Euro is emerging as the strongest currency for the week, bolstered by ECB’s resistance to the expectations of a rate cut. The common currency will now look into today’s Eurozone data. Positive surprises from there could solidify ECB’s stance, and give Euro more fuel to extend recent rise. For now, Japanese Yen followed as the second strongest, supported by declining global treasury yields and in anticipation of the upcoming BoJ meeting. Australian Dollar ranked as the third strongest, driven by robust job data and an improving trade relationship with China.

Conversely, Dollar remains generally weak and is on track to be the worst performer for the week. Fed’s dovish turn led to sharp decline in the greenback and treasury yields, while simultaneously propelling DOW to record highs. The impact of these moves is ongoing and far from over. New Zealand Dollar ranks as the second-worst performer, with economists retracting their expectations of another rate hike by RBNZ following disappointing GDP data. Canadian Dollar also underperformed, despite a recovery in WTI crude oil prices above 70 mark. Sterling showed mixed performance despite BoE’s hawkish hold.

Technically, 10-year yield’s close below 4%, the long term channel support, as well as 55 W EMA is worth a mention. If TNX cannot quickly recovered to 4% handle, chances are deeper decline is imminent to 3.253 cluster support (38.2% retracement 0.398 to 4.997 at 3.24). This decline would extend through the rest of the year to the early part of Q1, and keep Dollar pressured and Yen afloat.

In Asia, Nikkei closed up 0.87%. Hong Kong HSI is up 2.05%. China Shanghai SSE is down -0.58%. Singapore Strait Times is down -0.34%. Japan 10-year JGB yield rose 0.0238 to 0.700. Overnight, DOW rose 0.43%. S&P 500 rose 0.26%. NASDAQ rose 0.19%. 10-year yield fell -0.103 to 3.930.

Japan’s PMI Composite up to 50.4, expansion resumes with inflation resurgence

Japan’s PMI data for December presents a mixed picture of the country’s economic The PMI Manufacturing index fell to 47.7 from 48.3, underperforming the market expectation of 48.2 and indicating contraction in the sector. In contrast, PMI Services index rose from 50.8 to 52.0. Consequently, PMI Composite index, moved back into expansion territory, rising from 49.6 to 50.4.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, noted, “The December PMI surveys indicate that Japan’s private sector experienced a renewed, albeit mild increase in overall business activity as the year came to a close.”

Fiddes further elaborated, “The overall performance of the private sector remained subdued.” This is evident in the composite new business, which declined for the second consecutive month. Although there was modest sales growth in the service sector, it was not sufficient to offset the sharp and accelerated drop in manufacturing orders.

Another critical aspect highlighted in the PMI report is the resurgence of inflationary pressures. Fiddes noted, “The latest survey also indicated a renewed pick up in inflationary pressures amid reports that a weaker exchange rate and higher labor and raw material costs had pushed up expenses.” As a result, the prices charged by Japanese firms increased at the fastest pace since August.

China’s industrial output Surges, retail sales and investment miss expectations

China’s economic data for November 2023 presented a mixed picture, with industrial output exceeding expectations while retail sales and fixed asset investment fell short.

Industrial output saw a significant increase of 6.6% yoy, surpassing the expected 5.6% yoy and marking the strongest expansion since February 2022.

However, retail sales, rose by 10.1% yoy, which was below the anticipated 12.5%. It’s important to note that this increase was influenced by a low base effect from the previous year, when China’s stringent coronavirus pandemic control measures significantly impacted consumer activities.

Fixed asset investment, a key driver of economic growth, increased by 2.9% ytd yoy, slightly missing the expected 3.0%.

National Bureau of Statistics of China commented on the overall economic situation, stating: “There are still a lot of external instabilities and uncertainties, and the domestic demand appears insufficient.” The NBS emphasized the need to solidify the foundation of the economy’s recovery.

Australia PMI composite climbs to 47.4, aligning with soft landing scenario

Australia’s manufacturing and service sectors showed marginal improvements in December, as indicated by the latest PMI data. PMI Manufacturing index inched up slightly from 47.7 to 47.8, while PMI Services index rose from 46.0 to 47.6. PMI Composite, which combines both manufacturing and services, also increased from 46.2 to 47.4. Despite these increases, all indices remained below 50.0 threshold that separates expansion from contraction, suggesting that both sectors are still facing challenges.

Warren Hogan, Chief Economic Advisor at Judo Bank, noted: “For the RBA and Treasury, these results are consistent with the soft landing view of the economic outlook. There are few signs that the economy is likely to tip into a steeper downturn next year.”

Hogan also emphasized the importance of the employment sector in this context: “Most importantly, the strong employment results suggest the economy may prove resilient in 2024. It is hard to see a sharp downturn in the economy while employment and incomes are expanding.”

NZ BNZ manufacturing improves to 46.7, ninth month in contraction

New Zealand’s manufacturing sector experienced a slight improvement in November, as indicated by the BusinessNZ Performance of Manufacturing Index. The index rose from 42.9 to 46.7, marking its highest level since June. However, it’s important to note that the PMI remained in contraction territory (below 50) for the ninth consecutive month.

Breaking down the index, several components witnessed modest improvements. Production increased from 41.6 to 43.6, employment from 43.8 to 47.9, new orders from 44.5 to 47.7, finished stocks from 45.8 to 50.7, and deliveries from 43.3 to 48.0. Despite these gains, the improvements were not strong enough to push the overall PMI into the expansion zone.

The proportion of negative comments from the manufacturing sector was 58.7%, a decrease from 65.1% in October and 68.8% in September. This indicates a slight shift in sentiment, although a significant portion of feedback remains pessimistic. The predominant concerns cited by manufacturers revolved around a general lack of demand and sales, highlighting the primary challenges facing the industry.

BNZ Senior Economist, Craig Ebert, particularly focused on the production index. He noted that despite a slight improvement in November, the production index remained almost 10 points below its long-term average. Ebert emphasized that “That’s a big undershoot, in historical context”.

Looking ahead

Flash PMIs from Eurozone and UK will be the main focuses in European session. Later in the day, US will release Empire State manufacturing index, industrial production and PMIs. Canada will release housing starts and wholesale sales.

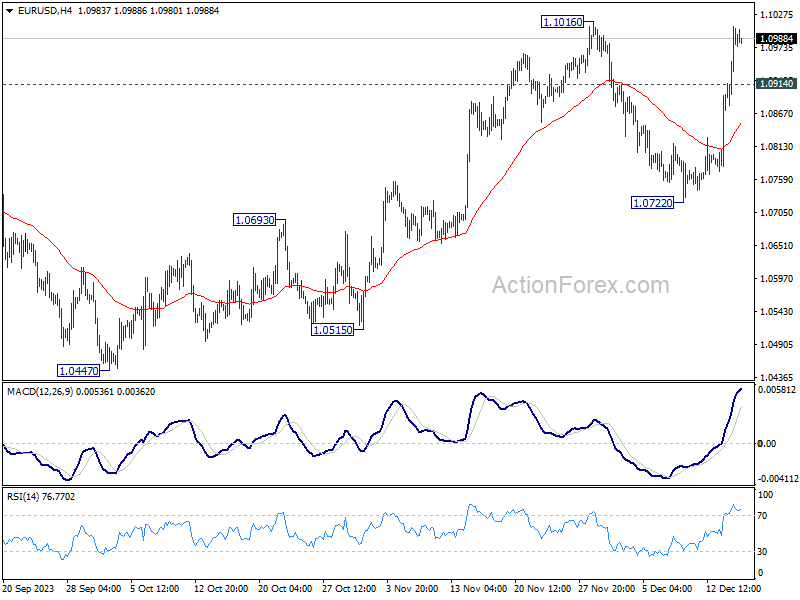

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0905; (P) 1.0957; (R1) 1.1044; More…

Intraday bias in EUR/USD stays on the upside for 1.1016 resistance. Decisive break there will will confirm resumption of whole rally from 1.0447. Further rally should then be seen to retest 1.1274 high. On the downside, below 1.0914 minor support will turn intraday bias neutral first. But outlook will stay cautiously bullish as long as 1.0722 support holds.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Nov | 46.7 | 42.5 | 42.9 | |

| 22:00 | AUD | Manufacturing PMI Dec P | 47.8 | 47.7 | ||

| 22:00 | AUD | Services PMI Dec P | 47.6 | 46 | ||

| 00:01 | GBP | GfK Consumer Confidence Dec | -22 | -23 | -24 | |

| 00:30 | JPY | Manufacturing PMI Dec P | 47.7 | 48.2 | 48.3 | |

| 00:30 | JPY | Services PMI Dec P | 52 | 50.8 | ||

| 02:00 | CNY | Industrial Production Y/Y Nov | 6.60% | 5.60% | 4.60% | |

| 02:00 | CNY | Retail Sales Y/Y Nov | 10.10% | 12.50% | 7.60% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 2.90% | 3.00% | 2.90% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | -0.80% | 0.20% | -1.00% | |

| 08:15 | EUR | France Manufacturing PMI Dec P | 43.2 | 42.9 | ||

| 08:15 | EUR | France Services PMI Dec P | 46 | 45.4 | ||

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 43.3 | 42.6 | ||

| 08:30 | EUR | Germany Services PMI Dec P | 49.8 | 49.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 44.5 | 44.2 | ||

| 09:00 | EUR | Eurozone Services PMI Dec P | 49 | 48.7 | ||

| 09:30 | GBP | Manufacturing PMI Dec P | 47.5 | 47.2 | ||

| 09:30 | GBP | Services PMI Dec P | 51 | 50.9 | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 10.3B | 9.2B | ||

| 13:15 | CAD | Housing Starts Y/Y Nov | 260.0K | 274.7K | ||

| 13:30 | CAD | Wholesale Sales M/M Oct | 0.50% | 0.40% | ||

| 13:30 | USD | Empire State Manufacturing Index Dec | 2 | 9.1 | ||

| 14:15 | USD | Industrial Production M/M Nov | 0.30% | -0.60% | ||

| 14:15 | USD | Capacity Utilization Nov | 79.20% | 78.90% | ||

| 14:45 | USD | Manufacturing PMI Dec P | 49.1 | 49.4 | ||

| 14:45 | USD | Services PMI Dec P | 50.5 | 50.8 |