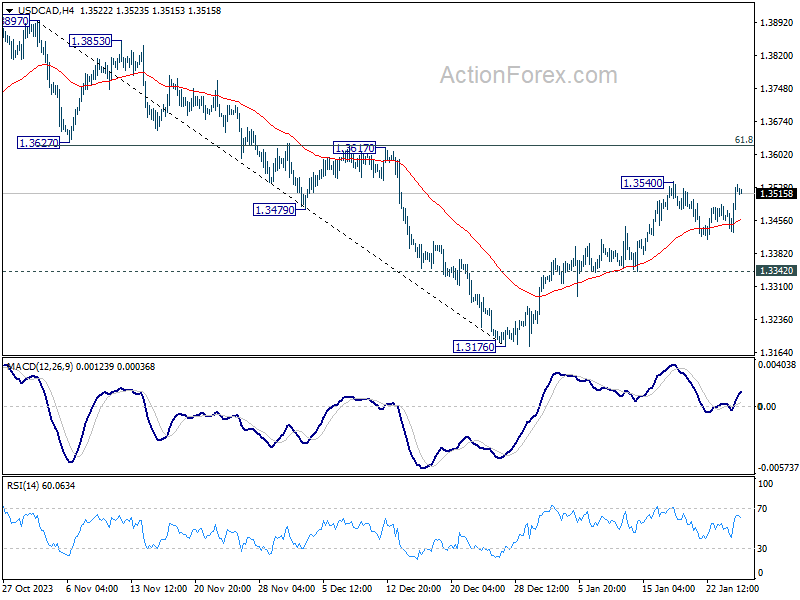

USD/CAD is staying below 1.3540 despite strong recovery overnight. Intraday bias remains neutral first and more consolidations could be seen. But further rally is expected as long as 1.3342 minor support holds. Fall from 1.3897 should have completed at 1.3716. Break of 1.3540w ill target 1.3617 cluster resistance (61.8% retracement of 1.3897 to 1.3176 at 1.3622). Decisive break there will pave the way to 1.3897/3976 key resistance zone.

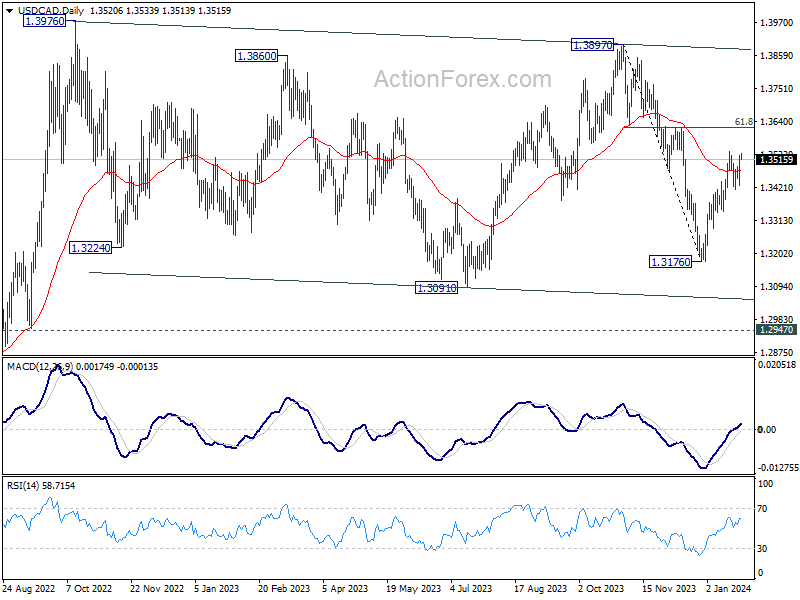

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Bulletin Q4 | ||||

| 09:00 | EUR | Germany IFO Business Climate Jan | 86.7 | 86.4 | ||

| 09:00 | EUR | Germany IFO Current Assessment Jan | 88.6 | 88.5 | ||

| 09:00 | EUR | Germany IFO Expectations Jan | 84.9 | 84.3 | ||

| 13:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 19) | 199K | 187K | ||

| 13:30 | USD | GDP Annualized Q4 P | 2.00% | 4.90% | ||

| 13:30 | USD | GDP Price Index Q4 P | 2.20% | 3.30% | ||

| 13:30 | USD | Goods Trade Balance (USD) Dec P | -88.7B | -90.3B | ||

| 13:30 | USD | Wholesale Inventories Dec P | -0.20% | -0.20% | ||

| 13:30 | USD | Durable Goods Orders Dec | 1.00% | 5.40% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Dec | 0.20% | 0.40% | ||

| 13:45 | EUR | ECB Press Conference | ||||

| 15:00 | USD | New Home Sales Dec | 646K | 590K | ||

| 15:30 | USD | Natural Gas Storage | -154B |