Yen’ decline resume today after release of Japan’s latest CPI data, which suggests that BoJ is not be under immediate pressure to exit its negative interest rate policy. . Economists have noted a crucial aspect of Japan’s inflation dynamics: while cost-push inflation is clearly easing, the transition to demand-pull inflation remains unconfirmed. The market’s attention is now turning to BoJ’s meeting next week, where new economic forecasts will be published. Although many analysts consider April as the most likely month for a rate hike, this remains contingent on the upcoming projections.

Amidst the Yen’s decline, USD/JPY is approaching 150 psychological level, prompting verbal interventions from Japanese financial authorities. Finance Minister Shunichi Suzuki reiterated the importance of stable currency movements that reflect economic fundamentals. He assured that the government would continue to closely monitor forex markets. However, these comments have not provided a sustainable boost to Yen.

For the week, Dollar remains the strongest performer, but its rally is pausing with the rebound in stocks overnight. However, there is no indication of a reversal in Dollar’s strength at this stage. Sterling and Euro are following as the second and third strongest currencies, respectively. Yen remains at the bottom of the performance chart, trailed by New Zealand Dollar and Swiss Franc. Australian Dollar is also showing softness, while Canadian Dollar displays mixed performance.

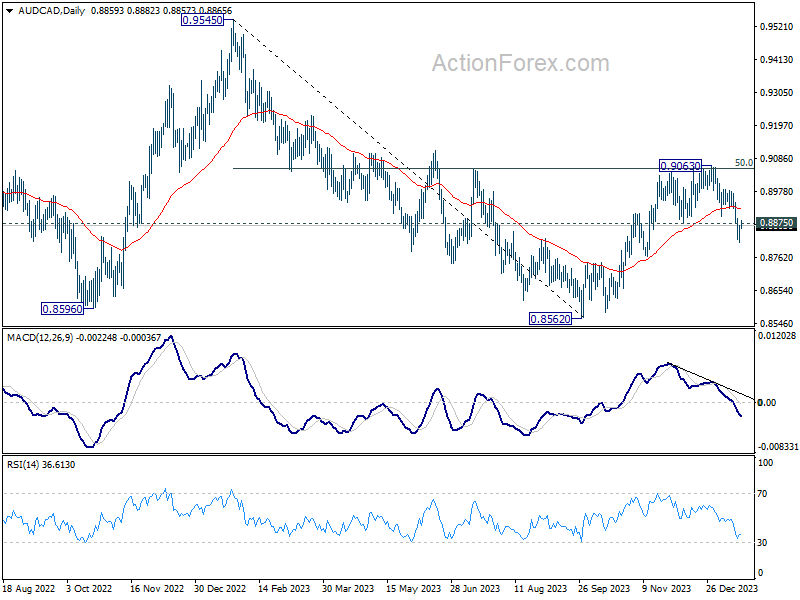

Technically, AUD/CAD’s break of 0.8875 support indicates that rebound from 0.8562 has completed at 0.9063, after hitting 50% retracement of 0.9545 to 0.8562 at 0.9054. Further decline is now expected as long as 55 D EMA (now at 0.8920) holds. Next target is a retest on 0.8562 low. It’s still a early to assess, but further downside acceleration would raise the chance of breaking through 0.8562 to resume larger down trend from 0.9991 (2021 high).

In Asia, at the time of writing, Nikkei is up 1.34%. Hong Kong HSI is down -0.66%. China Shanghai SSE is down -0.60%. Singapore Strait Times is up 0.31%. Japan 10-year JGB yield is up 0.0133 at 0.668. Overnight, DOW rose 0.54%. S&P 500 rose 0.88%. NASDAQ rose 1.35%. 10-year yield rose 0.038 to 4.144.

Fed’s Bostic foresees rate cuts in Q3, sets high bar for earlier action

Atlanta Fed Raphael Bostic said overnight that he now projects Fed to begin cutting interest rates in the third quarter of this year, a shift in timing from his previous expectation of the fourth quarter.

This adjustment is a response to the recent economic data, as he explained, “Because I’m data dependent, I have incorporated the unexpected progress on inflation and economic activity into my outlook, and thus moved up my projected time to begin normalizing the federal funds rate to the third quarter of this year from the fourth quarter.”

While Bostic does not entirely dismiss the possibility of an earlier rate cut, potentially as soon as July, he emphasizes that the criteria for such a decision would be stringent. “The bar will be high,” he stated, indicating that any move to cut rates before the third quarter would require substantial and convincing evidence.

He elaborated on this point, saying, “If we continue to see a further accumulation of downside surprises in the data, it’s possible for me to get comfortable enough to advocate normalization sooner than the third quarter.” However, he stresses that the evidence supporting such a decision would need to be compelling.

Japan’s CPI core dips to 2.3%, remains above BoJ’s target for 21st month

Japan’s CPI core, excluding fresh food, decelerated slightly in December, moving from 2.5% yoy to 2.3% yoy, aligning with market expectations. This slowdown brings core inflation rate to its lowest since June 2022, yet it notably remains above BoJ’s 2% target for the 21st consecutive month.

Overall headline CPI also showed a slowdown, decreasing from 2.8% yoy to 2.6% yoy. Additionally, CPI core-core, which excludes both food and energy, saw a modest decline, moving from 3.8% yoy to 3.7% yoy.

A notable aspect of CPI data is the stability of services prices, which rose by 2.3% yoy, maintaining the pace from the previous month. This rate marks the fastest increase in services prices in three decades when periods affected by sales tax hikes are excluded.

A significant factor contributing to the slowdown in inflation was the substantial drop in energy prices, which decreased by -11.6% yoy. This decline was driven by reductions in electricity and city gas prices, which fell by -20.5% yoy and -20.6% yoy, respectively, largely due to government subsidies.

NZ BNZ manufacturing falls to 43.1, 10th month of contraction

New Zealand’s BusinessNZ Performance of Manufacturing Index fell from 46.5 to 43.1 in December. This latest figure marks a continued contraction in the manufacturing sector, which has now been shrinking for ten consecutive months.

The index components reveal a widespread decline across various manufacturing activities. Production fell from 43.5 to 40.5. Employment decreased from 47.9 to 46.7. New orders dropped from 47.4 to 44.0. Similarly, finished stocks and deliveries both saw declines, from 50.4 to 45.9 and 47.8 to 43.4, respectively.

Manufacturers’ feedback further underscored the industry’s challenges, with 61% of the comments in December being negative. This is a slight increase from 58.7% in November, though an improvement from 65.1% in October. The predominant concerns revolved around a lack of demand and sales, which have been significant hurdles for many manufacturers.

Stephen Toplis, BNZ’s Head of Research, echoed these sentiments in his assessment of the PMI data. “The December PMI reaffirms our view that economic conditions remain very difficult,” he stated. Toplis anticipates that while the economy and the manufacturing sector might gain some momentum by the end of 2024, the immediate future appears challenging, particularly with pressures in retail spending and construction activity.

Looking ahead

UK retail sales and German PPI will be released in European session. Later in the day, Canada will publish retail sales. US will release existing home sales and U of Michigan consumer sentiment.

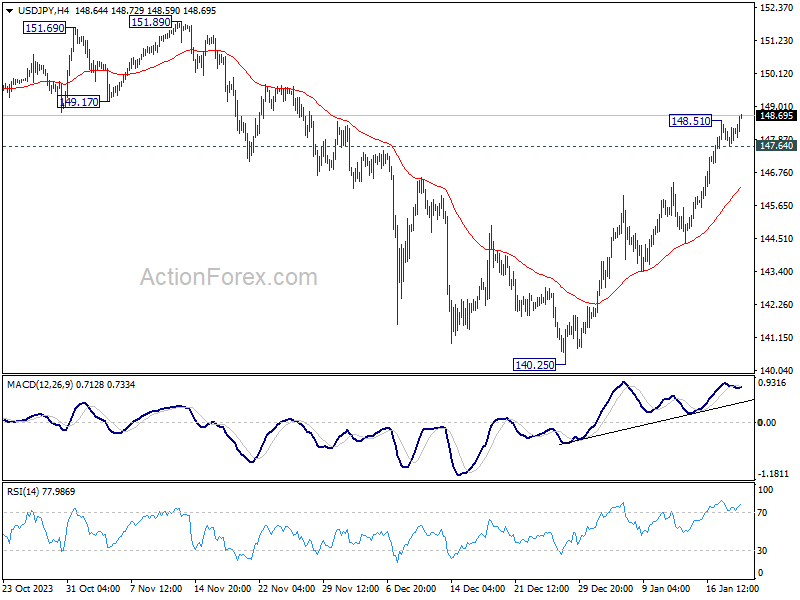

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.78; (P) 148.05; (R1) 148.44; More…

USD/JPY’s rally resumed after brief retreat and intraday bias is back on the upside. Current rise from 140.25 should target a retest on 151.89/93 key resistance zone. On the downside, below 147.64 minor support will turn intraday bias neutral again and bring consolidations, before staging another rise.

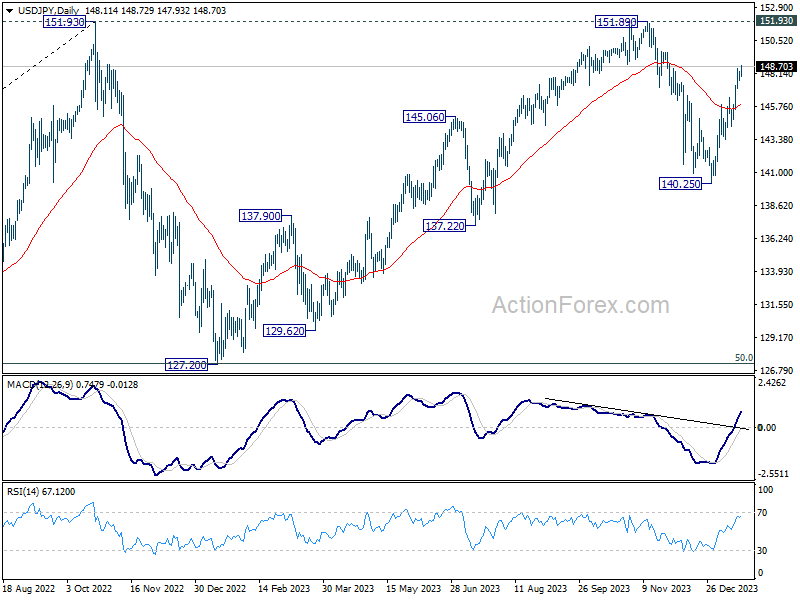

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Dec | 43.1 | 46.7 | 46.5 | |

| 23:30 | JPY | National CPI Y/Y Dec | 2.60% | 2.80% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Dec | 2.30% | 2.30% | 2.50% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Dec | 3.70% | 3.80% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Nov | -0.70% | 0.20% | -0.80% | -0.20% |

| 07:00 | GBP | Retail Sales M/M Dec | -0.50% | 1.30% | ||

| 07:00 | EUR | Germany PPI M/M Dec | -0.50% | -0.50% | ||

| 07:00 | EUR | Germany PPI Y/Y Dec | -7.90% | -7.90% | ||

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.60% | -0.90% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | -1.30% | |||

| 13:30 | CAD | Retail Sales M/M Nov | 0.00% | 0.70% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | -0.10% | 0.60% | ||

| 15:00 | USD | Existing Home Sales Dec | 3.82M | 3.82M | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 69.6 | 69.7 |