The forex markets commenced the week on a relatively quiet note, despite generally positive risk sentiment. This was highlighted by Japan’s Nikkei, which continued its impressive performance, breaking above 35k mark to reach new three-decade highs. The robust momentum could continue until the eagerly awaited BoJ meeting later in the month, where fresh economic forecasts are set to be revealed.

On the other hand, stocks in China and Hong Kong, meanwhile, presented a picture of stability, seemingly unaffected by PBoC’s decision to keep the key policy interest rate unchanged. This decision, while unexpected, did not cause significant ripples in the markets, possibly due to a wait-and-see approach among investors in these regions.

Currency markets, meanwhile, displayed a notable lack of dynamism. Major currency pairs and crosses were largely confined within the trading ranges established last Friday. Within this context, Sterling stands out as the month’s strongest performer so far, a position followed by Dollar and then Euro. Conversely, Japanese Yen finds itself at the bottom of the performance ladder, with Australian and New Zealand Dollars also underperforming. Swiss Franc and Canadian Dollar are positioned in the middle.

Subdued trading atmosphere is likely to persist through the day, with stock and bond markets closed for Martin Luther King Day. Eurozone’s industrial production and trade balance, alongside Canada’s manufacturing sales figures, are the main featured which might not trigger much reactions. Nevertheless, the week promises to ramp up in volatility with a barrage of crucial economic data scheduled for release, spanning all major currencies. This includes impactful releases from US, UK, Canada, Australia, Japan, and China.

Technically, Copper is worth a watch in the coming days. As fall from 3.9346 extends, immediate focus is now on 3.6833 support. Decisive break there will confirm that whole rebound from 3.5021 has completed at 3.9436. Deeper fall would be seen back to retest 3.5021, even if it’s just in sideway consolidation. This development, if realized, could drag AUD/USD through 0.6639 support.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is down -0.10%. China Shanghai SSE is up 0.19%> Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is down -0.0285 at 0.562.

ECB’s Lane: Wage increases as determinants for rate cut timing and extent

In an interview with Corriere della Sera, ECB Chief Economist Philip Lane acknowledged that the December inflation data was “broadly in line with our projections”. He highlighted a “continued progress” in easing of core inflation, yet pointed out existing “headwinds to services inflation.”

A critical point raised by Lane concerns wage growth, which he notes is still rising well above any kind of long-run equilibrium rate”. ECB is expecting “high wage increases” to continue in 2024. “the scale of that will determine the timing and the scale of rate adjustment this year,” he added.

Lane also touched upon ECB’s reliance on data. He mentioned that while new wage data is received weekly, the “most complete dataset” from Eurostat’s national accounts will only be available at the end of April.

This timeline suggests that key policy decisions, especially those pertaining to rate cuts, are likely to be heavily influenced by data available by June meeting.

Finally, Lane’s projection of a “significant recovery” in the European economy this year is tempered with caution, as he acknowledges downside risks to their forecasts. The question of whether 2024 will see a recovery or a continuation of the stagnation experienced in 2023 remains a “big data question” for ECB.

Contrary to market expectations, PBoC maintains MLF rate but increases liquidity

Despite the anticipation of a rate cut to bolster the weakening economy, currently grappling with deflation for the past three months, PBoC held firm, keeping the rate on CNY 995B worth of one-year medium-term lending facility loans steady at 2.50%. This decision defied the general expectation of a 0.1% cut to 2.40%.

Opting not to alter the policy rate, the central bank instead chose to enhance liquidity in the banking system. This is seen from the net injection of CNY 216B of fresh funds, following the expiration of CNY 779B worth of MLF loans this month. Moreover, PBoC also infused CNY 89B yuan through seven-day reverse repos, maintaining a stable borrowing cost at 1.80%.

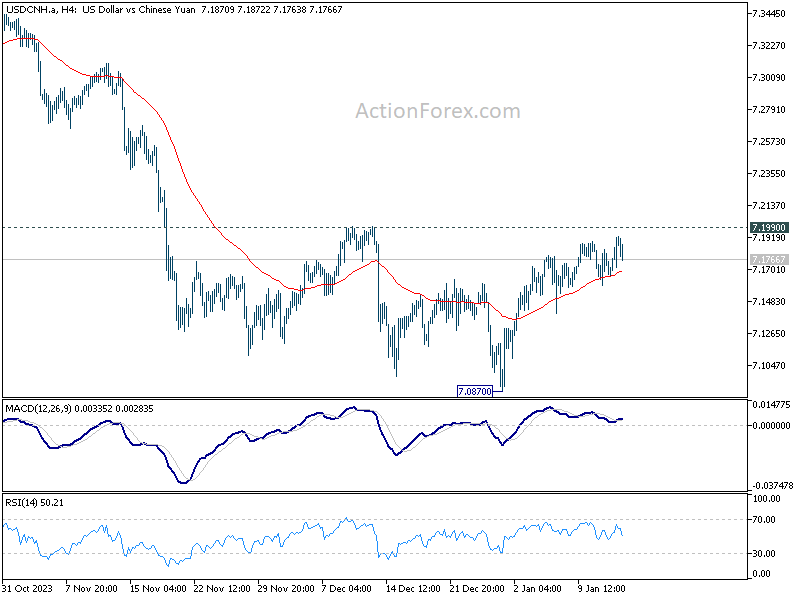

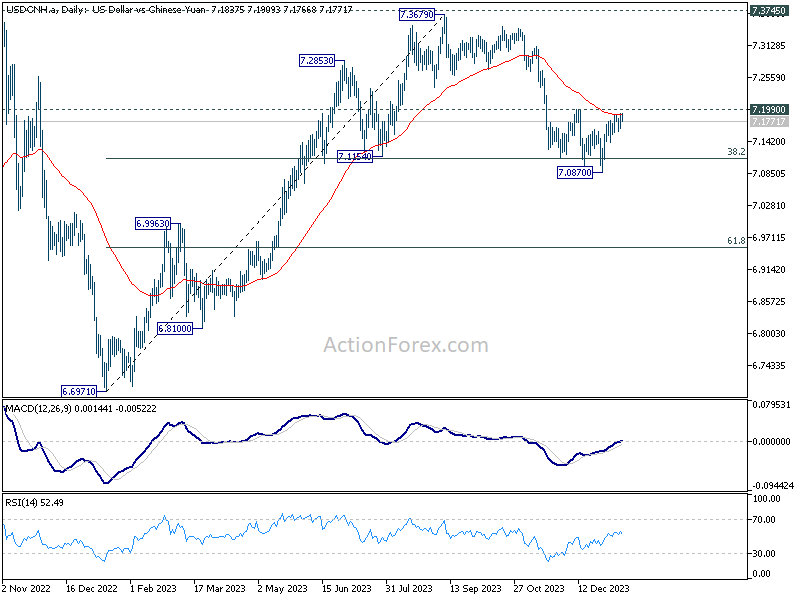

There is little reaction from USD/CNH to PBoC’s announcement. Technically, USD/CNH is now at a critical juncture, pressing 55 D EMA, just ahead of 7.199 near term resistance. Near term outlook is staying bearish. Another decline and break of 7.0870 short term bottoming will resume the whole fall from 7.3679 to 61.8% retracement of 6.6971 to 7.3679 at 6.9533.

However, firm break of 7.1990 will argue that the fall from 7.3679 has completed and turn near term outlook bullish for retesting this high.

A hectic week Ahead: Gauging the path of global monetary easing through key economic data

A plethora of crucial economic data sets the stage for volatility in the currency markets this week. The dataset encompasses a wide range from inflation, retail sales, employment, to investor confidence across majorly traded currencies. The pivotal question at this juncture is identifying which data could potentially be the most influential in swaying currency movements.

The year 2024 has unmistakably been earmarked as a period of interest rate reductions, with the exception of BoJ. The primary uncertainties lie in pinpointing the exact timing of the initial rate cut and the subsequent velocity of monetary policy relaxation. Current market pricing appears quite assertive, predicting up to six rate cuts by both Fed and ECB, and five cuts each by BoE and the BoC. This aggressive market stance argues that traders are bracing for potential major economic or financial shocks globally this year.

In a scenario devoid of significant shocks, the response of various currencies to economic data releases is likely to hinge on the particular phase of the disinflation cycle each region is experiencing. For US, Eurozone, and Canada, where substantial disinflationary progress has been made, any data underscoring growth shortfalls could incite speculations of earlier and more rapid policy easing. Conversely, in UK and Australia, where inflation levels remain elevated, surprises on the higher end of inflation data could limit the scope for BoE and RBA in implementing rate cuts.

Hence, the spotlight could be marginally more focused on a few key data points: US retail sales, UK CPI and wage growth figures, Canadian retail sales, and Australian employment. Additionally, Japan’s CPI and China’s GDP might also contribute to market volatility. In terms of central bank activities, both Fed’s Beige Book and meeting accounts from ECB are not anticipated to offer any significant revelations that are not already factored into market expectations.

Here are some highlights for the week:

- Monday: Eurozone industrial production, trade balance; Canada manufacturing sales, wholesale sales, BoC business outlook survey.

- Tuesday; New Zealand NZIER business confidence; Australia Westpac consumer confidence; Japan PPI; Germany CPI final, ZEW economic sentiment; UK employment; Canada CPI, housing starts; US Empire state manufacturing.

- Wednesday: China GDP, industrial production, retail sales, fixed asset investment; UK CPI, PPI; Eurozone CPI final; Canada IPPI and RMPI; US retail sales, import prices, industrial production,business inventories, NAHB housing index, Fed’s Beige Book.

- Thursday: Japan machine orders; Australia employment; ECB meeting accounts; US jobless claims, housing starts and building permits, Philly Fed survey.

- Friday: New Zealand BusinessNZ manufacturing; Japan CPI, tertiary industry index; Germany PPI, UK retail sales; Swiss PPI; Canada retail sales; US U of Michigan consumer sentiment, existing home sales

EUR/USD Daily Outlook

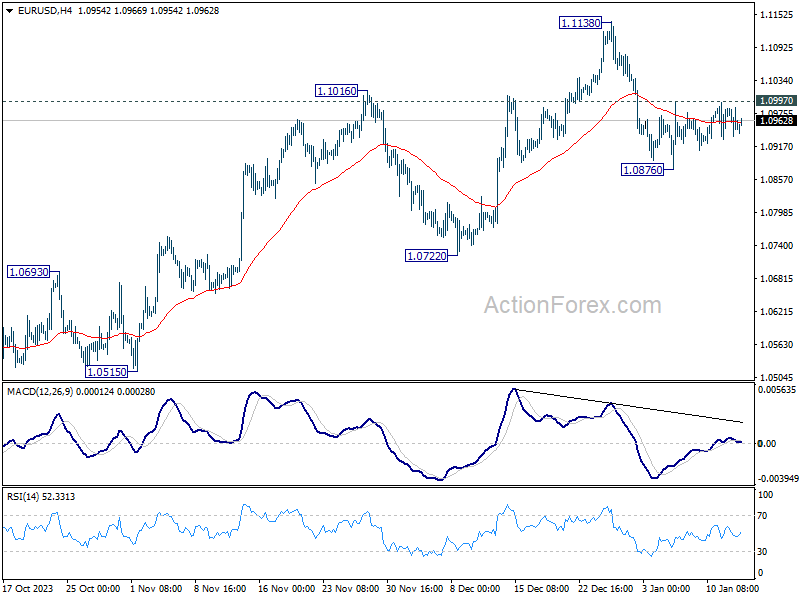

Daily Pivots: (S1) 1.0929; (P) 1.0958; (R1) 1.0980; More…

EUR/USD is still bounded in range trading and intraday bias remains neutral. Further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

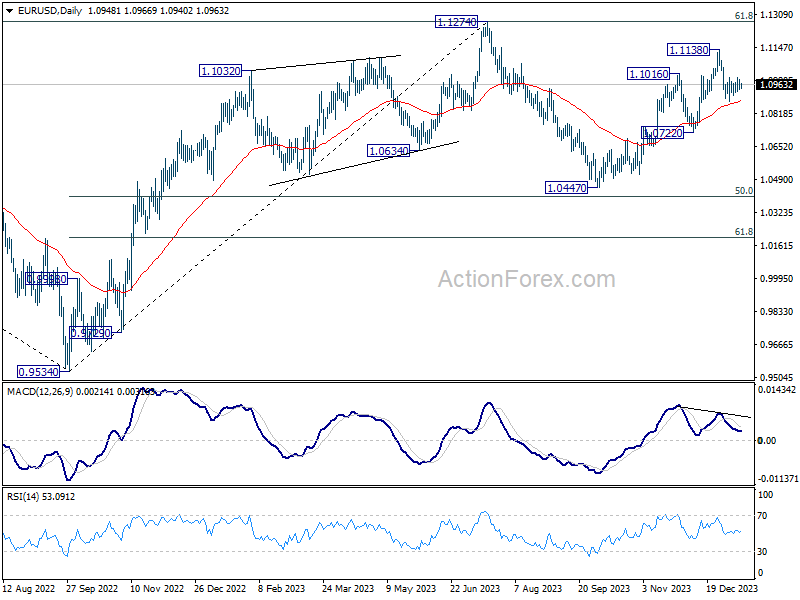

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 2.30% | 2.20% | 2.30% | |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 1.00% | 0.30% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Dec | -15.50% | -13.60% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | -0.30% | -0.70% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 11.2B | 10.9B | ||

| 13:30 | CAD | Manufacturing Sales M/M Nov | 0.90% |

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!) RULE-BASED Pocket Option Strategy That Actually Works | Live Trading

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading