As US session gets underway, Dollar is declining broadly, influenced by a series of lackluster economic reports. US GDP growth for Q3 was revised downward to annualized rate of 4.9% in the final estimate. Additionally, Philadelphia Fed business outlook survey for December showed a drop from -5.9 to -10.5, signaling deeper contraction in regional manufacturing activity. However, the labor market showed some resilience, with jobless claims maintaining relatively stable level at 205,000, a positive sign amidst other economic headwinds.

Despite the negative economic indicators, US stock futures are pointing towards a higher opening, suggesting a potential rebound in the equity markets. Nevertheless, with the year-end holiday period approaching, there is uncertainty about whether this sell-off in Dollar and the uplift in stocks can be sustained over a longer period.

In other parts of the currency market, Japanese Yen is emerging as the strongest performer for the day, followed by Australian Dollar and Swiss Franc. Canadian Dollar and Sterling are positioned as the second and third weakest currencies, respectively, trailing Dollar. Euro is showing a mixed performance, positioned in the middle of currency chart.

In Europe, at the time of writing, FTSE is down -0.38%. DAX is down -0.31%. CAC is down -0.36%. Germany 10-year yield is down -0.024 at 1.949. UK 10-year yield is down -0.004 at 3.521. Earlier in Asia, Nikkei fell -1.59%. Hong Kong HSI rose 0.04%. China Shanghai SSE rose 0.57%. Singapore Strait Times rose 0.14%. Japan 10-year JGB yield rose 0.0289 to 0.592.

US initial jobless claims rises to 205k, below exp 220k

US initial jobless claims rises 2k to 205k in the week ending December 16, below expectation of 220k. Four-week moving average of initial claims fell -1.5k to 212k.

Continuing claims fell -1k to 1865k in the week ending December 9. Four-week moving average of continuing claims rose 6k to 1878k, highest since December 11, 2021.

Canada’s retail sales rises 0.7% mom in Oct, led by motor vehicle and parts

Canada’s retail sales rose 0.7% mom to CAD 66.9B in October, below expectation of 0.8% mom. Core retail sales—which exclude gasoline stations and fuel rose 1.2% mom.

Sales were up in seven of nine subsectors and were led by increases at motor vehicle and parts dealers (+1.1%).

Advance estimates suggest that sales were relatively unchanged in November.

ECB’s de Guindos: Premature for rate cut discussions, emphasizes Europe’s growth challenge

In an interview with 20 Minutos, ECB Vice President Luis de Guindos emphasized that it is “too early” to discuss rate cuts, despite recent favorable data. He stressed that the data available are still insufficient for ECB to alter its current monetary policy stance for now.

De Guindos highlighted ECB’s data-dependent approach: “We are data-dependent. The data have been favorable but still not enough for us to change our monetary policy.”

He also expressed confidence in the current interest rate levels, stating, “If sustained for a sufficiently long period of time, current interest rates will help bring inflation down to 2%.”

Addressing the prospect of a recession, de Guindos noted that ECB does not anticipate a technical recession, defined as two consecutive quarters of negative growth. However, he acknowledged a broader structural growth issue within Europe’s economy. ECB’s projections, along with those of European Commission, foresee only modest growth of around 1% until 2026.

De Guindos identified low productivity and the energy crisis as key challenges hindering Europe’s economic competitiveness, particularly given Europe’s reliance on energy imports. He argued for the necessity of structural reforms to address these issues.

While ECB’s focus remains on reducing inflation, de Guindos emphasized that achieving growth requires a broader set of solutions: “Structural reforms are therefore necessary. The aim of monetary policy is to reduce inflation, but to achieve growth, other factors must be brought into play.”

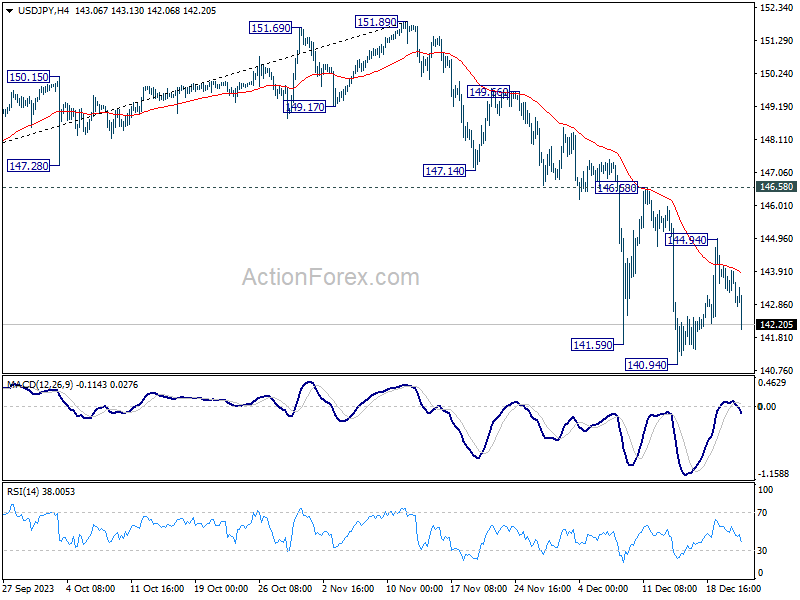

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.18; (P) 143.64; (R1) 144.02; More…

USD/JPY’s fall from 144.94 extends lower today but it’s staying above 140.94 support so far. Intraday bias remains neutral and more range trading could still be seen. But outlook will stay bearish as long as 146.58 resistance holds. Firm break of 140.94 will resume the whole fall from 151.89. Next target will be next fibonacci level at 136.63.

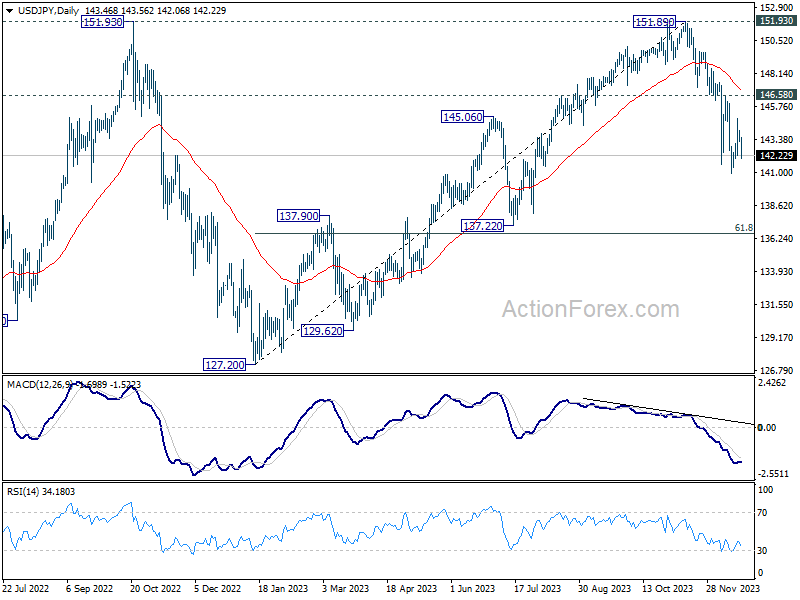

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | 13.4B | 13.2B | 14.0B | |

| 13:30 | CAD | Retail Sales M/M Oct | 0.70% | 0.80% | 0.60% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | 0.60% | 0.50% | 0.20% | |

| 13:30 | USD | Initial Jobless Claims (Dec 15) | 205K | 220K | 202K | 203K |

| 13:30 | USD | GDP Annualized Q3 | 4.90% | 5.20% | 5.20% | |

| 13:30 | USD | GDP Price Index Q3 | 3.60% | 3.60% | 3.60% | |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Dec | -10.5 | -3 | -5.9 | |

| 15:30 | USD | Natural Gas Storage | -82B | -55B |

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)