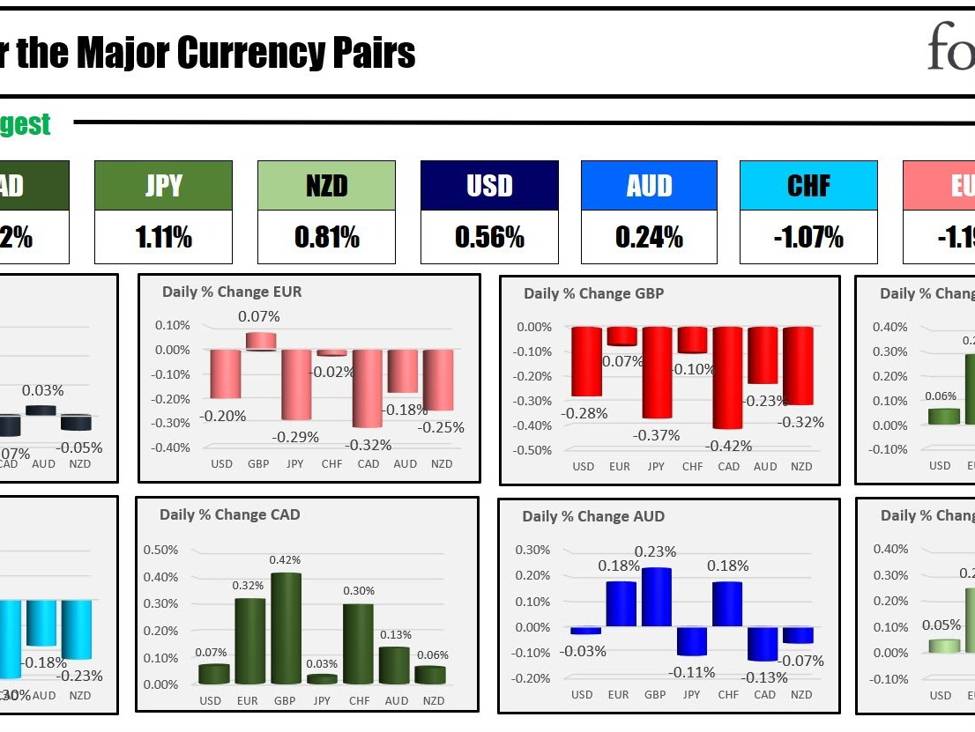

The strongest to the weakest of the major currencies

As the North American session begins, the CAD strongest and the GBP is the weakest. The USD is mixed to higher with gains versus the EUR, GBP and CHF and modest declines versus the JPY, CAD, and NZD.

Overnight in geopolitical news, the US and UK conducted airstrikes against Houthi rebel targets in Yemen. The military actions were a response to the Houthi rebels’ attacks on ships in the Red Sea since November. As per expectations, the Houthi deputy foreign minister warned that the US and UK will “pay a heavy price” for what they describe as “blatant aggression.” Both Iran’s foreign ministry and the Iran-backed Lebanese armed group Hezbollah have condemned the airstrikes. The Houthis have said they will continue targeting Israel-linked ships in the Red Sea. President Biden hinted at the possibility of additional measures to protect international commerce and US interests. The news has led to a spike in oil prices today with crude oil up over 3.5%.

Spot trading in Bitcoin ETFs started yesterday and was met with strong demand from investors. Grayscale, Blackrock and Fidelity offerings dominated the volume race. It is estimated that over $4 billion worth of transactions occurred. Morning morning

The earnings season begins in earnest today with the traditional release of some of the major financial institutions (along with a few others). Below are the results of the major company releases so far (along with whether the beat, missed or met expectations). Citicorp will announce at 8 AM ET.

-

JPMorgan Chase & Co (JPM) Q4 2023

- EPS: 3.97 (Beat; Expected: 3.36)

- Revenue: 39.94 billion (Beat; Expected: 39.78 billion)

-

Wells Fargo & Co (WFC) Q4 2023

- EPS: 0.86 (Miss; Expected: 1.17)

- Revenue: 20.48 billion (Beat; Expected: 20.3 billion)

-

Bank of America Corp (BAC) Q4 2023

- EPS: 0.70 (Beat; Expected: 0.68)

- Revenue: 22.0 billion (Miss; Expected: 23.74 billion)

-

Bank of New York Mellon Corp (BK) Q4 2023

- EPS: 1.28 (Beat; Expected: 1.13)

- Revenue: 4.31 billion (Beat; Expected: 4.29 billion)

-

Delta Air Lines Inc (DAL) Q4 2023

- EPS: 1.28 (Beat; Expected: 1.17)

- Revenue: 14.22 billion (Beat; Expected: 13.52 billion)

-

BlackRock Inc (BLK) Q4 2023

- EPS: 9.66 (Beat; Expected: 8.84)

- Revenue: 4.63 billion (Met; Expected: 4.63 billion)

-

UnitedHealth Group Inc (UNH) Q4 2023

- EPS: 6.16 (Beat; Expected: 5.98)

- Revenue: 94.4 billion (Beat; Expected: 92.14 billion)

And just released:

Citigroup Inc (C) Q4 2023

- Adjusted EPS: 0.84 (Beat; Expected: 0.75)

- Revenue: 17.4 billion (Miss; Expected: 18.74 billion)

US PPI will be released at 8:30 AM ET with expectations showing:

- PPI Final demand 1.3% versus 1.9% last month

- PPI final demand MoM 0.1% versus 0.0% last month

- Ex Food and Energy YoY, 1.9% versus 2.0% last month

- Ex Food and Energy MoM, your .2% versus 0.0% last month

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading up $2.70 or 3.76% at $74.73. At this time yesterday, the price was at $72.83

- Gold is trading up $20.25 or 0.99% at $2049.09. At this time yesterday, it was trading at $2032.89

- Silver is trading up $0.30 or 1.32% to $23.04. At this time yesterday, it was trading at $23.04

- Bitcoin traded at $45,731. At this time yesterday, the price was trading at $47,448

In the premarket for US stocks, the major indices are trading lower. The Nasdaq index eked out a tiny gain yesterday for its 5th consecutive up day. That streak is in jeopardy today, however:

- Dow Industrial Average futures are implying a decline of 155.02 points. Yesterday, the index rose 15.29 points or 0.04%

- S&P futures are implying a decline of -10.74 point. Yesterday, the index -3.23 points or -0.07%

- Nasdaq futures are implying a decline of -48.15 points. Yesterday, the index rose 0.54 points or 0.00%

In the European equity markets, the major indices are all trading higher:

- German DAX, +0.57%. Yesterday, the index fell -0.86%

- France CAC +0.75%. Yesterday, the index fell -0.52%

- UK FTSE 100 +0.68%. Yesterday, the index fell -0.90%

- Spain’s Ibex +0.62%. Yesterday, the index fell -0.62%

- Italy’s FTSE MIB +0.61% (delayed by 10 minutes). Yesterday the index fell -0.66%

Shares in the Asian Pacific markets were mostly lower with the exception of the Japan’s Nikkei 225 index which made a new 34 year high and closed sharply higher in the week.

- Japan’s Nikkei 225, +1.50%. For the trading week, the index closed at 34 year highs androse 6.59%

- China’s Shanghai composite index , -0.16%, For the week, the index built -1.61%

- Hong Kong’s Hang Seng index, -0.35%. For the week, the index fell -1.76%

- Australia S&P/ASX,-0,10%, For the week, the index rose 0.10%

Looking at the US debt market, yields are trading higher. Yesterday the yield curve steepened (although still negative). The 2– 30 year spread is up to -6.0 basis points from -17 basis points yesterday and getting new near parity. A 2– 10 year spread is also more positive (although still negative) that -26.9 basis points versus -34.9 basis points at the start of trading yesterday.

- 2-year yield 4.268% +0.8 basis points. Yesterday at this time, the yield was at 4.337%

- 5-year yield 3.910% +2.0 basis points.. Yesterday at this time, the yield was at 3.933%

- 10-year yield 3.997% +2.3 basis points.. Yesterday at this time, the yield was at 3.988%

- 30-year yield 4.207% +2.7 basis points. Yesterday at this time, the yield was at 4.168%

- The 2-10 year spread is at -26.9 basis points. At this time yesterday, the spread was at -34.9 basis points

- The 2-30 year spread is at -6.0 basis points. At this time yesterday, the spread was at -17.0 basis points

In the European debt market, the benchmark 10-year yields are lower:

Europe 10 year yields are lower

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)