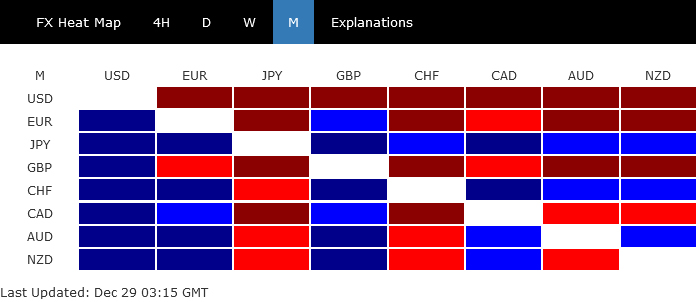

Trading activity is rather subdued in the last Asian session of the year. With no major economic events on the calendar for the day, trading is expected to remain quiet. Dollar is making an attempt to recover but continues to be the weakest performer for the week. It is followed by Euro and Sterling in terms of weak performance. Conversely, Swiss Franc and Japanese Yen are standing out as the strongest currencies. Australian Dollar and New Zealand Dollar are showing slight strength, while Canadian Dollar is leaning towards the weaker side.

From a technical analysis perspective, a key focus as we enter 2024 is the trajectory of Bitcoin. The primary question is whether Bitcoin will resume its medium-term upward trend towards 50k handle. Consolidation from 44,727 appears to be near completion. Break of 44727 will target 161.8% projection of 15452 to 31815 from 24896 at 51371. However, break of 40145 support will dampen this immediate bullish view, and bring deeper correction first.

In Asia, Nikkei closed down -0.51%. Hong Kong HSI is down -0.04%. China Shanghai SSE is up 0.48%. Singapore Strait Times is up 0.92%. Japan 10-year JGB yield rose 0.0234 at 0.616. Overnight, DOW rose 0.14%. S&P 500 rose 0.04%. NASDAQ fell -0.03%. 10-year yield rose 0.061 to 3.850.

Happy New Year to our readers. We’ll be back on January 2.

Dollar marks December as worst performer, market foresees 88% chance of March Fed rate cut

As December 2023 concludes, Dollar is set to be the month’s weakest performer. The persistent selloff can be largely attributed to Fed’s signal of the possibility of implementing rate cuts totaling 75 basis points in the coming year, as seen in latest economic projections. This unexpected pivot towards more accommodative monetary policy had a ripple effect across financial markets, notably propelling DOW to record highs and bringing S&P 500 close to its peak levels.

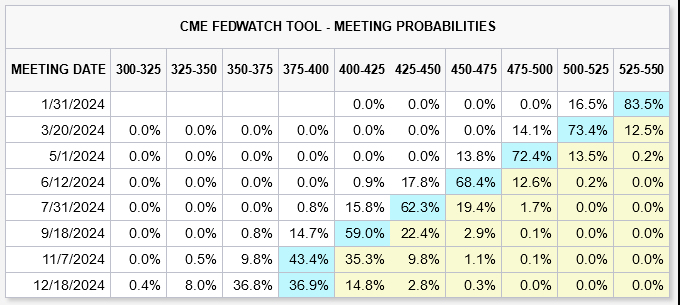

The market’s response to Fed’s policy shift has been markedly aggressive. Traders have priced in an 88% probability of a 25bps cut as soon as March. Looking ahead to the entirety of 2024, there’s a strong consensus, with over an 80% chance, that federal funds rate could decrease to a range of 3.75-4.00%, a notable drop from the current rate of 5.25-5.50%. The underlying rationale for such aggressive market expectations centers around the anticipation of recession in the US next year, a scenario that some analysts believe is increasingly likely.

However, it is important to note that Fed is not alone. ECB and BoE are also expected by the markets to commence rate cuts at some point in the next year. Officials from both these institutions continue to resist these market expectations, but their efforts have fallen into deaf ears. Sterling and Euro have emerged as the second and third weakest currencies, respectively, for December.

Yen dominates December as best performer on BoJ expectations

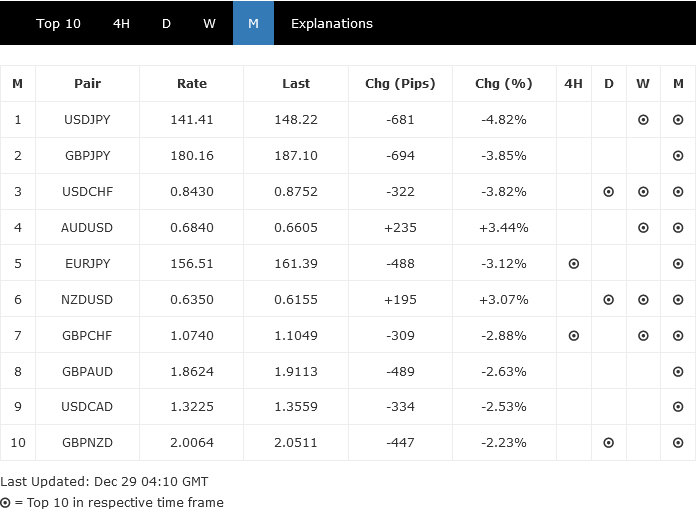

Japanese Yen is poised to be December’s best performer in the currency markets. Its strength is primarily driven by growing expectations that BoJ will eventually exit its long-standing negative interest rate policy in 2024. Yen’s performance is particularly noteworthy against Dollar (USD/JPY) and Sterling (GBP/JPY), both of which are top movers for the month, with the possibility of ending down more than 700 pips.

The strengthening of Yen comes amidst a broader context where other major global central banks, such as Fed, ECB, and BoE, are expected to start loosening their monetary policies or, in some cases like SNB, BoC and RBNZ, maintain unchanged rates.

BoJ Governor Kazuo Ueda has recently softened his typically dovish tone, acknowledging that the likelihood of a rate hike in 2024 is “not zero.” He also emphasized the importance of the Spring wage negotiations and the need for wage hikes to “broaden” from large companies to small businesses. This change in stance has contributed further to Yen’s rally, with April being viewed as a probable timing for rate hike. Yen could see further gains if incoming information in Q1 solidifies this expectation.

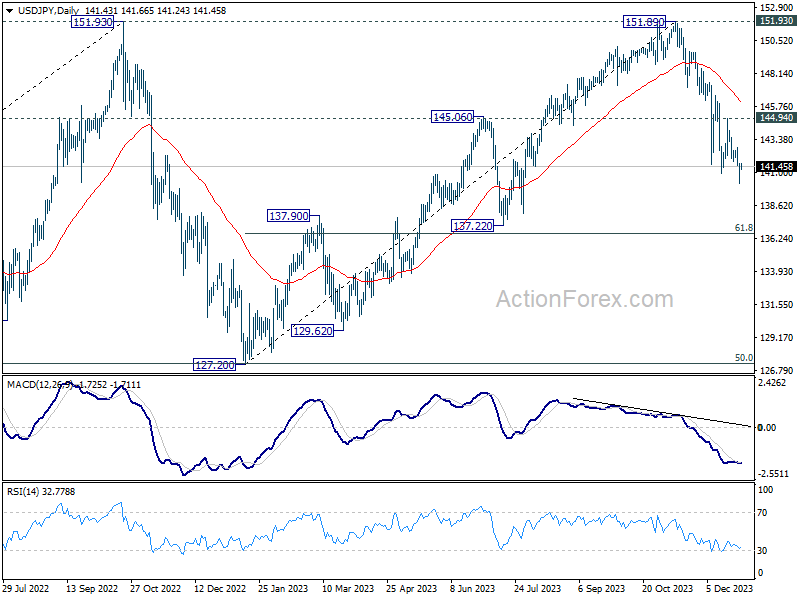

Technically, USD/JPY’s fall from 151.89 is seen as the third leg of the consolidation pattern from 151.93. Further decline is expected as long as 144.94 resistance holds. Next target is 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low).

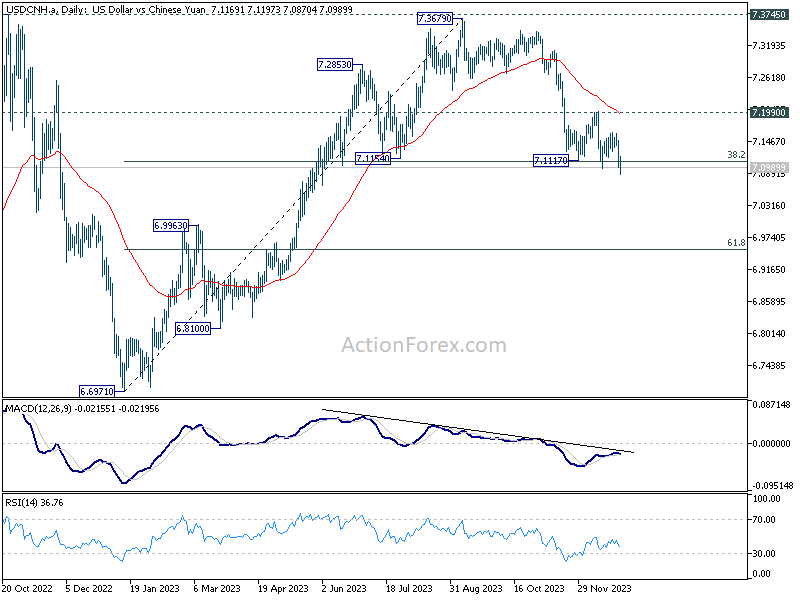

At the same time, USD/CNH is undergoing similar development. The pair is having a second attempt to break through 38.2% retracement of 6.6971 to 7.3679 at 7.1117. Sustained trading below this level will strengthen the case that fall from 7.3679 is the third leg of the consolidation pattern from 7.3745, aligning with the outlook of USD/JPY. In this case, deeper fall would be seen to 61.8% retracement at 6.9533, with prospect of having a take on 6.6971 support.

Looking ahead

Swiss KOF economic barometer and US Chicago PMI are the only features today.

AUD/USD Daily Report

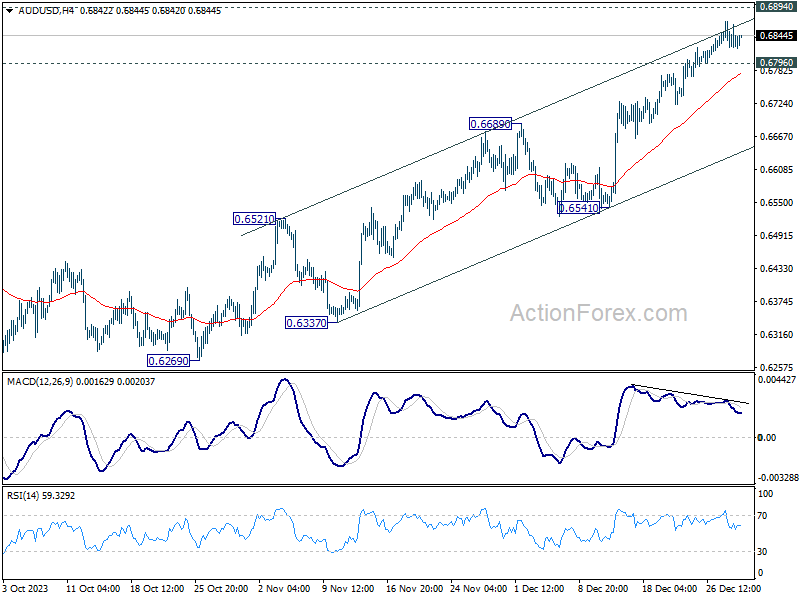

Daily Pivots: (S1) 0.6812; (P) 0.6841; (R1) 0.6859; More…

AUD/USD continues to lose upside momentum ahead of 0.6894 resistance and intraday bias is turned neutral first. On the upside, decisive break of 0.6894 will extend the rally from 0.6269 towards 0.7156 key resistance next. On the downside, however, break of 0.6796 support will indicate short term topping, on bearish divergence condition in 4H MACD. Intraday bias will be turned back to the downside for pullback to 0.6689 resistance turned support.

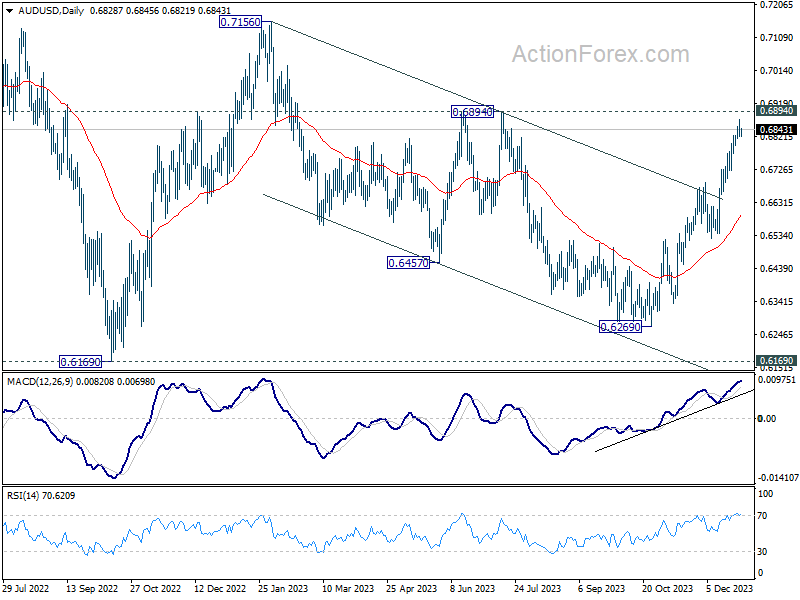

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | CHF | KOF Economic Barometer Dec | 97.3 | 96.7 | ||

| 14:45 | USD | Chicago PMI Dec | 50.7 | 55.8 |