Japanese Yen and Swiss Franc are standing out with significant rallies in otherwise relatively subdued markets today. Yen resumed its near-term rise against the Dollar, reaching its highest level in five months. Simultaneously, Swiss Franc has achieved its highest level in over a decade, excluding the spike seen in 2015.

While Dollar remains the weakest performer for the week, its selloff against currencies like the Sterling, Canadian Dollar, and Australian Dollar appears to be decelerating slightly. Euro remains firm, although it’s underperforming against Yen and Franc. But the Sterling is noticeably underperforming compared to its European peers.

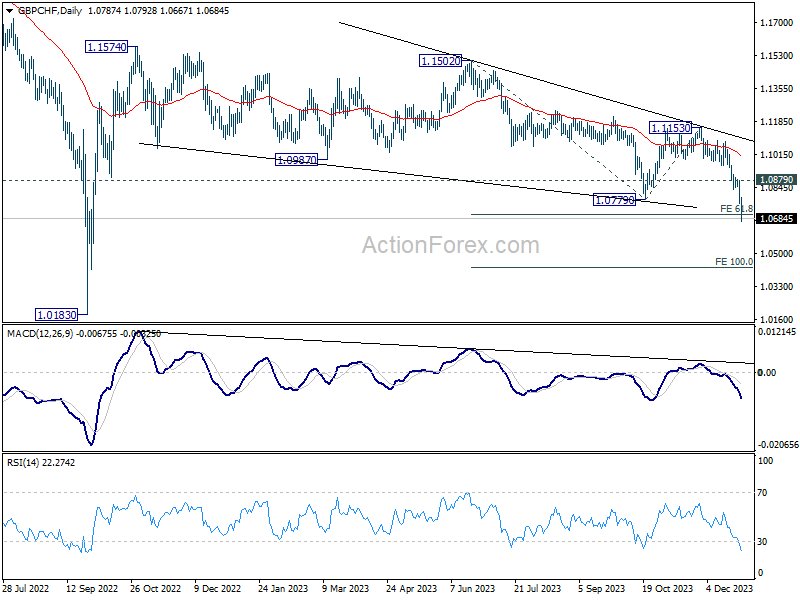

Technically, GBP/CHF’s decline accelerates further to as low as 1.0667 so far. 61.8% projection of 1.1502 to 1.0779 from 1.1153 at 1.0706 is take out. Near term outlook will stay bearish as long as 1.0879 resistance holds. Next target is 100% projection at 1.0430.

In Europe, at the time of writing, FTSE is up 0.05%. DAX is down -0.19%. CAC is down -0.41%. Germany 10-year yield is up 0.035 at 1.931. UK 10-year yield is up 0.062 at 3.497. Earlier in Asia, Nikkei fell -0.42%. Hong Kong HSI rose 2.52%. China Shanghai SSE rose 1.38%. Singapore Strait Times rose 1.38%. Japan 10-year JGB yield fell -0.0056 to 0.593.

US initial jobless claims rises to 218k, vs exp 204k

US initial jobless claims rose 12k to 218k in the week ending December 23, above expectation of 204k. Four-week moving average of initial claims fell -250 to 212k.

Continuing claims rose 14k to 1875k in the week ending December 16. Four-week moving average of continuing claims fell -12.5k to 1865k.

US goods trade deficit widens slightly to USD -90.3B in Nov

US goods export fell -3.6% mom to USD 165.1B in November. Goods imports fell -2.1% mom to USD 255.4B. Goods trade deficit widened from USD -89.6B to USD -90.3B, slightly larger than expectation of USD -89.5B.

Wholesale inventories fell -0.2% mom to USD 895.7B. Retail inventories fell -0.1% mom to USD 794.9B.

ECB’s Holzmann cautions against expectations of 2024 rate cuts

ECB Governing Council member Robert Holzmann emphasized there should be no presumption of rate reductions in the coming year.

Holzmann stated, “Even if the ECB is past an unprecedented series of ten consecutive rate increases, there is also for the year 2024 no guarantee of rate reductions.”

Further reinforcing this cautious approach, Holzmann remarked on the current status of inflation and the ECB’s policy measures, “Monetary policy normalization is already showing its impact on slowing inflation, but it would still be premature to think about rate cuts.”

Japan’s industrial production down -0.9% mom, continues to seesaw indecisively

Japan’s industrial production fell -0.9% mom in November, marking the first decrease in three months. This drop, however, was less severe than the expected -1.6% mom decline. A notable factor in the contraction was -2.5% mom fall in motor vehicle production. Among the 15 sectors surveyed, 11 reported decreased production, while four sectors experienced increases.

Index of industrial shipments also dropped by -1.3% mom, aligning with overall decline in industrial production. Conversely, Index of inventories saw a marginal increase of 0.1% mom.

The Ministry of Economy, Trade and Industry maintained its assessment of industrial output as “fluctuating indecisively.” Looking ahead, manufacturers expect a rebound in output by 6.0% mom in December, followed by -7.2% mom decrease in January 2023.

An METI official said, “We’ll continue to monitor the impact of the global economic downturn and rising prices”.

In separate release, retail sales data painted a more positive picture. Sales in November rose 5.3% yoy, exceeding forecast of 5.0% yoy, and marked the 21st consecutive month of expansion since March 2022. On a month-on-month basis, retail sales grew 1.0%, following 1.7% growth in October.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.31; (P) 142.08; (R1) 142.61; More…

USD/JPY’s break of 140.94 indicates resumption of fall from 151.89. Intraday bias is now on the downside. Next target is 136.63. fibonacci level. On the upside, above 142.84 minor resistance will turn intraday bias neutral gain. But recovery should be limited below 144.94 resistance to bring another decline.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Nov P | -0.90% | -1.60% | 1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Nov | 5.30% | 5.00% | 4.20% | 4.10% |

| 13:30 | USD | Initial Jobless Claims (Dec 22) | 218K | 204K | 205K | 206K |

| 13:30 | USD | Goods Trade Balance (USD) Nov P | -90.3B | -89.5B | -89.6B | |

| 13:30 | USD | Wholesale Inventories Nov P | -0.20% | -0.20% | -0.40% | |

| 15:00 | USD | Pending Home Sales M/M Nov | 1.10% | -1.50% | ||

| 15:30 | USD | Natural Gas Storage | -80B | -87B | ||

| 15:30 | USD | Crude Oil Inventories | -2.7M | 2.9M |