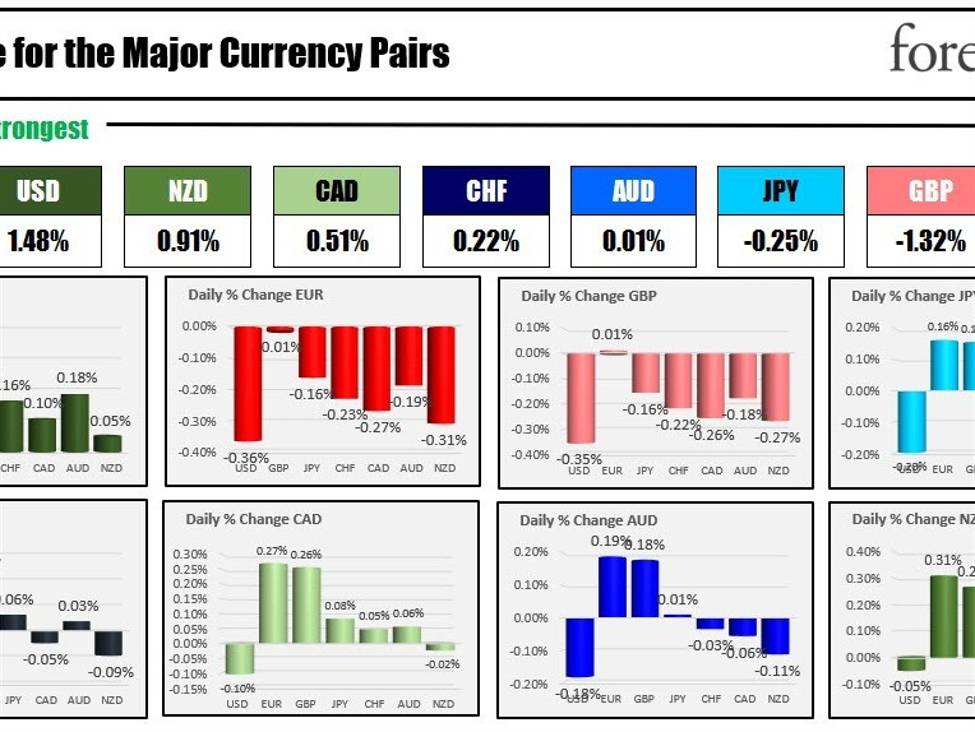

As the North American session begins. the USD is the strongest of the major currencies while the EUR is the weakest.

The latest Eurozone data released by Eurostat on November 30, 2023, showed that the preliminary Consumer Price Index (CPI) for November came in at +2.4%, lower than the expected +2.7% year-on-year. This comes after previous figures were at +2.9%. The core CPI, which excludes volatile items, was at +3.6%, also below the anticipated +3.9%, and down from the prior +4.2%. These softer-than-expected results, following similar trends in Spain, Germany, France, and Italy, present a challenge to the European Central Bank (ECB). While headline annual inflation is nearing the 2% target, core annual inflation remains just under 4% in November, indicating that the ECB’s efforts to curb inflation are not yet complete.

In Japan, Bank of Japan (BOJ) former deputy governor Toshiro Muto expressed his views on the current financial strategies of the BOJ. He suggested that there is a high likelihood of the BOJ abandoning its Yield Curve Control (YCC) and negative interest rates, potentially as soon as April next year. This decision largely depends on the results of the upcoming spring wage negotiations. Additionally, Muto mentioned that the BOJ is currently compelled to maintain its holdings in Exchange-Traded Funds (ETFs). He cautioned that any attempt to unwind these holdings might lead to a market sell-off. Meanwhile, Bank of Japan (BOJ) policymaker Toyoaki Nakamura commented on the potential timing for a shift in the bank’s monetary policy is challenging to precisely determine. Nakamura emphasized the risks associated with altering the policy based on the assumption of future improvements in the Japanese economy. He stated that now is not the appropriate time to consider a policy shift. However, he mentioned that a change could be considered when Japan’s economy shows sustainable increases in wages and inflation. Nakamura also highlighted the importance of examining firms’ profitability in deciding the timing of any policy shift. He mentioned that the BOJ is looking at various data, including the upcoming Ministry of Finance (MOF) quarterly business sentiment survey, to assess if the conditions are aligning for a potential policy change. It looks like all roads are pointing to the March/April wage negotiations for a change. As Justin likes to say, the can continues to get kicked down the road.

At 8:30 AM ET, the key PCE inflation data will be released in the US. This measure of inflation is the “preferred” gauge of inflation from the Federal Reserve which will be gearing up for its rate decision meeting on December 12-13.

- Forecast for the YoY inflation rate to be 3.0% for the month vs. 3.4% in September.

- On a monthly basis, inflation is expected to slow to 0.1% vs 0.4% last month.

- The core inflation rate, which excludes volatile items such as food and energy, is estimated to be 3.5% on an annual basis vs 3.7% last month.

- The monthly core inflation rate is projected at 0.2% vs 0.3% in September.

Personal income (0.2% versus 0.3% last month), and personal consumption 0.2% versus 0.7% last month will be released with PCE data.

Also, scheduled for release at 8:30 AM ET will be the weekly initial and continuing claims. The initial dose claims are expected at 220K versus 209K last week. Continuing claims are expected at 1.872M vs 1.840M last week. Last week if you recall both the measures decreased.

Canada GDP for the 3rd quarter will keep the 8:30 AM ET time slot busy with expectations of 0.2% versus -0.2% last quarter. The month-to-month expected at 0.0%.

US Pending home sales will be released at 10 AM ET

The OPEC+ meeting is taking place today and the twists and turns continue. Recent reports his morning suggested that an additional production cut of over 1 million barrels per day (bpd) might be implemented by members of a particular bloc, with most members agreeing on the necessity of these cuts at this time. The development led to a surge in oil prices, with a significant rally that pushed the price to a high near $79.60. The current price is trading around $78.50, up $0.63 or 0.78% on the day. Just a week earlier, internal disputes within the bloc had caused a slump in oil prices, dropping them to as low as $72.37 intraday. Adding another twist to the situation, Energy Intel correspondent Amena Bakr reports that the proposal might include Saudi Arabia extending their voluntary cut of 1 million bpd, potentially accompanied by additional cuts from other states. Despite the initial impact, this news seems to have had a less dramatic effect than first anticipated, as evidenced by a slight decrease in oil prices to $78.80.

A snapshot of the markets to kickstart the North American session shows:

- Crude oil is trading up $0.70 or 0.82% and $78.61. Yesterday at this time, the price was trading at $77.78

- Spot gold is trading down -$5.25 or -0.25% at $2038.87. Yesterday at this time, the price was trading at $2041.41

- Spot silver is trading up $0.07 or 0.28% and $25.07. Yesterday at this time, the price was trading at $24.97

- Bitcoin is trading lower at $37,888. Yesterday at this time, the price was trading at $38,250

In the US stock market, the major indices are implying a higher opening after mixed results yesterday. S&P and Nasdaq are set to have their best month since July 2022:

- Dow Industrial Average is trading up 223 points. Yesterday, the index rose 13.44 points or 0.04% at 35430.43. For the month, the Dow industrial average is up 7.19% (best since October 2022)

- S&P index is trading up 12 points. Yesterday, the index fell -4.33 points or -0.10% at 4550.57. For the month, the index is up 8.51%.

- NASDAQ index is up 49 point Yesterday, the index fell -23.27 points or -0.16% at 14258.49. For the month, the index is up 10.95%

In the European equity markets, the major indices are trading higher.

- German DAX, +0.46%. For the month, the index is up 9.68% – the best since November 2020

- France’s CAC, +0.56%. For the month, the index is up 6.15% which is the best since January 2023

- UK’s FTSE 100, +0.70%. For the month, the index is up 2.13%.

- Spain’s Ibex, +0.29%. For the month, the index is up 11.89%, its best month since November 2020.

- Italy’s FTSE MIB, +0.55% (10 minute delay)

In the US debt market, yields are trading mixed with the 2 year yield down while the rest of the yield curve is higher:

- US 2Y T-NOTE: 4.634% -1.3 basis points.. The level from this time yesterday was at 4.668%

- US 5Y T-NOTE: 4.224%, +0.5 basis points. The level from this time yesterday was at 4.228%

- US 10Y T-NOTE: 4.287%, +1.7 basis points. The level from this time yesterday was at 4.289%

- US 30Y BOND: 4.472%, +1.9 basis points. The level from this time yesterday was at 4.486%

- 2 – 10-year spread closed at -34.7 basis points. The level from this time on Friday was at -40.3 basis points

- 2 – 30 year spread closed at -16.8 basis points. The level from this time on Friday was at -22.1 basis points

In the European debt market, benchmark 10-year yields are trading higher:

European 10 year yields